American Empire I: Did the American Revolution Trigger World War I?

In a conversation yesterday on World War I, my good friend Jim E. suggested an astonishing but thought-provoking thesis: that the anti-monarchist American Revolution of 1776-1781 precipitated a century-long anti-monarchist trend which led to Kaiser-dominated Germany facing off against the democratic Allies of France and Britain.

Jim also recounted the various secret machinations both sides went through to undermine their opponents: Germany supported the anti-czar Lenin and anti-British forces in Ireland and Africa, and even went so far as to prod Mexico to consider invading the U.S. The Allies of course had their own intelligence forces at work around the globe, including Lawrence of Arabia, whose job was to foment revolution in the Ottoman Empire, an ally of Germany.

None of this was known to the general public on either side. Propaganda reigned supreme, with each side demonizing the other to flog the populace into continuing sacrifices of life and treasure.

Two other forces were at work, undermining monarchy beneath the surface: literacy and communication. The American Civil War was the first modern war in the terms of railway logistics, ironclad warships and many other innovations, but it was also the first modern war in the sense that the majority or participants knew how to read and there were newspapers and telegraphs to insure rapid and wide dissemination of war news.

The first imperative of any dictatorship/monarchy is to control the flow of news and ideas. A literate, well-informed populace is the natural enemy of monarchy and dictatorship, as Hitler well understood. After its brief, aborted lurch into democracy (recall that Hitler gained power via a free election), Germany renewed its love affair with dictatorship and centralized power, as did Japan.

Just as the American Revolution set the stage for World War I, WWI set the stage for World War II. With the complete and total defeat of both Axis powers, monarchy in the West was finally destroyed as a political and cultural force.

The American Civil War played a role in World War I as well. On one level, the war was about slavery, the deep, unanswered conflict papered over by the Constitutional Convention. But on another level, it resolved the lingering conflict between states rights and the Federal, centralized government.

The modern state capable of global reach and war is by nature centralized. Only by mobilizing an entire modern economy can any nation project power and protect the trading lanes and outposts which generate most of any global economy's net profits.

Before the American Revolution, every major government in the world was a monarchy. Afterward, European powers were drawn to dismantle or limit monarchies one way or the other; France convulsed in multiple revolutions and swings from democracy to monarchy, while Russia went down the path of the "dictatorship of the proletariat."

In this long view, the entire Cold War was a continuation of the long trend of democracy undermining and then replacing monarchy. The Soviet Union and Maoist China essentially lost the Cold War (along with North Vietnam and North Korea), and all but the latter have undergone slow, as yet incomplete transformations from dictatorships to more open societies and economies. Their transformation is still a work in progress.

In this context, it is well to recall what Chou En-Lai replied when asked about the impact of the French Revolution: "It's too soon to say." In other words, from the long perspective of Chinese history, it was too soon to say in 1970 what the full outcome of the 1790s revolution would be.

That is to say, we are participants in and observers of very long-term trends. From at least one point of view, the Iranian Revolution of 1979 was the (abortive) attempt by the Iranian people to replace their monarchy with a more open, more democractic government. (Their first attempt in 1953 had been foiled by a C.I.A.-funded coup which brought the Shah's father to monarchist power.)

How will the American involvement play out in Iraq? It is definitely too soon to say. Recall that U.S. troops remain in Japan and Germany, 60 years after their defeat, largely to insure their neighbors that the former Axis Powers will never be allowed to slip back into fascism and aggression.

As easy as it is to mock "nation building" and "democracy" in the chaos the U.S. has unleashed in Iraq, the genie is definitely out of the bottle in one supremely fundamental way: the media is gloriously, rampantly luxuriously free in Iraq. Let a thousand flowers bloom, indeed; by all accounts, newspapers and flyers arise and fade at a dizzying rate. With high literacy and a free press, Iraq is now under the sway of the long-term trend away from monarchy and dictatorship which has influenced every nation for the past 200+ years.

In a peculiar way, Iran and Iraq may well be bound up in a very long-term, largely hidden process of moving away from monarchy and oligarchy toward more open, more deomocratic societies. In this, they are simply following the global trend which has already been in place for hundreds of years.

We should also note that machinations don't work long-term. Supporting coups and terrorists never truly turn the tide back to monarchy and closed societies; at best they delay, at frightful cost, the inevitable.

In this sense, the entire notion of "empire" becomes suspect. More on that tomorrow.

NOTE: contributions are humbly acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Reed H. ($20), for your generous donation in support of this humble site. I am greatly honored by your contribution and readership. All contributors are listed below in acknowledgement of my gratitude.

Thank you, Cyril O. ($100), for your astoundingly generous donation in support of this humble site. I am greatly honored by your contribution and readership. All contributors are listed below in acknowledgement of my gratitude.

Thursday, January 31, 2008

Wednesday, January 30, 2008

We Told Ya So--But So What?

I had to chuckle at the breathless February 4 BusinessWeek feature: The Economy: How Real Was the Prosperity? The Economy: How Real Was the Prosperity?

Why? Take a look at these entries I wrote way back in September 2005 and January 2006:

Adios, O Bogus Prosperity (9/17/05)

Once More, With Feeling: This Is False Prosperity (1/31/06)

How did a poor dumb writer like me (and many other bloggers) beat BusinessWeek's huge staff of professional journalists like a gong, getting the story they are just now addressing by over two years?

Your answer, whatever it may be, says volumes about the pathetic cheerleading state of the mainstream financial media.

What's even more stunning is that the BusinessWeek story ran charts which are eerily similar to charts you've seen on the Web for years--there's absolutely nothing new in the BW story except the tacit admission of journalistic incompetence that the "story" was ignored until events forced BW's hand.

OK, you were right. Nice. But what have you done for me today? Jeez, what a demanding audience! A guy can't even rest on his laurels. So you want a snapshot of the future? I can't provide that, but let's start with a quote from one of the great traders of all time, George Soros:

"Economic history is a never-ending series of episodes based on falsehoods and lies, not truths. It represents the path to big money. The object is to recognize the trend whose premise is false, ride that trend, and step off before it is discredited."

