Thank You, Contributors!

December 31, 2007 / January 1, 2008

To my great astonishment, 215 of you have donated money to this site since I began accepting contributions last March. Only two of you are old friends; 30 of you chose to honor the site with multiple donations. 45 of you generously donated $50 or more. The $6,000 contributed by you, readers, has made a huge difference in this poor dumb writer's daily existence.

This number far exceeded my modest expectations, as I reckoned a few dozen brave souls might respond and then the number of contributors would quickly drop to zero. Instead, you have continued to step up and donate throughout the year. This has been unexpected, humbling, and supremely encouraging. The site takes a lot of time, and I get hundreds of emails from readers which I try to answer in a timely fashion. (Illness and family business put me behind; please accept my apologies.)

Thank you, readers, for your support. Thanks to you, it has been an amazing year here at oftwominds.com. The "two minds" are yours and mine; together they create this site.

A number of things differentiate this site from the millions of other blogs and sites on the World Wide Web. Together, they have attracted an extremely thoughtful, experienced and erudite audience of contributors and readers which has grown from 14,000 unique visitors a month in January 2007 to 40-50,000 per month by year end.

1. The site has a diversity of voices and readers. According to the site logs, visitors from 101 nations have visited; perhaps more importantly, many essayists live elsewhere than the U.S.: John Kinsella (France), UKC and Mega (England) and Vera K. (Canada) to name a few. Within the U.S., comments come from Maine to Arizona to Texas to Florida and everywhere in between. Many of us have learned from the comments and charts provided by Harun I.

2. Readers provide key content: topics, critiques and commentaries. If a reader takes issue with some statement I've made, his or her comment is welcomed in Readers Journal. Many topics covered here are suggested by readers.

3. The focus is on writing, ideas, data and diversity of opinion. Good solid writing isn't a preserve of professional journalists; the quality of the writing posted here in Readers Journal is equal to or better than that found on any site. Read any essay by Michael Goodfellow or Protagoras or a dozen other contributors and you will be impressed. I know I am.

Your humble editor (me) has been a professional free-lance writer for major newspapers and other publications for 20 years. I strive to share the diversity of opinions and experience offered by you, the readers and contributors, and to write as sharply and entertainingly as I can about the wide range of topics you suggest.

Any reader who writes cogently on a topic is encouraged to share his/her work. Attacks, blind ideology, swearing and views unsupported by experience and/or data don't make it on the site. My guiding philosophy is simple: we all benefit from editing, and few of us have time to plow through 188 daily comments per blog (for example), most of which are repetitive or lacking in substance/value. I strive to be respectful of opposing views and I try to edit with a light hand, working from the notion that you'd rather read a few well-written comments and critiques in a few minutes than scan dozens of anonymous threads.

Though poetry is largely ignored/has zero influence in American culture, I am proud to provide a forum for poetry, from Haiku by UKC or Jed H. to creative, thoughtful works long and short by Protagoras and Verona U.

4. You are spared the clutter and mindlessness of advertising. Given that the site has attracted almost 900,000 visits this year, I suppose it could generate some decent ad revenue, but I prefer the honesty of asking for donations to the constant barrage of marketing of products and services I mostly detest--and you probably do, too.

5. This is an experiment in what I call Open Source Journalism. Open source software is freely available for anyone who is not using it commercially. In this sense, the blogosphere and indeed the Web is "open source" except for those sites which charge subscriptions for "premium content."

In other words, this site is free to you, and all data is sourced according to journalistic standards. Every commentator's email is known to me, though you are free to choose a name here for your comments which protects your own identity. There are no anonymous comments.

Put another way: financial contributors to this site are supporting a free, responsible form of journalism and commentary which is supported not by faceless corporate advertisers but by actual individuals like yourself. Once you contribute money, topics or comments, you join/support this outpost of Open Source Journalism.

What I love about this model is its complete democracy. Anyone is free to launch a blog, but attracting readers requires providing some content compelling enough for readers to invest precious time reading the content.

I also think what separates oftwominds.com from other sites is the dynamic of readers being commentators. Other sites have "the usual suspects" (other journalists and academics) as commentators, but here anyone can be a featured commentator if they take a few moments to compose their thoughts/analysis cogently. I am unimpressed by credentials, as no doubt you are, too; what impresses me is a thoughtful presentation which draws upon either data or experience unique to the commentator. (I think of contributor Nurse Dorothy, who brings a frontline point of view to healthcare topics.)

6. This site is not a link-farm; the content and many of the charts are original (and copyrighted). Take, for instance, this chart I made a few months ago. It tells a very different story than the one hyped by the financial and mainstream press, i.e. "the credit crisis is limited to subprime mortgages." Not so fast--take a look at the data first. (You won't find this chart anywhere else, though the data is readily available.)

7. The site seeks to surprise you with topics and ideas beyond the mainstream media and blogosphere. I'm as interested as the next bloke in finance, the stock market and the housing bubble, but every topic gets tiresome day after day. Hence, this site also covers films, literature, urban planning, nutrition, politics, history, energy, and a host of occasionally zany topics whose purpose is to enliven your day with the unexpected.

8. It's free--and it's all "premium content;" for better or for worse, it's my best work and the best of readers' work.

Here is my craven pitch:

There are no ads on this site to annoy you, except the fake ones I design for your amusement. (Please google 'Zombiestra'.)

A 95-minute movie with 10 minutes of ads and a popcorn costs $15. If you enjoyed this site for at least 2 hours this year, and you donate $15, you already received more entertainment than you did from the movie. The other 100+ hours of enjoyment you receive here is FREE (and lead-free and trans-fat free, too).

You have the immense moral satisfaction of aiding a poor dumb writer who seeks to inform, entertain and amuse you.

Donate $50 or more and I'll send you a signed copy of my completely ignored novel I-State Lines which is perfect for stabilizing wobbly tables and desks.

Donate $100 and I promise not to send you the book.

{/end craven pitch}

NOTE: contributions are humbly acknowledged in the order received.

Thank you, Andrew J. ($20), for your generous support of this humble site. I am greatly honored by your readership. All contributors are listed below in acknowledgement of my gratitude.

If you would like to contribute, please go to the main site www.oftwominds.com/blog.html

Monday, December 31, 2007

Saturday, December 29, 2007

The Stock Market: Poised on an Edge?

The stock market seems poised on a rather interesting edge. By all rights, the looming recession should make the future easy to predict: the market should fall hard as the reality of recession kicks in. But the future has proven to be remarkably resilient to easy predictions, and so all we have is charts and other tea leaves.

Let me start by noting I don't have a prediction. As frequent contributor Harun I. has said (and I paraphrase): no one knows what will happen, we can only know how we will respond.

As noted in the chart, the large head-and-shoulders formation which may have formed can be argued to mark a long-term top. On the other hand, the market has bounced twice off a line that was once resistance and is now support; double bottoms often denote market strength.

MACD is neutral, and could go either way, so there's no strong short-term trend in place. The multi-year long-term uptrend is still in place, and until that's broken then the Bullish stool (however wobbly it now seems) is still standing.

The confluence of the three moving averages suggests some major break of the red wedge up or down is nearing. If the 20-day and 50-day moving averages dip below the long-term 200-day MA, that is a bearish signal (i.e. "cross of death"). It wouldn't take much of a decline to create such a Cross of Death.

Since prices tend to oscillate between the Bollinger Bands, this suggests that the DJIA may move down to the 13,100 level before starting its next bounce to the top band.

As noted here before, I remain profoundly suspicious of any market move which is heartily supported by a dominant majority. The Market tends to take away the money of everyone betting on "the sure thing" as reflected by the options market. Right now the options bets are heavily weighted against the DJIA and the financial stocks rising, and in favor of oil continuing to rise.

As legendary trader Jesse Livermore trenchantly observed, the market moves to reward the fewest possible number of participants. If everyone is betting it will drop, then it somehow contrarily rewards the relative few still riding the "up" tram. When the majority are firmly confident that the market will rise, it contrarily decides to drop, taking along the fewest possible number of participants on the profitable "short" train.

Fundamentally, the market may be reflecting the great question which as yet has no clear answer: will the rest of the world shrug off the coming U.S. recession, enabling U.S. global corporations to grow profits in their non-U.S. markets?

To some degree, this has been the dominant theme of corporate profitability since the dot-com crash in 2001-2002. Domestic growth in most markets has been weak while overseas growth has been strong. Global U.S. corporations already earn most of their profits overseas, i.e. in non-U.S. markets. So it is not inconceivable to expect "more of the same." This is the Bullish case for the U.S. stock market's global companies.

On the other hand, if you see the erosion of the U.S. economy--still a quarter of the global GDP-- as dragging down the global economy and financial empires (as I do), then profits will eventually sag for all companies in all markets. That would remove the raison d'etre of the six-year old Bull Market.

But we shall see. January, and indeed 2008, will be interesting.

Thank you, Fred R. ($50), for your generous support, intellectual and financial, of this humble site. I am greatly honored by your gift of Mark Heard music and your readership. All contributors are listed below in acknowledgement of my gratitude.

Friday, December 28, 2007

What "Lies" Ahead (Part II)

Please forgive this unpardonable pun, but what lies ahead is, well, "lies" ahead.

The sophistry and chicanery behind "official" statistics is truly a wonder to behold. The obfuscation and manipulation has reached such epic proportions that even a financial media that is utterly in thrall to the manufactured illusion of "prosperity" is now timidly questioning some of the more blatant lies. That once-mighty dinosaur, the mainstream media, has even raised itself from its blissful (or shall we say slothful?) torpor to wonder how food and energy can rise by double-digit leaps and bounds while official inflation hums along at a near-zero 2-3%.

Thus we may soon have shantytowns (see photo above) in which the residents will wonder what alternative universe their nation's media inhabits as it continues to spout the officially-massaged "data" that everything is really really fine.

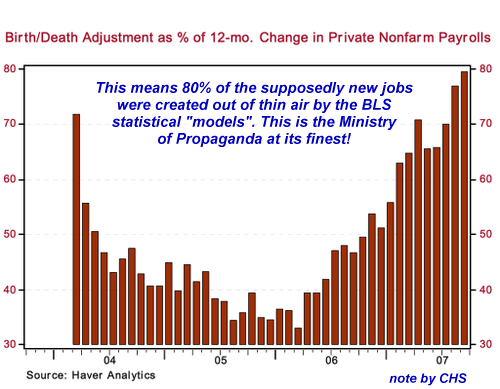

Others with more expertise than myself have picked apart each statistical legerdemain in great detail, but let's just grant the obvious by noting that assuming jobs are being created because more people have been born than have died is a wee bit suspicious.

With this logic, why don't we also just assume that since people are living longer, they are also working longer? Since we can "model" this statistically, why bother actually surveying the populace?

Granted, this is a nation of 300 million people, and accuracy is always statistically ambiguous at the edges of any poll or survey. But why should people who have been unemployed longer than six months be dropped from the ledger? (Let's just call them "discouraged" and no longer count them. It might muss the glowing picture we're painting here to have to include the "discouraged" job seekers.)

Yes, there are reasons for all the adjustments and models, and no doubt those employed to prepare the stats can argue quite passionately for the inadequacies of a simple count. But the point is: who benefits from a rosier-than-reality snapshot? Who has a deep and abiding interest in maintaining the illusion that all is well in an economy staggering down a rocky slope to recession?

Somehow the statisticians never seem to address that question, or the agenda behind the models.

A note on my photo. When I started this little blog I decided to display my physical being via a recent photo of some sort, as I always wonder what the writer of a blog actually looks like. While I understand the need for privacy, I reckoned it some sort of "truth in advertising."

The photo of me in sunglasses elicited comments that I was "hiding" (or worse, smirking) and I needed a haircut. The photo of me in the collarless shirt elicited both a word of praise and a word of tongue-in-cheek critique, to wit, "This looks like banker-bob trying to interest me in a short sale."

Clearly, this is a tough audience. My solution is to swap photos around, i.e. displease everyone equally.

To make sense of the above note, please go to my my blog page at www.oftwominds.com/blog.html

Thank you, Jeff B. ($20), for your generous contribution to this humble site. I am greatly honored by your gift and your readership. All contributors are listed below in acknowledgement of my gratitude.

Thursday, December 27, 2007

What Lies Ahead

Now that the speculative housing/lending bubble is undeniably deflating and the U.S. economy is sliding into recession--just as this site has been predicting for 2 years-- the bloom is off the doom and gloom.

(Sorry, I couldn't resist that bit of doggerel.) Truth be told, now that the decline in housing is being covered by every publication known to humanity, it's become rather boring. I mean, how many ways can you say, "housing is going down for a long time"?

Ditto with "the U.S. is heading into recession." The flaccid attempts at a "debate" engineered by the financial press are laughably absurd, as the same tired old hands who failed to foresee the 2000-2002 recession are again trundled out to make yet more failed forecasts of permanent rosiness.

As a result, there is less and less to say of any value about housing and the financial meltdown in the U.S. It was fun to cover those topics when they were being ignored and glossed over by the mainstream and financial press, but now that doom and gloom is mainstream, my focus in 2008 will shift to what is less obvious: the feedback of forces attempting to ameliorate and counter the destruction of risk and wealth we all see at work.

In my view, the Empire Will Strike Back to protect its assets, reach and power, and to expect the U.S. economy to roll over and expire in a nice predictable swan-dive of doom is foolhardy, given the scope of that Empire:

This great, long unraveling--and the powerful counter-trend rallies as the Empire responds--certainly will impact our own financial situations. Everyone wants to know where to put their nestegg to preserve capital/buying power and perhaps even increase the nestegg, and the worldview I will explore is this: there are no "long-term" straightforward investment answers anymore. Risk has retaken the field, and every investment strategy that seems to be well-grounded and working well will stop working.

The era in which you could follow some simple plan year in and year out such as "buy on the dips" or "buy precious metals" may well be over. That is the thesis I will explore.

Just to reiterate what has been established here in dozens and dozens of entries and charts: the housing decline has barely started; the bottom is at least 4-5 years away. Anyone buying in previously "hot" markets in the next year or three will see their investment lose value, perhaps by a stupendous percentage.

The U.S. will enter a long, confusing recession which will fail to respond to the usual elixirs of lower interest rates and more government deficit spending. Structural imbalances in the global economy will drag the rest of the world, including China and India, into recession behind the U.S. Oil will plummet in price as demand drops, for this recession will deepen with time. It will not be "shallow" or brief, despite all the official predictions that it will be a mere pinprick.

Most importantly, I will continue to strive for that most difficult goal: to surprise you. Once you can predict what I will cover tomorrow, I will have lost my edge. What keeps me sharp, of course, is you: your ideas, your suggestions, your critiques. That's what keeps the site lively and unpredictable: the amazing range of reader intelligence and experience.

Thank you, Pedro V. ($10), for your generous contribution to this humble site. I am greatly honored by your gift and your readership. All contributors are listed below in acknowledgement of my gratitude.

Wednesday, December 26, 2007

Who Decides What Is Art?

For most of human history, Art was defined by those who hired the artisans: religious leaders and monarchs. In the Renaissance, the circle of art patrons widened to include nobility and wealthy merchants.

In our post-industrial, self-consciously ironic age, Art has become the purview of hyper-self-referential academia, "professional" artists and institutional curators. If you don't "get it," then you're "outside the inner circle."

So when you go to a modern institution which takes as its task the definition of Art (and the deification of Art), you may find an "installation" of a hundred little bottles filled with colored fluid randomly placed on a plywood board.

This is "high Art" with a capital A because it consciously references "cutting edge" works previously approved by the institutional Priesthood--the professional journals, the prestigious museums, the respected curators, and the academic Art community.