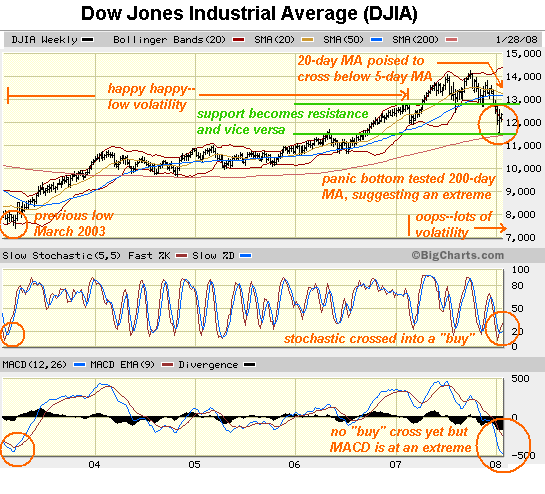

So what's the trend now? It's been down as the mainstream media and various other players have caught on to the inevitability of recession. But a reversal--yes, a trend whose premise, that everything's not as bad as we thought, is false--may well be working its way to the surface. Consider this 5-year chart of the Dow Jones Industrial Average:

Looking at the economy, the skeptic would wonder how the stock market could rally. That's where Mr. Soros steps in to remind us that traders aren't interested in the economy per se, they're interested in the trend. And there are various signals (stochastic cross, MACD extreme, widening Bollinger bands, etc.) which suggest the downward trend of the past few months may well reverse.

For how long? Until the trend reverses. Of course the market could swoon once again and even retest the 11,500 level in the short-term. But this long-term chart suggests a primary trend reversal is becoming likely.

It is frustrating to a fundamental analyst to be told the market has virtually no relation to reality or the truth; it should, it should! But alas, it doesn't. The economy stinks, but if the DJIA clears resistance around 12,800, it could conceivably hit a new high. Is that a prediction? No, just a way of saying the trend goes on until it reverses.

As Mr. Soros put it: "The object is to recognize the trend whose premise is false, ride that trend, and step off before it is discredited." We would do well, I think, to ponder that, even if it runs counter to what we currently believe.

Readers Journal has been updated! New comments by Michael Goodfellow and others have been added:

Readers commentaries

NOTE: contributions are humbly acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Kelly M. ($25), for your generous donation in support of this humble site. I am greatly honored by your contribution and readership. All contributors are listed below in acknowledgement of my gratitude.

Thank you, Michael S. ($15), for your much-appreciated donation in support of this humble site. I am greatly honored by your contribution and readership. All contributors are listed below in acknowledgement of my gratitude. Read more...

Tuesday, January 29, 2008

The Debt/Real Estate Orgy: Two Metaphors

Astute reader David V. sent in a story which he suggested was ripe with metaphoric possibilities: 19 bald eagles die in Alaska:

At least 19 bald eagles died Friday after gorging themselves on a truck full of fish waste outside a processing plant.

Fifty or more eagles swarmed into the truck, whose retractable fabric cover was open, after the truck was moved outside the plant, said Brandon Saito, a biologist with the U.S. Fish and Wildlife Service who coordinated the recovery operation.

The birds became too soiled to fly or clean themselves, and with temperatures in the mid-teens, began to succumb to the cold. Some birds became so weak they sank into the fish slime and were crushed.

The truck's contents had to be dumped onto the floor of the Ocean Beauty Seafoods plant so the birds could be retrieved. Some tried to scatter, but since they couldn't fly, wildlife officers soon retrieved them. The eagles were then cleaned with dish soap in tubs of warm water to remove the oily slime and warm them.

Could anyone dream up a more apt metaphor for the debt/real estate offal which America has gorged on the past seven years than this? Let's see: the Bald Eagle is the symbol of the U.S.A.: check. Fish waste = no-document, no down payment mortgages, check. The orgy left participants unable to escape the slime, check. Some participants weakened and were subsequently crushed, check. Government officials hurried to aid the entrapped participants in the hopes they would recover, check.

Whew. It doesn't get any better than this in Metaphor-Land. Thank you, David, for bringing this amazingly rich story to our attention.

Illness and medical metaphors are, along with war metaphors, easily overextended. (Consider the "War on Cancer," a two-fer.) Nonetheless, it is tempting to draw an analogy between the spreading debt crisis and an infection.

Not just any infection, but a special kind--the self-induced infection. Since we're stretching metaphors to the breaking point, let's run with "self-induced financial infection."

Metaphorically, here's how The global financial system managed to infect itself:

Having consumed nothing but Big Macs and Jack Daniel whiskey for a deplorably long time, Mr. GFS's (global financial system) judgment and health were already impaired when he stumbled upon an open vat of sewage-soaked, apparently "free" money. Like the ravenous eagles pitching themselves voraciously into the fish offal, Mr. GFS climbed in and gleefully cavorted in the smelly cash, ignoring his numerous open sores and abrasions and poor state of mental and physical health.

Alas, Mr. GFS eventually sneezes, then coughs, and in the first stages of multiple infections--let's say staph, pneumonia, influenza and multiple other microbal meanies--he crawls out of the oderiferous bin and whines, "I'm sick! How could this happen?"

How, indeed, when every reasonable caution was thrown to the winds of insatiable, frenzied greed and euphoria-impaired judgment?

The "self-induced infection" of miscalculated and mispriced risk, overleveraged debt and deeply underwater real estate is systemic. Although I cannot locate the source, I recently read that homeownership rates leaped throughout Europe in the housing boom. This suggests that millions of previously unqualified buyers purchased properties at the top of the market in much of the E.U., just as millions of unqualified buyers jumped into the orgy in the U.S. and Asia.

In other words, the infection is global. I have written numerous times about the empty condo buildings in China, and the government employees in China I know of firsthand who each own three or four investment condos (some rented, some empty, all leveraged). Astute reader Mega sent in this link to an excellent Britain-based site, Housepricecrash.co.uk. Similar sites can be found for Spain, Ireland, etc.

Alas, the medications being pumped into the system are only suppressing the symptoms, not the infection. Pumping in more liquidity, raising Fannie Mae loan limits, freezing mortgage rates, even switching hopelessly underwater ARMs to fixed rate loans--all of these measures skirt the primary issues: misguided risk management, plummeting bubblicious valuations and borrowers who are unable to service their loans, regardless of the tweaks being made to their debt.

The "cure" being offered is essentially the cause of the disease: more debt.

This is the "cure" which enabled Japan to enter a self-induced economic coma for most of the past 20 years. Can't service your loan? Hey, we'll rewrite it for a larger sum so you can use the difference to pay interest. Or, we'll rewrite it at a lower interest rate and arrange for a subsidiary loan from another lender that we're colluding with to hide the true nature of the debt. Or we'll set it aside in some dark, hard-to-find corner of our balance sheet for a few years, or maybe a decade.