What the self-referential institutionalization of Art actually does is reify Art-- withdraw it from the public discourse and consciously alienate it from the broader culture. This is the root of the division of "high Art" (approved by the institutional gatekeepers, i.e. the Elite Clergy of Art) from "low art" such as manga, comic books, web design, YouTube videos, etc.

If you haunt museums, then you already know that every "high Art" attempts to hijack or "refine" "low art" realms like the Web and video are always ham-handed failures. Their failure is an a priori one, for any attempt to reify what is essential a popular medium is doomed from the start.

The only way "low art" such as comics can be elevated to "high art" is when they have been processed through the Irony Mill, as Any Warhol did with comics and tomato soup labels. (Recall that Warhol was rejected by every gallery in New York for a decade. Then, magically, Institutional Art "got it" and elevated him to godlike status.)

My own view is that Art comes from within those with an irresistable urge to create. Those driven to create fashion objects, music or words which become art not by their skill but by the irresistability of their creative forces. For example, take a look at the musical instruments created by longtime contributor Bill Murath, a talented and creative craftsman.

When I saw these photos I instantly thought, "These belong in an art gallery or museum." In other words, they are pieces of art as well as musical instruments. Bill was not commissioned to make these works of art/instruments (which he jocularly calls "tuna bowls"), nor did he create them to earn an academic art degree. He is not "referencing" some "high Art" pieces already ordained by the Priesthood; the design, purpose, fabrication and finish all come from within him.

These instruments are, to me, wonderful art, and the fact that they create a secondary level of art--music--beyond the visual and sculptural make them even more wonderful.

Please go to www.oftwominds.com/blog.html to view the photos.

Here are Bill's own comments about the instruments:

"My art/creations are outward manifestations of my acquired knowledge and out of the box thinking which compensates for my lack of normal communications skills. A good way to describe where I and my art come are the 2 movies I relate to most. Not that I am a big Kev Costner fan but Field of Dreams and Tin Cup just resonate with me.

My goal with these 'tuna bowls'... not that I really have one is to let people find internal harmony by intuitively playing these things. That is why I chose to have people play these with mallets... their hands, which require much less upfront thought or study than using one's fingers. They can play what sounds good deep into an individual's soul with both harmony and rhythm. (Melody is there through an understanding of the 7 Greek modes.)"

Bill did not attach the "all rights reserved" tags to his photos, I did--to protect in some small way his creativity. (I don't think he considers this necessary.) I want anyone who may take one of these photos off the Web to know who created the instruments.

I know most of you don't ponder "what is Art?" as part of your daily concerns, but I think it a worthy question, just as I think it worthy to pronounce Bill's work Art with a Capital A. Thank you, Bill for sharing your creations with us. I sure want to know what they sound like now.

Note to readers: I have been away from my desk for a week and am suffering from a horrendous cold, so I am way behind on replying to email. Thank you for your patience.

Thank you, Christopher M. ($25), for your generous contribution to this humble site. I am greatly honored by your gift and your readership. All contributors are listed below in acknowledgement of my gratitude.

Monday, December 24, 2007

The Christmas Letter I'd Like To See

December 25, 2007

Whenever I get a cheery form Christmas letter from family and friends, my first instinct is to begin composing a biting parody of the genre. My wife observed this would reveal my true psychological profile (yikes!), but since you have (mostly) tolerated my various stupidities over the past year, I decided to share the results anyway.

{parody initiating . . . launch parody}

Dear Friends and Family:

I hope this holiday season finds you well and in good cheer. Things are certainly looking up here, as I managed to extricate myself from Federal prison last week by hocking the house. It was all a setup--the quarter-ton of Canadian OxyCotin in the trunk of the Cadillac, the empty Jack Daniel bottle in my lap, the "Cheney 2008" bumper stickers, the inflammatory Mo Tzu literature littering the back seat, the Twinkies wrappers, all of it.

You all know I prefer Zinfandel, so it was painfully obvious that the COINTELPRO crew only did a cursory background check. What really fries my fat is that I didn't even rank high enough on the Enemies List to get a quality character assassination--though they did get the Mo Tzu right.

I've stopped flying commercial airlines within the U.S. due to the fact I can never book a seat online any more; now I have to "check in to obtain a boarding pass" even on a half-empty flight. But enough of my troubles-- which you probably are dismissing as yet more paranoid rantings. I wanted to send you copies of my old 1970s-era FBI file which I obtained via the Freedom of Information Act, but thought, why bother decent law-abiding citizens with this junk at Christmas?

My health is improving after my little adventure in China. I always wanted to try an "extreme sport" before I get too old, so I signed up to climb the 1,000 foot tall bamboo Kroika Tower outside Shanghai. The climb went well until the freak windstorm hit.

As you know, bamboo is remarkably flexible, and as a result the top two hundred feet of the tower whipped back and forth with astounding force. Observers estimated the top was swinging at least 50 feet, a number I can't confirm, as I was flung off the tower and landed in a very surprised farmer's pigsty. Fortunately I missed the pigs and my fall was cushioned by the soft mud.

My flight was somehow recorded by a Chinese film student filming the tower, and I am pleased to note the YouTube clip has been hit over a million times. Woo-hee, fame at last!

Apparently the Chinese authorities discovered my interest in Mo Tzu and the Legalist School of Chinese philosophy, and so I was quickly bundled up as a subversive and put on the next flight back to the States. If it wasn't for the crack legal team of the hugely influential American-Chinese Philosophy Club, I might be rotting in some Chinese gulag instead of enjoying the "Club Fed" Federal Prison where I ended up on Homeland Security Act Violations.

I was just out of traction when I woke up on the U.S./Canadian border in the Caddy with the "hot" OxyCotin. Funnily enough, I wasn't even taking any for my own pain. You gotta hand it to those zany COINTELPRO guys, they have a keen sense of irony!

Now that I'm out of the pen, I'm enjoying a modest fund-raising success on a street corner here in town. I have plugged my trusty Les Paul electric guitar into a portable amp and my sign reads, "Give me money and I'll stop playing 'All Along the Watchtower.'" I got the idea from those weeklong PBS torture-fests known as "pledge drives". I think the eye-patch and all the barely healed wounds are eliciting the sympathy of passersby, though I do hear some negative patter and have been robbed repeatedly. But hey, life is good!

I'm kind of hacked off that Mo Tzu's name and ideas are being smeared along with my own, but Christmas is a time for joy and gratitude and I'm trying to look past the business failure that wiped out the last of our savings, my injuries, my countersuit against the government (hopeless, I know) and the fact that I have to tape my left hand to the guitar in order to play.

The pets are doing OK, though my beloved parrot lost a leg in an accident which I won't describe as it is too painful. I probably told you about the house roof, right? I did get a blue tarp over the gaping hole left by that frozen chunk of airliner latrine waste which crashed right through the rafters; bad things happen in threes, I guess, and since I've racked up six, I should be in for some good luck in 2008.

Have a safe happy Christmas!

{/end parody}

Thank you, readers, for all your astonishing support of this humble site in 2007. I am greatly honored by your readership. All contributors are listed below in acknowledgement of my gratitude.

Thursday, December 20, 2007

Holiday Viewing and Readers Journal

Since I will be visiting family for the next five days, I want to wish you--yes, you-- a safe and peaceful holiday.

Our usual programming mix of cynical skepticism and occasional zany foolishness will resume after Christmas.

Since holidays can be stressful, watching a film together at the end of a long day can offer low-key respite/fun. We recently asked our dear Italian friend (and movie buff) Emilia for a list of some of her favorite Italian films, and in the spirit of sharing holiday "movie ideas," here is her list. To help you decide if you might like to see/rent the film, I have linked the films to amazon.com's brief review and viewer comments.

Many of us have seen Il Postino and Cinema Paradiso, and perhaps the Fellini masterpiece La Strada or De Sica's The Bicycle Thief, but many of the other films are less known--for us, Christ Stopped at Eboli was a revelation, and a film effortlessly added to our "best films of all time" list.

Ladri di Biciclette) The Bicycle Thief

The Postman (there is an American film of this title as well, hence is it listed as)

Il Postino (Io Non Ho Paura)

I'm Not Scared (Cristo si e' fermato ad Eboli)

Christ Stopped at Eboli (Novecento)

The Legend of 1900 (Le notti di Cabiria) (By Federico Fellini)

Nights of Cabiria

La Strada

Malena

Cinema Paradiso

(Non ti muovere) Don't Move

Readers responded with substantive comments on the 12/18 entry Bailout: Could Government Actually Be Part of the Solution?. I think you'll enjoy the diversity of opinion. Longtime contributor Kip S. checked in with a fascinating closed-grained look at the price history and condition of a Northern California home currently for sale.

NOTE: If you have time/need a break from holiday stress, you might enjoy browsing through Readers Journal (essays listed in right sidebar), 2007 archives, or for some short fiction, the spicily named forbidden stories beckon.

Frequent contributor Harun I. made these cogent points:

I completely agree. Quickly acting to get rid of bad debt is the sensible thing to do.

The problem with bailouts: Once started, where does it end? Most are short-term fixes that do not address the fundamental issue, empirically this has led to progressively larger problems and bailouts. The fundamental issue lies in the psyche of those sucked into the delusion vortex.

To wit: Fixing the S&L crisis did not prevent the today’s crisis. Fixing the 1987 crisis did not prevent LTCM. Fixing LTCM did not prevent where we are today. The problems have progressively gotten larger because of the psychology created by bailouts that we term to be moral hazard.

There is nothing wrong with suffering. Suffering teaches valuable lessons; it forces adaptation. It is when adaptation cannot happen quickly enough that extinction occurs. The moral hazard of bailouts has now put the global financial system at risk of breakdown because the problem is now too large for successful adaptation by normal means.

In other words, the unchecked, parabolic, leveraged growth of financial derivatives far outweighing the physical output of the entire global economy has left us with no answers that can be employed quickly enough to offset the rate of change of the ensuing crisis in a way that will prevent suffering. Deflation, there will be suffering. Hyperinflation, there will be suffering. A new Bretton-Woods system, there will be suffering.

Every bad trade has taught me a valuable lesson, sometimes I needed to learn the lesson more than once. But the pain of those events taught me what not to do. Remove consequences from actions then what? Everyone wins or loses and nothing has value? Wouldn't this be the reason central planning failed?

Moral hazard, however inconvenient, is real. There is no such thing as a little moral hazard. And the lesson of Pandora's Box has to assert itself once more. Once a “little” moral hazard has been injected, how do we stop?

Next up, longtime contributor K.K.: (original entry excerpts in italics)

I am not predisposed to any bailout, but intellectual honesty requires me to recall that the much-maligned "bailout" of Chrysler in the early 1980s saved the company and tens of thousands of jobs at modest (or according to Lee Iacocca, zero) government funds.

1. The bailout did cost taxpayer funds

2. It is not the place of the government to "save jobs" since people that want to work will just get new jobs (most of the buggy wheel makers got new jobs just like most of the Chrysler employees would have got new jobs)...

Though it was obvious the Savings and Loan collapse in the 80s was caused largely by Reagan-era deregulation of an industry which simply requires some regulation--

The S&L crises was caused by 1. Changes in the tax laws that lowered the value of real estate, 2. Poor underwriting by a government insurance company (no private company would have insured $10mm of deposits with very little capital or lending restrictions)...

L.S. recommends that people under threat of foreclosure try to work it out with their lenders.

Great idea, but if you lied about what you make and borrowed more than you can ever pay back there is not much to "work out"...

Today (12/15-16)'s WSJ cites the proposal of "Center for American Progress, a liberal think tank ... that the government buy some mortgage-backed securities and create a new agency, the Family Foreclosure Rescue Corp. [to] issue new, more affordable fixed-rate mortgages for those facing foreclosure whose homes are worth less than what they owe.

No surprise that a "liberal think tank" thinks that it is a good idea to tax responsible Americans to help dumb Americans who have too much debt...

3. We can safely assume about 25% of distressed buyers were speculators who never occupied the house, i.e. "flippers."

ALL the distressed buyers were "speculators" (but not all were "flippers"). No one would pay more to "buy" a home than rent a home if they didn't "speculate" that the property values were going to go up...

Let's guesstimate that another 50% of distressed properties were purchased by buyers with little or no "skin in the game," i.e. down payment. The S.F. Chronicle study found that about 70% of subprime buyers in 2005-2006 put no money down. Thus, these people will lose virtually nothing in foreclosure because they brought nothing to the party in the first place.

Almost all of the people in trouble have little or no "skin in the game" since values have not gone down very much (yet) anyone who made a down payment can still sell and walk away...

From one view, it can be argued that since government enabled the entire bubble via lack of lending/investment banking oversight (once again), it should be part of the solution.

The bubble was caused by dumb buyers and dumb lenders (and bond buyers)… If the government does nothing it will be the dumb buyers, dumb lenders (including their dumb stockholders) and dumb bond buyers that pay the price...

I am talking about a government-sponsored auction of debt and properties along the lines of the Resolution Trust Corporation which cleared up the S&L mess in the late 80s/early 90s.

The RTC sucked up billions of tax dollars...

Frequent contributor Michael Goodfellow made these comments:

What killed the S&L's was not lack of government regulation. They were all in the business of taking short-term deposits and lending long-term mortgage money. When interest rates spiked in the 70's and early 80's, they were in an impossible position -- getting 6% on mortgages while forced to offer 8% on money market accounts. If that situation lasted long enough, they were doomed.

The government should be blamed for putting them in that position by mismanaging the money supply and creating the huge inflation of that time. The government did finally raise interest rates enough to kill inflation, but it took years too long. In the meantime, the government insurance of individual accounts made it possible for the S&L's to speculate risk free.

Since they couldn't lose account money, the S&L's moved into really stupid investments. chasing higher rates of return to make up for their losses on mortgages. That eventually failed and created the S&L "crisis." Eventually, the government come in and formed the RTC to clean up what was left of the industry. I'm not sure who took all the loses, but some of it went on the taxpayer's tab.

A sad story all around, but I wouldn't characterize it as lack of government oversight.

After I suggested inflation was only rampant in the early 80s, Michael added these notes:

This page inflationdata.com is a bit of a mess, but has 11% inflation for 1974, 9% for 75, then lower figures. 11% again in 79, 13%, 10% for the years after.

Also, I think it's unfair to say that government guarantees like the $100K deposit insurance don't count as "regulation." A much lower deposit insurance, or a max per depositor, not per account, would have introduced a lot more caution into the system.

I agree that the S&L's were looted in many places, but I think that was the end of the bubble, just as the "NINJA" loans were more prevalent at the end of the housing bubble. Once common sense goes out the window, the criminal actions get much more brazen.

Knowledgeable reader L.S., whose initial comments were reprinted in the 12/18 entry, offered this follow-up account:

Robert Roth wrote:

"L.S. recommends that people under threat of foreclosure try to work it out with their lenders. I have read in several places that that approach is problematic because in many (most?) cases, the people who collect the payments don't even know who holds the mortgage -- that precisely the complexity and opacity of the securities backed by these mortgages makes impractical the old-fashioned way of addressing the problem that L.S. suggests. If I'm wrong about that, I'd love to hear it, and wish someone would say so and why."

If you’ll indulge me, I tell you my story about the last real estate downturn and why I think my comments are not as naive as they may sound.

Newly married in summer 1990 and panicked that we would be priced out of the market, my bride and I skimped on our wedding so we could come up with the deposit for a condo. Since we only had an 18% down payment instead of the preferred 20%, we had to carry PMI (mortgage insurance), but we got in with an 8.875% 30-due-in-7 loan.

My wife was attending college and selling real estate, but by late 1990 the crashing market wiped our her income. A ruptured disk in her spine further reduced her ability to work so we struggled through 1991 just on my income.

In January of 1992, my employer announced they were closing their Southern California division and consolidating in Florida. By February I was unemployed. This was during the aerospace downsizing, and like many others in the engineering field, I was having trouble finding work. I quickly blew through my small severance pay on the mortgage and overpriced COBRA payments since a new medical policy would have excluded my wife’s now pre-existing back problems.