We can safely predict the self-induced infection has not yet run its course. Housing underpins most middle-class Americans' wealth, and their collective sense of wealth. But the credit orgy extends far beyond housing, of course, and the infection is already breaking out in auto loans (and their credit-based derivatives), credit cards, commercial real estate loans, and indeed, all debt, everywhere.

Readers Journal has been updated! A wealth of new comments and ideas await you:

Readers commentaries

How our Parents Shopped

Monoline Insurance and Financial Fear

The Three Little English Pigs

A New Regulatory Idea

--------------------------------------------------------------------------------

NOTE: contributions are humbly acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Knowel M. ($50), for your amazingly generous donation in support of this humble site. I am greatly honored by your contribution and readership. All contributors are listed below in acknowledgement of my gratitude.

Thank you, D.M.T. ($25), for your generous cash donation in support of this humble site. You did not include a full street address, and I am unable to locate your email address, so please accept this modest thank-you. I am greatly honored by your contribution and readership. All contributors are listed below in acknowledgement of my gratitude.

Read more...

Monday, January 28, 2008

A Great Depression, or Simply a Return to Normal Life?

Imagine living without electricity, radio or television. No, I don't mean camping for a few days, I mean everyday normal life. Imagine not having a car, and walking on unpaved roads. Imagine tasting soda once or twice a year--not that you get the whole bottle to yourself, mind you--at a special event at church. Imagine lunch being a rice ball with a pickled plum. Imagine getting to go to town once a year, on the train, for the Fourth of July.

Until the last sentence you might have reckoned I was referring to some distant, poverty-gripped Third World country rather than to giddy, gung-ho "Roaring 1920s" America. Much of the above come directly from the memory of my wife's 90-year old aunt in Hawaii, Kay H. We were able to chat with Auntie Kay (and record some of her memories) at some length, as we spent the last week helping the family ready her house to be sold. Though she is in excellent physical and mental health for her age, her family understandably decided it would be better for her to move in with them.

Poverty is a relative concept. If you're cold, any source of heat is wealth. If you're hungry, any food is wealth. If you're truly penniless, any job is wealth. If you're in the dark every night, any source of light is wealth. If you have a kerosene lantern, then an electric light is wealth. And so on.

We know this intellectually, but consider this: what most Americans would consider utterly abject poverty was simply normal life to millions of non-urban, non-wealthy Americans in the booming 1920s. Although the first paragraph describes the everyday life of plantation workers in Hawaii, the same conditions existed throughout mainland America as well, often with the added burdens of extreme cold and drought.

I know from email communication that some readers have experienced severe hunger and poverty much more recently than 1928. Middle-class America tends to think of poverty as only existing in rural pockets or limited urban ghettos, but it can be found anywhere that migrant agricultural workers do their work--and that now means vast swaths of the U.S.

Setting aside the issue of how many of these workers are illegal immigrants for a moment, I ask you: have you seen the places these workers live? I don't mean the occasional Potemkin Village of shiny new housing, I mean the shacks in rural Oregon, California, and dozens of other agricultural zones where for whatever reason the locals don't pick the crops any longer. Yes, some outstanding farms provide adequate housing, but many do not.

The average middle-class American is suburban and thus he or she never sees the primitive living conditions endured by many of the people who harvested the crops that end up so nicely plastic-wrapped in Safeway. For many, the "solution" is to "ship them all back to where they came from." I am afraid these people are not living in agricultural country, or listening to agricultural realities, or even driving around and talking to farmers.

Have you ever picked strawberries all day? Have you ever gone to the unemployment office and announced some wonderful jobs are available picking oranges in the blazing sun for minimum wage, and seen all those hardy, willing U.S. citizens hurry over to board your truck?

My seatmate on the flight home from Hawaii was as astonished by my picking pineapple on Lanai as if I'd said I'd made stone axes. Pineapple is no longer grown on the Hawaiian island of Lanai, but even in 1970 when I was on the afternoon shift along with other high school boys, there was a "local labor shortage" in summer. At peak harvest season, there weren't enough permanent plantation workers or high school kids on summer break to pick pine.

The high school kids in urban Honolulu, it seemed, had no interest in walking through spiny fields in protective clothing beneath a blasting tropical sun all day (or until midnight, if you were lucky) for minimum wage (add a dime for the swing shift and a couple more bucks if your crew exceeded its estimated number of truckloads). As a result Dole Pineapple recruited Mormon youths (all males) from the Mainland and put them up in simple dorm rooms.

So I know what harvesting heavy fruit under a hot sun by hand means. This may sound harsh, but I bet if you assigned 100 unemployed native-born Americans (of any race, religion or gender) to this kind of work, I would hazard that you would be lucky if there were three left by the end of Week One. If you can prove me wrong in this, I would be delighted. But I would want to see verifiable statistics for three months, minimum. Remember, we're not talking about a week-long "adventure" trip here, we're talking about everyday life.

And you know what? Picking pine was a lot easier than harvesting sugar cane by hand. It was also easier than bending over picking strawberries, and easier than a lot of harvesting jobs. We had a union (the I.L.W.U.) and had regular lunch breaks and an 8-hour shift. This cannot be said of all modern-day American fruit picking crews.

In 1928, poverty was relative, too. Having a full rice bin or larder and a roof that didn't leak was wealth to most people.

You knew where this was going, didn't you? Yes, the upcoming Depression. How will today's youth (let's call them Kylie and Josh) handle life when Mom or Dad can no longer afford cell phones for every member of the family? What if the DishTV or cable gets cut off due to lack of payment? What if there's no longer a case of soda purchased every week? What if their allowance drops from $20 per week to zero?

And how about Mom and Dad? What if there's no money for the dog walker, or the kennel when the family dashes off for an exotic vacation? What if there's no money for the personal trainer, or the gym? What if money disappears to such a degree that latte-mocha- caramel-soy-milk-no-foam coffee drinks can no longer be enjoyed?

The ironic answer might well be, good riddance. It was all a fraud, all along--the bogus "prosperity" based on credit bubbles and vast borrowing, the gaudy worshipping of Shopping as the New Religion, the phony collection of gadgets and name-brand clothing, the idiocy of one excess after another, the reduction of the culture to the lowest level of Pop slime, the $100 per person "fine dining," and all the other trappings of sham "prosperity."

At this point few in the Mainstream Media are willing to even mention the possibility that a reduction in income and "lifestyle" may not be short-lived or limited in scope. It will be interesting to see, to say the least, what a relative impoverishment will do to the average middle-class American's psyche.