While I eventually got another job, and my wife worked at some low paying retail and real estate assistant jobs, we had lost a lot of ground financially and were constantly playing catch up with our bills. I’ll never forget calling the finance company from a hospital waiting room, begging them not to repo my wife’s 5 year-old second-hand Volkswagen, as she was undergoing emergency surgery. Two weeks later when I chased down the repo men, they told me if I gave them the remote it would cost $100 less in fees. That was our good car.

We had listed and relisted the condo for sale, each time reducing the price. We said goodbye to our down payment. We got a broker friend to handle it without a sellers side commission. No luck. We were stuck.

I called the lender numerous times, begging for some relief. Could we roll the late payments into the balance? NO. Could you lower the payment temporarily? NO. Could you change the interest rate temporarily? NO.NO.NO. At one point after receiving a notice of foreclosure, I begged them to take the two and a half payments I scraped up with a promise to deliver the remaining half in 10 days. Nope – full amount or we foreclose.

But even if we had received an offer on the condo, it wouldn’t have mattered. The owners had been moving out and renting their units. When we moved in, it was 80% owner occupied – just above the 75% minimum required for loan approval. Now it was 80% rental. And the renters were not always good neighbors – like the gang member whose buddies came over to drink, one of which we saw showing his gun to another as we sat in our living room. When I asked the owner how he could have rented to this guy, he replied – I kid you not – that he thought the gang member was a good credit risk because he was getting a big settlement from the police after being shot at a traffic stop. There’s more, lots more.

Then I learned the world is a dynamic place.

---------------------------------

Up to that point I assumed if you owed money to a bank, that was one step below owing it to God. There was little question of you paying it back.

In 1993 my wife started working for a small property management company that had recently secured a contract to dispose of REO’s from Fannie Mae and a number of their client banks. Every week there would be a fresh batch of listings on the fax. They would go and trash out the property, change the locks, install smoke detectors, and list it on MLS. If it was occupied, offer 500 to 1000 bucks cash for keys or start the eviction. Usually these were renters. Owners nearly always had split.

I went to many of these properties and was astounded at the money loaned against them on seconds and even some thirds! I mean, what were the banks thinking? One with an $80K first was literally a shack on a hillside. One wall of the bathroom was dirt with tree roots protruding out of it! Some properties had additions that looked cobbled together with scrap material, yet had a $200K-$300K second!

The banks insisted these properties be listed for the loan amount, which meant they wouldn’t sell. So month after month, another 10 to 25K was shaved off the price until it moved. Fannie Mae even started paying $8K per property for paint and carpet to get them to move.

This office was also doing short sales. Never would I have imagined a bank would settle tens or even hundreds of thousands of dollars less than it was owed. But it was an event I witnessed many times, as my wife, who had reactivated her license, handled these transactions. Pretty soon lenders were even allowing short sales between family members.

By 1994 the flood of REO properties showed no signs of receding and lenders were starting to do loan modifications. One was for the guy who did the trash outs for the company. He had been trading up properties during the 80’s and was underwater on the last purchase. My wife handled the transaction. She got the lender to knock $150K off the balance and give the guy a new loan. Astounding.

Not long after that we did a short sale on the condo. We bought a foreclosure which Fannie Mae had graciously painted and carpeted, and was offering for only 3% down, and without PMI since they were carrying the loan.

-------------------------------------

So what’s the point of this long, boring story?

Robert Roth wrote:

"L.S. recommends that people under threat of foreclosure try to work it out with their lenders. I have read in several places that that approach is problematic because…"

This is what I directly addressed in my original comments. Opinion mixed with some fact gets repeated until it becomes the conventional wisdom and discourages people from acting. In the late 80’s, who would have imagined the banks would be doing short sales by the early 90’s? And only a madman would suggest that a few years after that, banks would be doing no doc, 100%, sub prime loans to farmworkers for half a million dollars. Don’t assume any avenue is closed just because you hear it often repeated or because it’s true at this very moment.

One other point is that not all these loans have been securitized, whatever that may imply. The banks still hold a bunch of them as regular loans. Citibank just moved $49B worth back onto it’s balance sheet. Does that help untangle them? Who knows. You think the borrowers are under pressure? The lenders are going to feel it by orders of magnitude greater and will have to act.

And here is longtime contributor Kip S.'s account of a classic Eichler-designed and built home in richly overpriced Northern California:

(For those unfamiliar with the name Eichler, he was the 1950-60s-era builder of the quintessential "California Ranch" style home, a design largely inspired by Frank Lloyd Wright's low-slung Usonian houses.)

Again, thanks for the detailed response to my renovation question. The house I mentioned (1400 sq ft 3br 2ba 1955 vintage Eichler in the San Francisco Bay Area) was open yesterday and I did a walkthrough.

I’m not a professional builder but have done some renovation work over the years (e.g. kitchen, bath, built interior walls, etc) and I was amazed at the condition of the place. Some of the highlights that your $630,000 brings: Non-functional heating; non-functional solar hot water heating (on roof), bathrooms with collapsing walls (I touched a shower wall and pieces literally started falling); no kitchen; bad roof; rotten carpet, mold, and apparent water damage to the structural wooden beams. That’s in a 10 minute walk through by a non-professional. In my humble opinion, the entire property should either be a) leveled, or b) gutted down to the studs. At least the listing agent is honest and just says “As-is. Bring all offers”. I don’t think they’d like my offer.

The reason why I’m writing today is because of another house (about the same size and vintage) that I saw in the same neighborhood that is both an apparent flip gone bad and what exemplifies everything that went wrong during the bubble. This second one has new Pergo type floors, 2 nicely but bizarrely renovated bathrooms, new kitchen cabinets with granite countertop (naturally!), and a high end range hood (GE Monogram). However, this work is coupled with a 10 year old stove, and 10 year old dishwasher, a broken garage door, peeling wallpaper throughout the house, dead garden, etc. Now here’s the kicker – I looked it up on Domania (great website) and it shows 3 sales in the last 7 years:

April 2000 -- $495K (seemed high even then, but it was the peak of the dotcom bubble)

March 2006 -- $920K (!!); August 2006 -- $985K (!!!!).

It’s on the market (just reduced) for $730K. Fair price – probably under $400K.

I keep harping on this because of the collateral damage done by the bubble. The area I’m referencing is a small (maybe ½ by ¾ mile square) neighborhood of Eichler homes (200 or so) in an OK area. A traditional development. How many individual were coerced by the propaganda of the RE industry to mortgage their lives for a house that in a non-bubble market would sell for one-half or less than the price that they paid?

In my quick review of Domania, there were at least 50 transactions in the past 3 years -- ranging from $600-900K. Now there may be multiple sales of the same property, but it's still a lot of transactions. For all of the discussions of CDOs, unscrupulous mortgage brokers, shady real estate agents, etc. the real damage will be done to those poor souls who paid $850K in January 2007 for a house that sold for $298K in January 2000. What are they going to do? The amounts involved are what one commentator called “whoo-whoo” money: a number so large that it’s not realistically conceivable to have for most people. It will NEVER be paid back.

This is an ugly, ugly situation for which there is no simple solution. We have had a combination of an utter abdication of government and regulators coupled with a get rich quick/money for nothing mentality permeating our collective national psyche compounded with a generation of quasi-sociopaths participating in the scheme (see Casey Serin). I think that how we collectively respond to this crisis (and despite what the media and government say, it will be a crisis) will profoundly influence the US for the next 50 years.

Many commentators assume that we can simply inflate our way out of this mess. They look back to the 1970’s and the era of “stagflation” and presume that that is our path. They think we can (and will) walk that inflation path again. Inflation was rampant and pervasive then but so were wage increases. There is nothing (NOTHING) that leads me to believe that there will be a commensurate increase in wages if (when?) inflation occurs. Unions existed and had COLA clauses; when the union wages went up, so did everyone else’s.

Today, it’s too easy to ship work to China, India , Singapore , Vietnam, etc. or to bring in cheap labor from Mexico or Central America (I hate to say it, but it does sound like Marx’s reserve army of the unemployed). If inflation comes without commensurate wage increases, the traditional income/price ratios may return – but most families will need every dollar to pay for food, shelter, taxes and other day to day necessities. I’m most worried that if we’re not careful in how we respond (and I have no faith that we will be careful), we risk impoverishing the entire nation except the upper 1-2%. Virtually no one will be exempt.

If you watch the comedy “That 70’s Show” and look past the humorous interplay between the teenagers, there’s a tremendous undercurrent of angst. Red (one of the main characters) loses his good, full time job working in manufacturing and goes to work for a “superstore” at substantially reduced wages. Mom works. The neighbor owns a furniture store: he goes bankrupt, loses his store and home and then gets divorced. Cars are old. Clothes are plain. Meals are cooked at home. The kids hang out in the basement and watch TV for entertainment. No BMW’s. No designer clothes. No expensive restaurants. No exotic vacations. It’s actually quite realistic of how it was – and a warning of the true standard of living that stagflation and the initial stages of de-industrialization wrought. It could also be a harbinger of our stagflationary future.

Kip later added this price history and note:

I checked Property Shark (an even better website than Domania) on the second house I mentioned. Here's the transaction history:

7/97 -- $295K

4/00 -- $495K

3/06 -- $930K

8/06 -- $985K

7/07 -- $833K

The last transfer was to First Franklin Mortgage, so it appears to be a default on the 8/06 sale.

Excellent commentaries one and all, with a wealth of thoughtful points well made. Thank you, Harun, K.K., Michael, L.S. and Kip.

I would like to add one point not mentioned elsewhere here, which is that the majority of failed thrifts were located in Texas. Why did so many fail? Some causes have been listed above, but another is oil: specifically, the collapse in oil prices in the mid-80s which gutted the Texas economy and made all those condos, subdivisions and commercial buildings which had been thrown up with all that easy S&L money essentially unsellable at anything but truly fire-sale prices (10 cents on the dollar, etc.).

Which is to say that the long tentacles of coal/petroleum extend into all places on the planet, and have since the mid-1800s.

Readers, please be safe if you're traveling this holiday season, and I'll rejoin you here on the 24th or 26th.

Holiday gift bonanza:

Recommended Books and Films, many of which have been recommended by readers. (Here is the URL: http://www.oftwominds.com/books.html )There are over 250 titles and films organized into topics ranging from finance to Hapas/mixed-race Americans to World War II to world history to China to Italian cooking to gardening to novels to ideas to you-name-it, plus a number of wonderful films, many recommended by fellow readers.

Thank you, Don E., ($10), for your astonishing ninth contribution to this humble site. I am greatly honored by your readership, film recommendations and support. All contributors are listed below in acknowledgement of my gratitude.

Wednesday, December 19, 2007

Paging Mr. Scrooge

Here's a Christmas thought: Americans aren't just spendthrifts--they're wasteful, which is even worse. It's one thing for an entire nation to have a negative savings rate--spending more than its income--and quite another to have wasted much of that money on junk which is thrown away.

We share refuse and recycling facilities with college students attending one of the premiere public universities in the world. Many are from overseas, many are U.S.-born. If I didn't know better, I would assume such bright, well-educated young idealistic souls would be avid recyclers and careful with their money (or their parents' money).

Au contraire. The volume of complete, utterly shameless waste has staggered us. Just to recount recent throwaways which could have been given away with extremely modest effort: three unopened bags of Halloween candy; new untouched box of expensive Tazo tea; apparently new shoes; barely used or new T-shirts. The list goes on and on.

Over the years, we have noted that Europeans, Asians and first-generation students tend to waste less, while young American-born students (2nd generation and up) of all ethnicities, races and religions are in aggregate stupendously wasteful: of food, and everything else.

Yes, students are busy, especially those who hold jobs, too; but would it have been any extra work to carry the new candy to campus and drop it off at the department office, where it could have been placed in a bowl? Or how about walking an extra block to drop it off at the food bank? As for the new shoes and shirts, there is a Salvation Army store three blocks from campus. There's even an easier way to give stuff away in college towns: just place the shoes, etc. on the curb instead of in the trash.

Clearly, throwing stuff away is ingrained in Americans as the default setting of life. It simply doesn't occur to many Americans to recycle or make an effort to give away perfectly good items. Why? Because disposing of stuff in the trash apparently makes economic sense: Everything is just too cheap to bother with.

Many people in the U.S. spend perhaps 5% or 10% of their income on food; even with flour doubling in price, it's still ridiculously cheap. In countries where 50% or more of the family income is spent on food, you can be sure little is wasted.

Ditto for shoes, clothing, electronics, Ikea furniture, gasoline, and on and on: it's so cheap, it makes no sense to conserve it. And so we waste it, freely and easily and without a second thought. Even though there's a recycling bin a few feet away, plastic bottles, aluminum cans and glass containers are placed in the trash bin. You'd think recycling was some extraordinary effort, or something so new that college students hadn't yet grasped the concept. Yet the concept has been around for 37 years--and the concept of it being shameful to waste has been around much, much longer.

To return to the difference between spending money you don't have and wasting money you don't have: If every American family which spent beyond its means had purchased, say, solid oak furniture instead of a big-screen TV and Ikea particle-board garbage "furniture", then in 50 or even 100 years, that solid oak furniture would still be serving someone somewhere.

But alas, the TV will be in the dump in a few years, as will the rusty BBQ grill, the rusty cheap bicycle, the collapsed Ikea particle board, and virtually everything else Americans have borrowed to buy in the past debt-fueled decade of "prosperity," including entire shoddily-constructed houses.

It almost goes without saying that the food you will find tossed in the trash in the U.S. is never the chips or snacks or frozen convenience food: it's always the fresh food which is tossed out, untouched and uneaten.

Last night I made a pretty decent ratatouille (feeds four) for a few dollars. The beautiful zucchini was from our garden, the beautiful eggplant from a bag of five on sale for a dollar or so, and the onion and garlic were purchased at an ethnic market (we shop at Mexican, Indian, Asian and Halal markets) for what amounts to a few dimes each. The French feta cheese generously sprinkled on top at serving cost another few dimes. The whole wheat bread, a dime or so per slice.

The total cost of this meal was a few dollars, even if you bought the zucchini. And yet the media is filled with stories about how expensive real food is now, and how fast food is cheaper than real food. Are we truly this insane? Last time I checked, a "value meal" at a fast food outlet costs about $4. Four meals adds up to $16--a far cry from $2-$3 for a delicious and healthy ratatouille which would set you back $12+ per serving in a restaurant.

What really troubles me is the value of "waste not want not" has been largely lost in our culture. (The Japanese phrase is "motainai.") The sentiment that it is wrong or even sinful to waste, especially food, is not unique to any one culture; it arose from a life of scarcity. Now that everything is so cheap, we can throw away and waste resources at a prodigious rate because it still makes "economic sense" not to bother with conservation or careful use of resources.

If trash was hauled off and paid for by the pound, would people start recycling more? Perhaps. When gasoline is $5/gallon, will people start conserving it? Perhaps. But perhaps not. Perhaps profligacy is so deeply embedded in American culture that we as a people will only whine about the "high cost" of things as we struggle to pull our overloaded trash bins to the curb, alongside the dead TVs and broken shelving awaiting delivery to the landfill. As we hurry off to buy a "cheap" fast-food meal, having left a binful of fruit and vegetables rotting in the garbage, we'll focus our most strident complaints on the high cost of food, not on what we have wasted so needlessly and recklessly.

Holiday gift bonanza:

Recommended Books and Films, many of which have been recommended by readers. (Here is the URL: http://www.oftwominds.com/books.html )There are over 250 titles and films organized into topics ranging from finance to Hapas/mixed-race Americans to World War II to world history to China to Italian cooking to gardening to novels to ideas to you-name-it, plus a number of wonderful films, many recommended by fellow readers.