I know from email that many of you have worked in low-paying, difficult jobs, and that many more of you have chosen to live a simple, low-energy-use lifestyle based on frugality and good living (yes, those two concepts do actually go together). I honor your hard work, and your memories of those low-income days, and I applaud your reject-the-excesses lifestyle.

When does a "reduced lifestyle" reach absolute (as opposed to relative) poverty? When the larder is empty and the roof leaks and nobody has a job. But if "poverty" means the household only gets pizza once a week--well, that is still wealth almost beyond imagination.

For another excellent look at a simpler time--the 40s and 50s--please read Protagoras's new essay, How our Parents Shopped. It will be eye-opening to anyone under the age of 40.

Readers Journal has been updated! A wealth of new comments and ideas await you: Readers commentaries And four new excellent essays--three by Protagoras, and a thought-provoking look at bank regulation by Oliver King-Smith:

How our Parents Shopped

Monoline Insurance and Financial Fear

The Three Little English Pigs

A New Regulatory Idea

NOTE: contributions are humbly acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Nathaniel H. ($5), for your much-appreciated donation in support of this humble site. I am greatly honored by your contribution and readership. All contributors are listed below in acknowledgement of my gratitude.

Friday, January 25, 2008

Are You On the TSA Watch List, Too?

Does the U.S. need to harden its transportation, infrastructure and border security? No reasonable person would answer "no." So then the question becomes: how to you effectively do this, as opposed to ineffectively wsting a lot of money and staffing on essentially useless procedures?

And that takes us to the Transportation Security Administration (TSA) Watch List. The TSA is tasked with airport security, which is why all the screeners at airports wear uniforms with "TSA" emblazoned on the back.

While there are a number of disturbing reports about harmless/innocent travelers being harassed by TSA employees floating around the Web, I haven't personally encountered any such behavior. My focus today is not on abuse of travelers (certainly a valid topic) but on the absolute stupidity of the Watch List, of which I am a select member.

Or maybe not so select. Apparently the List contains thousands of names, the vast majority of whom have absolutely no connection to terrorism--and there is not a scintilla of evidence which would justify their inclusion on a list of "potential threats" or "persons of interest" to U.S. intelligence and security agencies.

Want to find out if you're on the TSA watch List? It's easy! Just try to print a boarding pass on your home computer. If you can't--after you've bought the ticket, and selected your seat, and clicked all the appropriate buttons--then guess what: you're on the Watch List!

Or more precisely, your name is on the Watch List. I first discovered my inclusion on the Watch List last summer when I couldn't print a boarding pass at home, or at the airport kiosk. This was confirmed on my flight to Honolulu on 1/16/08, as I was left cooling my heels for 45 minutes while various airline employees tried to clear me to fly.

How idiotic is the Watch List? If you have a common name like Charles Smith, very. It seems the way the List is compiled is this: somebody somewhere (who gets to add you to the List is shadowy/obscure, as is why you've been added) decides that a certain "Charles Smith" (for example) is somebody the TSA better keep an eye on.

So the TSA basically puts every "Charles Smith" in the nation on the Watch List (or every "Charles H. Smith"). Busy airport employees are then tasked with scanning hundreds of "Charles Smiths" to see if you're the bad guy or if you're cleared or if you're apparently not the bad guy.

How hard would it be to finger "Charles Hugh Smith" or "Charles Frederick Smith" born on such and such a day? Once you toss in a middle name and birth date, you eliminate about 99% of all "Charles Smiths" or even "Charles H. Smiths". How could any system which tags hundreds of people who happen to share a common name be considered efficient or useful?

From what I can gather, this Watch List must be cluttered with thousands of names of people who will be needlessly delayed at airports simply because they happen to have common names such as Sanchez or Brown or Chang.

If some security agency has fingered an individual as a potential threat to national security, can't they at least I.D. him correctly? Even if the guy is using aliases, then can't they get his various names and birth dates right? If you can't find out any more about a suspect than his name is "Charles Smith," then do you really have sufficient evidence to start tracking every "Charles Smith"? Or do you in fact just have shoddy law enforcement and intelligence work being passed off as "protecting the nation"?

Exactly how does such an idiotic system add even a speck of "security" to the nation's airports? This one example then suggests a further question: how many other of the security measures being overseen by the vast, sprawling Homeland Security bureaucracy are equally useless in terms of security? How many are needlessly annoying to the citizenry and stupendous wastes of tax money?

Being on the Watch List raises other questions, too. For instance: which "Charles Smith" is considered such a security risk that he must be screened before flying commercial aircraft? And what evidence fingers him as a security threat to the nation?

Has he frequented a church preaching hatred of the U.S.A.? Has C-4 explosive been traced to him? Has he flown to Islamabad and disappeared into the Pakistani hinterlands for long stretches?

In other words, has he exhibited any behavior which links him to known terrorist groups or threatening activities such as acquisition of illegal high explosives? Or is he just some poor schmuck who ran afoul of some bureaucrat somewhere, or some guy who a malevolent person secretly reported as "suspicious" to some acquaintance in a security or law enforcement agency?

I mean, how likely is it that some guy named "Charles Smith" is involved in terrorist activities? I have to admit a great curiosity about which "Charles Smith" has caused hundreds of the rest of us "Charles Smiths" to become suspects of interest, and what precisely has he done to warrant the interest of our nation's vast security agencies. Domestic terror leanings, perhaps? Hatred of the IRS? Who knows?

If standing around in front of the airline counter for 45 minutes while various employees work on clearing you to fly doesn't give you pause, well, try it some time and see how it feels. In the big picture, of course, it's a small delay, and no big deal; if it actually added to the security of the nation or the flight you're about to board, such a delay would be well worth it.

But it seemed instead like a totally useless expenditure of airline employees and passengers time, a system designed to waste time and create needless anxiety in completely innocent passengers.

If you're really a security risk, then you're on the "No Fly" List. Once you get on this List, you will not be issued a boarding pass under any circumstances, except perhaps with clearance from TSA in Washington.

So if the security forces tasked with protecting the citizenry already have a list for known "bad guys" considered serious risks (the No Fly List), then what the heck is the Watch List for except harassment and the churning of millions of records? Somebody's making money processing all these "Watch List" records, to be sure, but their activities don't seem to be adding to the nation's security. And it certainly doesn't take much of this nonsense to make you wonder if Homeland Security has any business maintaining such a flimsy, nonsensical Watch List in the first place.

Tuesday, January 15, 2008

How the U.S. Could End Up with High Interest Rates

January 16, 2008

I will be away on family matters from Jan. 16 - 24. I apologize for the lack of new posts in this period, and invite you to explore the voluminous archives on this site: forbidden stories, 2007 archives, Recommended Books/Films, and even the first chapters of a young-adult adventure novel, Claire's Great Adventure. I am sorry, but I will be unable to reply to email until I return.

Everywhere you turn, the pundits' predictions are unanimously for "much lower interest rates." Aren't you a little skeptical of any "received wisdom" on which the pundits all agree? I certainly am, as history has time and again thumbed its nose at collective certainty by swerving in the exact opposite direction of what was unanimously predicted as a "sure bet."

Low interest rates are supposed to calm the recessionary waters by invigorating the sagging housing market. Sure, lower rates make everything from corporate debt to new auto loans cheaper to service--but the real impact, we're told, will be on housing.

Why? Two reasons. First, the family house is the bedrock of 2/3 of the nation's families' wealth--and the key metric in their perception of overall family wealth (up, down, neutral).

Second, the last seven years of "prosperity" have been ones of equity expansion (rising stock market and home equity) and equity extraction (re-financing/equity lines of credit). If lower rates can re-ignite housing sales, the hope is that home prices will at least stabilize or perhaps even start rising again.

In an economy where 70% of GDP is consumer driven, does anyone actually believe that lowering the cost of corporate borrowing will pull the economy out of recession?

So lower mortgage and interest rates are seen as the essential foundation of continued consumer borrowing and the reinvigoration of the consumer's primary asset, their home. Nice, but what if rates don't stay low, but actually start rising?

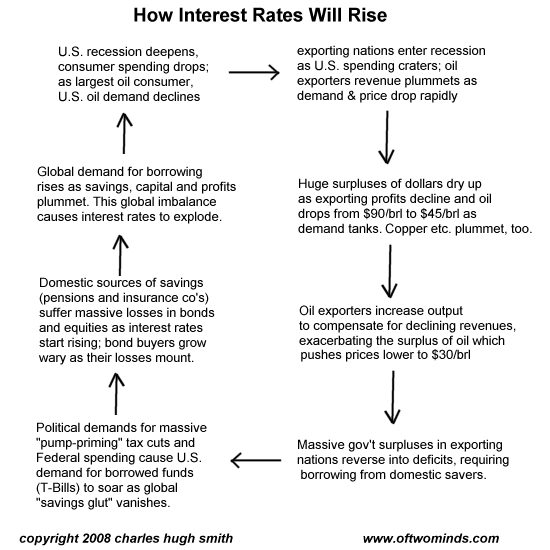

What situation could possibly cause U.S. interest rates to rise, regardless of the Federal Reserve's actions? Here's a graphic depiction of what could well cause real interest rates (that is, not the Fed Funds Rate, but what you and I will pay to borrow money) to rise in a long-term, self-reinforcing trend:

The key point is simple: the U.S. has been able to fund stupendous government deficits and a cheap/easy-money fueled housing bubble because non-U.S. banks and investors were piling up mountains of dollar-based exporting profits and petro-dollars which they needed to invest somewhere. Trillions of these profits flowed into U.S. bonds and debt-based securities (mortgage-backed securities, etc.), enabling cheap, easy-to-get loans and mortgages.

So what happens of a global recession knocks down both the profits made by exporting to the U.S., and the demand for oil? Then the pool of hundreds of billions in dollars looking for a home dries up in astonishingly short order.

As exporting nations slip into recession and deficit spending, they will tap the savings and capital of their own citizens. The way to do this is raise interest rates.

The pool of savings available to the profligate U.S. will dwindle, forcing the U.S. to bid for the shrinking pool of global savings. The only way to secure funding will be to raise the rates of return being paid to savers--i.e., interest rates will rise.

Two other forces will exacerbate this trend. As revenues drop along with the price of crude oil, oil exporters will pump even more product to compensate for lower revenues. This will depress prices further, pressuring exporters to pump more, and so on.

Secondly, as the global recession depresses corporate profits, global stock markets will tank, erasing trillions in capital. As interest rates rise, the value of existing bonds drops, too, setting up a one-two punch to pension funds, insurance company holdings, and individuals' retirement accounts. The global pool of capital will shrink, along with profits, reserves and savings.

All of this seems commonsensical, but we are told again and again that global savings are so robust that rates will stay low for years or even generations. What the pundits overlook is this: those savings are a result of an uprecedented global boom which is now ending. Once the boom dissipates, the profits and savings vanish along with it-- and so does all the cheap money which fueled the boom.

Readers Journal has been updated! Check out the new thoughtful, provocative ideas which have been added, including "401K debt cards," an excellent new essay by Lloyd L., What to Tell Your Children? and a new book recommendation by Riley T., Deer Hunting with Jesus: Dispatches from America's Class War

NOTE: contributions are humbly acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

A flurry of much-appreciated donations arrived in the past two weeks, and rather than delay recognition of those charitable souls who honored this site with their financial support, I am acknowledging one for every day I will be absent:

Thank you, Cheryl A. ($50), for your amazing donation in support of this humble site. I am greatly honored by your ongoing contributions and readership, and by your suggestions for topics.

Terrorism, Good Intentions and the Erosion of Civil Liberties

Several readers (Jon. H. and U. Doran) sent me this highly disturbing essay by Paul Craig Roberts, Thinking For Yourself Is Now A Crime on a new Federal "anti-terrorism" law which is poised to become law: Violent Radicalization and Homegrown Terrorism Prevention Act of 2007 (HR 1955).

Here is the core of the proposed law (full text available on the link above)

(1) COMMISSION- The term `Commission' means the National Commission on the Prevention of Violent Radicalization and Homegrown Terrorism established under section 899C.

(2) VIOLENT RADICALIZATION- The term `violent radicalization' means the process of adopting or promoting an extremist belief system for the purpose of facilitating ideologically based violence to advance political, religious, or social change.

(3) HOMEGROWN TERRORISM- The term `homegrown terrorism' means the use, planned use, or threatened use, of force or violence by a group or individual born, raised, or based and operating primarily within the United States or any possession of the United States to intimidate or coerce the United States government, the civilian population of the United States, or any segment thereof, in furtherance of political or social objectives.