Thank you, Steve J., ($20), for your very generous contribution to this humble site. I am greatly honored by your readership and support. All contributors are listed below in acknowledgement of my gratitude.

Tuesday, December 18, 2007

Bailout: Could Government Actually Be Part of the Solution?

Thoughtful reader Robert Roth sent in some cogent comments in response to Saturday's entry on renegotiating mortgages. He raises many important issues about the mortgage crisis which tend to get brushed aside by blanket condemnations of any bailout.

I am not predisposed to any bailout, but intellectual honesty requires me to recall that the much-maligned "bailout" of Chrysler in the early 1980s saved the company and tens of thousands of jobs at modest (or according to Lee Iacocca, zero) government funds.

Though it was obvious the Savings and Loan collapse in the 80s was caused largely by Reagan-era deregulation of an industry which simply requires some regulation--that is, the crisis was predictable and easily avoidable--the horrendously expensive bailout did resolve a financial crisis which could have festered for years. Though the government covered depositor's money, the primary tool used to clean up the mess was auctioning of/ liquidating all the impaired properties--thousands of buildings around the country.

So all the bailout ideas require an honest analysis. Let's start with Robert Roth's commentary:

"L.S. recommends that people under threat of foreclosure try to work it out with their lenders. I have read in several places that that approach is problematic because in many (most?) cases, the people who collect the payments don't even know who holds the mortgage -- that precisely the complexity and opacity of the securities backed by these mortgages makes impractical the old-fashioned way of addressing the problem that L.S. suggests. If I'm wrong about that, I'd love to hear it, and wish someone would say so and why.

And while I agree folks in trouble shouldn't wait for a government bailout, I also think that to save everything from the homes of a great many unfortunate (even if some profligate) people to the global financial system and real economy, we should demand a government bailout commensurate with the size of the problem.

Today (12/15-16)'s WSJ cites the proposal of "Center for American Progress, a liberal think tank ... that the government buy some mortgage-backed securities and create a new agency, the Family Foreclosure Rescue Corp. [to] issue new, more affordable fixed-rate mortgages for those facing foreclosure whose homes are worth less than what they owe," and that of Alex Pollock, a resident fellow at the American Enterprise Institute, who says take a look at the history of Home Owners' Loan Corp, a now-defuncy federal agency created in 1933 that "acquired distressed mortgages from banks at a discount and refinanced them on easier terms."

Both ideas sound promising to me. So do preemptive tax cuts implemented by reducing payroll taxes immediately so as to put some cash into the hands of consumers, who carry two-thirds of the economy and seem to be sagging under its weight and quite likely about to drop it.

Perhaps it would be worth adding another point: I recall reading in the WSJ years ago that the French government, to combat an economic slowdown, was offering interest-free mortgages to first-time homebuyers. I suspect there are many more potential solutions if we were able to transcend the democracy deficit as a result of which relief is targeted to the Big Boyz (as I believe Jim Kunstler calls them) rather than the rest of us.

Paul Krugman's December 10, 2007 piece entitled Henry Paulson's Priorities argues that the Paulson proposal is intended only to create the appearance of action -- while helping some investors, but not families losing their homes -- "thereby undercutting political support for actual attempts to help families in trouble," in particular, probably, "legislation sponsored by Barney Frank that would give judges in bankruptcy cases the ability to rewrite mortgage loan terms. ... 'Bankers Hope Bush Subprime Plan Will Scuttle House Bill,' as a headline in CongressDaily put it."

Properly empowered, by the way, the bankruptcy courts may have considerable potential to examine transactions in more detail than would otherwise be possible. Then there's your own blog entry The Unintended Consequences of the Housing Bubble Bursting citing the December 10th SF Chronicle article which suggested the Paulson proposal is intended to shield Wall Street firms from lawsuits by foreign investors challenging the basis of the interests they'd been sold in CDOs, etc. as fraudulent in origination."

Any bailout is a complex thicket, so let's start with what we can safely surmise:

1. The political process will be slanted toward major contributors, i.e. the banking, real estate and lending industries. This should not surprise us in the least. Nonetheless, history suggests (i.e. the Depression-era Home Owners Loan Corp. mentioned above) that occasionally some political "interference" may have some value beyond helping the Big Boyz preserve their capital and profits--though of course any bailout must accomplish this first.

2. There will be political action of some sort because "we have to do something." Former Fed Chairman Greenspan has come out in favor of tax cuts for the imperiled borrowers, a proposal which is essentially meaningless because most of those borrowers probably wouldn't save enough in any such proposal to make a dent in their mortgage payments.

In this sense, the proposal will be largely ineffective but also relatively harmless.

3. We can safely assume about 25% of distressed buyers were speculators who never occupied the house, i.e. "flippers." A recent San Francisco Chronicle study found Investors own about one-fifth of Bay Area homes in foreclosure but the methodology was extremely conservative and so 25% seems fair. but the methodology was extremely conservative and so 25% seems fair.

Let's guesstimate that another 50% of distressed properties were purchased by buyers with little or no "skin in the game," i.e. down payment. The S.F. Chronicle study found that about 70% opf subprime buyers in 2005-2006 put no money down. Thus, these people will lose virtually nothing in foreclosure because they brought nothing to the party in the first place.

So when the mess is settled by market forces, i.e. auctions etc., the primary losers will be speculators (whom no one expresses interest in saving) and the lenders and buyers of CDOs, SIVs, mortgage-backed securities, etc. (ditto).

4. The primary lesson of the 1980s S&L bailout is: move quickly to liquidate bad debt via market auctions of distressed properties. In extremely overbuilt, investor-fueled markets like California's Central Valley and Las Vegas (to name but two of many), there may be no buyers at lender-run auctions; but the market solution is simple: lower the price until buyers emerge, even if the price is $1.

In extremely depressed areas such as certain neighborhoods in Detroit, houses don't sell even for $1. In these cases, Nature takes over the neighborhood and/or the city bulldozes the vacant, decrepit homes. This is sad, but you can't force people to live somewhere, or artifically inflate prices or economic vitality.

If we set aside these outliers, most distressed property in economically viable areas can be sold, albeit at huge discounts. Thanks to a steady flow of "on the ground" intelligence from readers all over the country, I can report that buyers--not just professional investors, but wage-earners looking for investments/places to live--will come out when the price is right.

Within the last few days I have heard from readers who are planning to bid on properties which are being auctioned off (foreclosure/REO auctions) or considering buying a home in areas which never experienced the bubble rise and therefore aren't experiencing the bubble popping.

Since readers of this site are a priori fiscally conservative and savvy, :-) I think these potential buyers are evidence that not everybody is an underwater owner of a negative-equity home. One reader is considering paying the 10% penalty to extract some 401K money which is limited to stock market mutual funds in order to purchase property. If the stock market tanks as severely as many of us expect in 2008-2011, this will be seen in retrospect as a very savvy move.

5. As Mr. Roth suggests, the courts could step in and make a substantial contribution to rapid resolutions of bad debt and distressed properties. The courts are a wild-card because the Supreme Court could always step in and protect lenders and investors (domestic and foreign alike) from losses, but the bankruptcy laws have quite a bit of case history and may yet serve as a "clearing house" of sorts.

6. From one view, it can be argued that since government enabled the entire bubble via lack of lending/investment banking oversight (once again), it should be part of the solution. Again, I am not talking about using tax money to bail out hopeless mortgages, I am talking about a government-sponored auction of debt and properties along the lines of the Resolution Trust Corporation which cleared up the S&L mess in the late 80s/early 90s.

It's certainly something to consider, especially when we recall what happens when the government colaborates with lenders to cover up the losses, as the Japanese government has done for the past 17 years: you get 17 years of stagnation and deflation, and ballooning government deficits.

Holiday gift suggestion:

If Amazon.com gift certificates work for you, go for it through this link.