(4) IDEOLOGICALLY BASED VIOLENCE- The term `ideologically based violence' means the use, planned use, or threatened use of force or violence by a group or individual to promote the group or individual's political, religious, or social beliefs.

`(1) FINAL REPORT- Not later than 18 months after the date on which the Commission first meets, the Commission shall submit to the President and Congress a final report of its findings and conclusions, legislative recommendations for immediate and long-term countermeasures to violent radicalization, homegrown terrorism, and ideologically based violence, and measures that can be taken to prevent violent radicalization, homegrown terrorism, and ideologically based violence from developing and spreading within the United States, and any final recommendations for any additional grant programs to support these purposes. The report may also be accompanied by a classified annex.

Here is what Mr. Roberts has to say about the proposal law, which already passed the House of Representatives 404 to 6:

"Harman's bill is called the Violent Radicalization and Homegrown Terrorism Prevention Act. When HR 1955 becomes law, it will create a commission tasked with identifying extremist people, groups, and ideas. The commission will hold hearings around the country, taking testimony and compiling a list of dangerous people and beliefs. The bill will, in short, create massive terrorism in the United States. But the perpetrators of terrorism will not be Muslim terrorists; they will be government agents and fellow citizens.

This search for extremist views comes after President Bush and the Justice (sic) Department declared that the President can ignore habeas corpus, ignore the Geneva Conventions, seize people without evidence, hold them indefinitely without presenting charges, torture them until they confess to some made up crime, and take over the government by declaring an emergency. Of course, none of these "patriotic" views are extremist."

Just to refresh our collective memories, here is the text of Amendments I, IV, VI and IX of the Bill of Rights, part of the U.S. Constitution:

Amendment I

Congress shall make no law respecting an establishment of religion, or prohibiting the free exercise thereof; or abridging the freedom of speech, or of the press; or the right of the people peaceably to assemble, and to petition the Government for a redress of grievances.

Amendment IV

The right of the people to be secure in their persons, houses, papers, and effects, against unreasonable searches and seizures, shall not be violated, and no Warrants shall issue, but upon probable cause, supported by Oath or affirmation, and particularly describing the place to be searched, and the persons or things to be seized.

Amendment VI

In all criminal prosecutions, the accused shall enjoy the right to a speedy and public trial, by an impartial jury of the State and district wherein the crime shall have been committed, which district shall have been previously ascertained by law, and to be informed of the nature and cause of the accusation; to be confronted with the witnesses against him; to have compulsory process for obtaining witnesses in his favor, and to have the Assistance of Counsel for his defence.

Amendment IX

The enumeration in the Constitution, of certain rights, shall not be construed to deny or disparage others retained by the people.

Let's start with Amendment IX. Allow me to paraphrase it: all rights not mentioned specifically by the Constitution do not default to the government, which can then restrict or grant such rights to the citizenry; all rights default to the citizenry except as defined by the Constitution.

Example: the right to have private conversations or electronic correspondence free from government eavesdropping. That right appears to have "defaulted" to the government, as domestic surveillance is now a de facto "right" of the government as it now needs to "root around and see what we can find that smells like domestic terrorism." Isn't this a clear violation of Amendment IV?

On the face of it, this commission sounds rather harmless, doesn't it? After all, all reasonable people agree that "the use, planned use, or threatened use, of force or violence by a group or individual" against the nation and/or its citizenry is a bad thing.

But wait a minute: what the heck is an "extremist belief system"? Here's how the proposed law reads:

The term `violent radicalization' means the process of adopting or promoting an extremist belief system for the purpose of facilitating ideologically based violence to advance political, religious, or social change.

Gee, doesn't this sound like a good description of Communism? And do we all recall how the "Red Scare" transmogrified into the House on UnAmerican Activities Committee?

Here is how the Committee "took care of" any "UnAmerican" activity it dredged up:

In 1947, the committee held nine days of hearings into alleged Communist propaganda and influence in the Hollywood motion picture industry. After conviction on contempt of Congress charges for refusal to answer some questions posed by committee members, the "Hollywood Ten" were blacklisted by the industry. Eventually, more than 300 artists— including directors, radio commentators, actors and particularly screenwriters— were boycotted by the studios. Some, like Charlie Chaplin, left the US to find work. Others wrote under pseudonyms or the names of colleagues. Only about ten percent succeeded in rebuilding careers within the entertainment industry.

In May 1960, the Committee held hearings in San Francisco that led to the infamous "riot" at City Hall when on May 13th, 1960, San Francisco Police fire-hosed students from Berkeley, Stanford and other local colleges down the steps beneath the rotunda.

The committee lost considerable prestige after it subpoenaed Jerry Rubin and Abbie Hoffman of the Yippies in 1967, and again in the aftermath of the 1968 Democratic National Convention. Unlike previous subjects of the committee's investigations, the Yippies neither respected nor feared the committee, and used media attention to make a mockery of the proceedings. Rubin came to one session dressed as an American Revolutionary War soldier, and passed out copies of the United States Declaration of Independence to people in attendance. Then Rubin "blew giant gum bubbles while his co-witnesses taunted the committee with Nazi salutes."

In the fifties, the most effective sanction was terror. (emphasis added CHS) Almost any publicity from HUAC meant the 'blacklist.' Without a chance to clear his name, a witness would suddenly find himself without friends and without a job. But it is not easy to see how in 1969 a HUAC blacklist could terrorize an SDS activist. Witnesses like Jerry Rubin have openly boasted of their contempt for American institutions. A subpoena from HUAC would be unlikely to scandalize Abbie Hoffman or his friends."

Hmm, does this ring any alarms about where a "harmless commission" can go all too quickly?

You may have noticed the photo of me in the upper left corner of this page dates from 1973. This is the time period when the F.B.I. was hounding me and arresting some of my colleagues for alleged violations of theSelective Service System , , a.k.a. the Draft, which was squeaked into law in 1940 by a one-vote margin in 1940.

Some believe the the Constitution does not grant the government the right to invoke involuntary servitude, i.e. the Draft. This "right to obligate all young males to serve their government in unpopular overseas wars" has been sanctioned many times by the Supreme Court, so it is now the accepted law of the land.

Back in this time frame, the F.B.I. devoted an extraordinarily large percentage of its resources and staffing to the "domestic terrorism" of the day, the anti-draft and anti-war movement. What this meant was the gutting of any anti-Mafia/Organized Crime efforts by the Bureau; the "big show" was nailing those draft resisters and activists.

Let me explain how this works. Some radicals burn down a ROTC building somewhere in the U.S. Gee, I'm against that kind of violence, but so what? You're against the Draft, and the war, then you are obviously on the same side as those guys who burned down the ROTC building, an act of domestic terrorist violence.

Here is a snippet of my own experience with the F.B.I. during its last rampage seeking "domestic terrorism" circa 1968-74. This is excerpted from my personal account of that era, Among the Best of Friends.

Please note I had complied with the Selective Service Act; I had not burned my Draft Card or engaged in any violent resistance. My "crime" was being a volunteer with that hotbed of "domestic terrorism," the Quaker-inspired, deeply non-violent American Friends Service Committee. (Please also note the Quakers are Christians. So much for thinking your religious affiliation and piety will protect you.)

"So the following day I received a call at home (I was 18, living at home) from the FBI. The agent was very aggressive, reminding me that aiding and abetting a draft resister was a crime with a 5-year prison term. My diffidence must have annoyed him—of course I was terrified, but why let him know it?—because he said, and I remember this verbatim: "This isn’t the Sunshine Biscuit Company, you know. This is the FBI." He was also kind enough to remind me that they "knew where I lived" and threatened to come up and interrogate me right then.

It should be noted that Draft boards held great power in their communities, and there were media-reported instances of drunk drivers who happened to be Draft Board members threatening Police officers with being drafted and sent to ‘Nam if they didn’t let them off with a warning."

So this is where "good intentions" to "root out domestic terrorism" lead you: an out-of-control police state with agencies running wild over the rights of the citizenry-- all done "legally" and with the the passive compliance of all the "good citizens."

Readers Journal has been updated Check out all the new opinions and reports. This is another banner week of thoughtful, provocative (and even some zany) ideas.

NOTE: contributions are humbly acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, eMeL H. ($50), for your very generous donation in support of this humble site. I am greatly honored by your contribution and readership. All contributors are listed below in acknowledgement of my gratitude.

Monday, January 14, 2008

Does It Really Matter What Currency You Own?

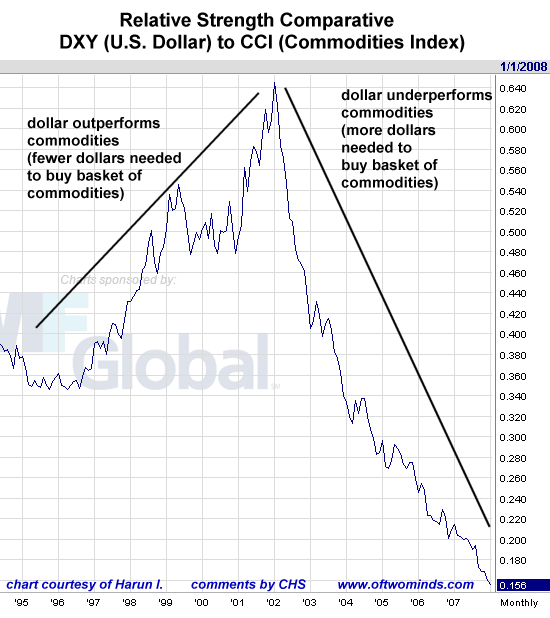

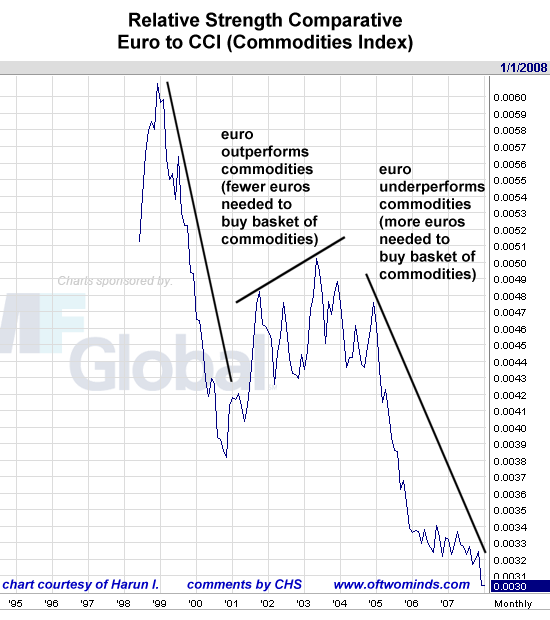

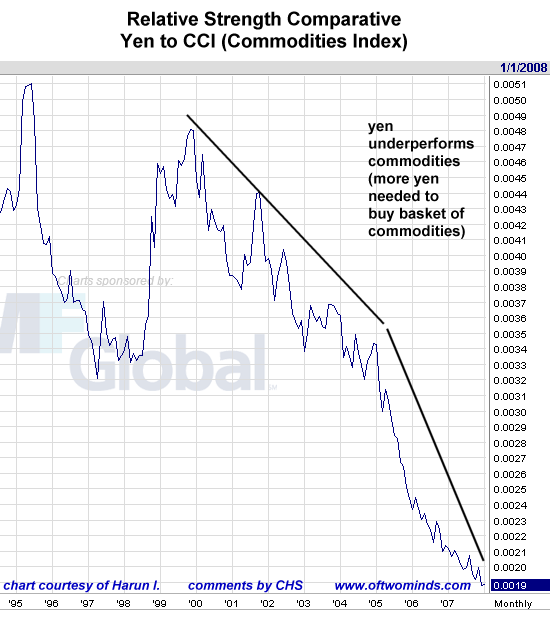

Is the trick to preserving purchasing power to put your money in a currency other than the dollar? Perhaps; but as frequent contributor Harun I. reveals, that's certainly not true of the globe's two other major currencies, the euro and the yen.

"The latest talk seems to revolve around which currency one should own. I have gone over this ad nauseam but to no avail. Against the basket of commodities (you know, the stuff we must consume to live) know as the Continuous Commodity Index (CCI) the major components of the USD index, the Yen and the Euro, are tanking in purchasing power at the same rate as the Dollar. What this means for the fiat currency system will only be know as a matter of history but the charts suggest it may not be good.

What the charts are basically saying is that, in real terms, as long as commodities are priced in dollars it does not matter which currency one owns.

I guess the one glimmer of hope is that under-performance leads to out-performance, but against a rising tide of unserviceable debt hope may remain just a glimmer."

Is there anything on the horizon which could change the trend? How about a global recession and some decent weather in grain-growing areas? As I have suggested here before, I foresee a recession of such depth, magnitude and speed that oil demand will fall so hard and fast that there will be a global surplus of oil, causing prices to plummet in half or perhaps even 2/3 back to $30/barrel.