If you think it might be of interest to the recipient, you could also forward my list of Recommended Books and Films, many of which have been recommended by readers. (Here is the URL: http://www.oftwominds.com/books.html )There are over 250 titles and films organized into topics ranging from finance to Hapas/mixed-race Americans to World War II to history to Italian cooking to gardening to novels to ideas to you-name-it, plus a number of wonderful films, many recommended by fellow readers.

Thank you, John H., ($50), for your very generous contribution to this humble site. I am greatly honored by your readership and support. All contributors are listed below in acknowledgement of my gratitude.

Monday, December 17, 2007

Stock Market Santa Claus: Rally or Lump of Coal?

Santa seems to be wavering about delivering his annual stock market rally to Wall Street. Little wonder, given the tapped-out consumer and the resulting inevitability of a consumer-real-estate-bust-global-overcapacity recession. But before we write Santa off completely, let's look at some charts: (see below)

The VIX (Volatility Index) moves inversely to the markets; when volatility spikes up to a peak, that usually marks a market bottom. When it drops to a low, that corresponds to a market top.

And just to confirm the wedge/pennant formation, here is the Nasdaq:

These wedges or pennants are rather obvious formations, and they typically break up or down in a big way. There are certainly may fundamental reasons to believe the market will break down--recessions usually bring declines in corporate earnings, etc.--but there are technical reasons to believe Santa gave the market a head-fake last week and is loading the sled with a rally.

You can see the market wavered in a very similar wedge in September, and even offered up a similar head-fake, i.e. MACD appeared poised to roll over into a "sell" signal. Yet the stochastic is oversold, suggesting the down move of last week has run its course. MACD is neutral, suggesting the market could move up or down.

One factor which is occasionally worth considering is how the options market is reflecting the overall market's sentiments. The cliche is that 80-90% of all options expire worthless; many options are purchased as hedges, and their expiration was expected.

With that said, the market rarely rewards bets held by 80% of the players. Right now there is a huge imbalance between puts and calls in the financial stocks like Citicorp (C), Washington Mutual (WM) and Countrywide (CFC). There are 3 or 4 puts (bets the stock will decline) for every call (bet the stock will rise). This tremendous imbalance suggests to me--and please note this is merely a wild opinion-- that the financials are poised to explode upward, rendering all those puts worthless.

Why? No reason; just that's the way it usually works. When four punters line up to bet that "these wretched financials are doomed to huge declines" for every punter gambling that the financials' demise is somewhat premature, the market typically takes the four punters' money and rewards the sole punter.

Since wedges generally break big up or down, it should be an interesting week.

The VIX (Volatility Index) moves inversely to the markets; when volatility spikes up to

a peak, that usually marks a market bottom. When it drops to a low, that corresponds to

a market top.

And just to confirm the wedge/pennant formation, here is the Nasdaq:

Holiday gift suggestion:

If Amazon.com gift certificates work for you, go for it through this link.

If you think it might be of interest to the recipient, you could also forward my list of Recommended Books and Films, many of which have been recommended by readers. (Here is the URL: http://www.oftwominds.com/books.html )There are over 250 titles and films organized into topics ranging from finance to Hapas/mixed-race Americans to World War II to history to Italian cooking to gardening to novels to ideas to you-name-it, plus a number of wonderful films, many recommended by fellow readers.

Thank you, Eugenio M., ($20), for your second generous contribution to this humble site. I am greatly honored by your readership and support. All contributors are listed below in acknowledgement of my gratitude.

Saturday, December 15, 2007

Reader Commentaries and Christmas Gift 'Hail Mary'

We have some great reader commentaries on this week's topics, but first let's get through a hopefully-only-slightly-annoying Christmas gift pitch.

If you're a wonderful gift-giver and enjoy shopping, please skip this section. If you're a lame gift-giver who loathes shopping like myself, read on. Dear fellow lame gift-givers: yes, this is the season we dread: what to give people we care about? Ugh, yikes, horrors, etc. My solution is candy, books and gift certificates, but with people's health so poor nowadays I can only give chocolates to a few people without feeling like I'm undermining their resolve/health. But books are always a joy; and if we guess wrong, the recipient can pass it on to another reader. Better yet, give them a gift certificate and let them pick their own books.

Here's the usual disclosure found elsewhere on this site: if you buy anything from amazon.com via this site, I receive a small sliver from amazon. You pay nothing more than if you went to amazon.com through a new browser window.

So if Amazon.com gift certificates work for you, go for it through this link. The gift certificate is what I call a "Hail Mary" gift, for as in the fourth-down and seconds-left-to-win football play of the same name, it is a desperation toss which occasionally works despite the odds.

If you think it might be of interest to the recipient, you could also forward my list of Recommended Books and Films, many of which have been recommended by readers. (Here is the URL: http://www.oftwominds.com/books.html )There are over 200 titles and films organized into topics ranging from finance to Hapas/mixed-race Americans to World War II to history to Italian cooking to gardening to novels to ideas to you-name-it, plus a number of wonderful films, many recommended by fellow readers.

Here are a few titles recommended by readers that I recently read with pleasure--among dozens of other excellent suggestions:

Here are a few titles recommended by readers that I recently read with pleasure--among dozens of other excellent suggestions:

The Year the Music Died, 1964-1972: A Commentary on the Best Era of Pop Music, and an Irreverent Look at the Musicians and Social Movements of the Time (recommended by reader Charlie R.)

Goodbye to All That (a classic memoir of World war I recommended by reader Lloyd L.)

Manias, Panics, and Crashes: A History of Financial Crises (recommended by reader U. Doran)

The Shock Doctrine: The Rise of Disaster Capitalism (recommended and donated by Faith A.)

Other books I have recently read and have added to the recommended list:

The Sense of Being Stared At: And Other Aspects of the Extended Mind

The Contractor (fiction)

Walk On, Bright Boy (fiction)

The Hero and the Outlaw: Building Extraordinary Brands Through the Power of Archetypes

The Oxford Companion to Ships and the Sea

(this isn't a book you read straight through but browse through at your leisure)

We now return you to our regularly scheduled programming.

Here are two very thoughtful commentaries on the 12/14/07 entry entry The Politics of Atomization:

J.D.:

The "politics" of atomization is an interesting way of framing this topic.

This frenzied lifestyle reminds me of "on the beach" - a cold war era short story about a sub commander that takes a post-apocalyptic trip down under to be with the last humans alive. The towns people he ultimately encounters all react differently to the sands draining out of the hour glass. Some retreat, some freak out.

I think the befuddled masses are going to be "shocked and awed". They are going to go through the stages of grief and get stuck on anger, and I am afraid, become suseptible to demagogery and authoritarianism. Ursula Hegi in Stones from the River depicts in fine detail the short slide the German people took the very instant they struck the bargain that "we" will be OK, because they are only after the communists, gypsies, Jews, etc. Hegi's point is that once you accept the incarceration of one among you, you yourself have already surrendered.

And here I am writing to you, because you can't bring this up at the proverbial water cooler without being chastised for being either a downer, or a crackpot. In the land of the blind, the one eyed man is not king, he is noise interfering with the signal of cognitive dissonance, No?

L.S.:

Charles – another excellent, albeit sadly true essay.

"Self-reliance is a major American value, as is "the buck stops here" acceptance of responsibility. Great stuff, these values."

I’ve always been on board with this sentiment – maybe even to the point of being a bit of a scold. But this time I have to admit things got beyond the limits of simple self restraint. My analogy has been that lenders have simply thrown money into the air and encouraged people to bid up the price of housing, perhaps even with the tacit understanding that large scale fraud was being committed.

So what’s the result? Young families with kids see themselves forever priced out of the market unless they make a deal with the devil. My heart aches to think of the spiral of destruction that lays ahead for these families. I can already picture the angry exchanges, the divorces – children not only losing their home, but their family as well. It always gives my heart a twinge when I see a swingset or sandbox in the yard of a foreclosure. What did that family go through before they were forced to move?

So what to do? Well I think the 80/20 rule applies here. The lenders are culpable for at least 80 percent of the mess, so they deserve to clean up after the elephants in this parade. But these are just words - how about some action? Here’s what I’m doing.