Grain supplies have been stretched by rising demand and extremes of weather/low yields. Perhaps demand for meat won't drop much in the U.S., but as workers get laid off by the thousands in developing nations, those families will be eating less meat, cutting demand for grain. Toss in a bumper crop here and there, and wheat could fall from $10/bushel to $2/bushel in a relatively short period of time. If China slows its hyper-active building after the August 2008 Olympics, the demand for cement, steel and copper could drop enough to send prices spiraling downward.

As the price of gasoline plummets along with global demand for oil, ethenol won't be seen as such a panacea, and corn could suddenly be in surplus again, forcing prices down.

Just to widen the speculation to currencies, consider what would happen if any one currency were perceived to be "safer" than the others. What currency that might be--the yuan, the yen, the euro or the dollar--depends on just how roiled the global financial markets become, and which central bank is debasing their currency less than the rest. Severe social disruption could also quickly undermine the perception of a currency's value; indeed, the survival of the euro itself will become doubtful if the great central bank divide between Germany and Everyone Else widens.

Or perhaps commodities will slowly begin to be priced in ounces of gold. Once the Emperor (fiat money) has been revealed as naked, then perhaps some nation somewhere will demand a currency which isn't constantly losing purchasing power. That currency would rise, perhaps with amazing speed, as it becomes seen as a relatively secure store of value which is actually outperforming commodities and other currencies.

Could a "flight to safety" cause the dollar to reverse course and actually outperform falling commodities? Or could the yuan, euro or yen become a "flight to safety" currency? The cliche is that when the U.S. sneezes, the rest of the world catches cold. Perhaps the major currencies will soon reflect the relative fragility of each currency's home economy; if so, whatever economy suffers the least social turmoil and wealth destruction may be rewarded with a currency which actually outperforms sagging commodities.

Or maybe the "commodity-super-cycle" adherents are correct, and global demand will barely be dented by a massive, deep, long U.S. recession. Maybe gold will continue its climb to $3,000/ounce and the dollar will continue its depreciation to near worthlessness.

Maybe, but the premise that 75% of the global economy (non-U.S. economies) will be utterly unscathed by the sharp decline of the other 25% (the U.S. economy)--this makes little sense when you you look at the huge surpluses the rest of the world runs with the U.S.

If U.S. spending tanks, how can that not affect those who have profited from, and indeed, grown to depend on, exports to the U.S.? And if the exporting nations are actually more vulnerable than they seem, then who can say with any degree of certainty that commodites will continue to outperform all currencies? Could one currency suddenly outperform both the other currencies and commodities? As unlikely as it seems at the moment, we should be open to the possibility.

Readers Journal has been updated! Check out all the new opinions and reports. This is another banner week of thoughtful, provocative (and even some zany) ideas.

Here is but one entry, a fascinating bit of history contributed by Ron Sprouse:

"FYI regarding the air traffic controller strike. My father was an air traffic controller at Boeing Field in Seattle when he retired, just a short time before the strike. He was an air traffic controller in the Air Force in WWII helping the planes over the Hump in China.

I remember him sleeping for 8 hours after a shift and then returning to work for another 8 hours. There were not enough controllers hired for the work at hand. There was no radar, and he prefered it that way. All lights, and radio and Sea Tac control tower radar if they needed it.

They were interested in some sort of help, but a union was not an option then. The FAA wanted them to buy their own uniforms, but they refused and wore white shirts and ties instead. They were constantly asking for more help, but there was no relief. Wages were not very high.

The Seattle Times posted a cartoon of traffic control operators holding strings to numerous planes illustrated like balloons with the number of passengers written in the balloon. A hundred here a hundred there. (Westcoast was just trying out their 747 Jumbo jet, not in commercial use yet.)

Here's my point on the strike issue. Air traffic controllers were essentially still part of our armed forces under the FAA. What would happen if our armed forces personnel went on strike? They can't. Our defenses would be put at risk.

When the Cuban missile crisis occured, they gave the control tower a Red Phone to the White House. My dad also got a rad meter and a sign to put in the front windshield of his 1952 Nash Statesman that said "Air Traffic Controller must get to control tower". Reagan could not allow a strike because our national defense would be at risk. Therefore, they were replaced.

I believe this action sent an unintended message to some businesses that they could do the same, and therefore bust some of the smaller unions around the U.S. Hope this was of interest.

PS. I was a musician in Vegas Showrooms until our Union Local #369 was busted in the late 80's. "

Thank you, Harun, Ron and all the other contributors to Readers Journal for your thought-provoking commentaries.

NOTE: contributions are humbly acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Kevin L. ($25), for your much-appreciated donation in support of this humble site. I am greatly honored by your contribution and readership. All contributors are listed below in acknowledgement of my gratitude.

Saturday, January 12, 2008

Introducing Whine Magazine

Every time I read about the big bucks other sites are pulling in from advertising, I get jealous. Why am I so stupid? Who cares whether there's ads here or not? Why bother with dumb "ideals" when I could be pulling in thousands a month?

Then I drop all scruples, honor and my most closely held values and accept a big fat ad. So please welcome our big-bucks sponsor, "Whine" magazine.

NOTE: contributions are humbly acknowledged in the order received.

Thank you, Tanya Z. ($50), for your very generous and much-appreciated donation in support of this humble site. I am greatly honored by your contribution and readership. All contributors are listed below in acknowledgement of my gratitude.

Been thinking of contributing, but don't think your few bucks would matter? Hey, it's just you and me here; we don't have any big-bucks advertisers or sponsors. Believe me, it matters; you are it. Without your support, this thing's a tumbleweed blowing aimlessly along in the zephyrs of the Web.

Friday, January 11, 2008

What Are the Risks of Hyper-Inflation?

More than a few citizens are worried about the possibilty of a hyper-inflationary cycle taking hold in the U.S.--a cycles which would impoverish everyone.

New correspondent Scott M. describes the situation and reaches an important conclusion:

Thank you for your most recent submission on Inflation/Deflation and Purchasing Power.

I have been a loyal reader of your site for about the past year, and while always interested in your commentaries on the markets in particular, was moved to make a comment for the first time.

I too have been sucked into too many expert opinions on whether we will experience I nflation/Deflation or some other esoteric academic iteration or combination of the two. If one looks one can find the concept hotly debated on the web ad nausem (not to imply criticism of the web as at least we can enter into the debate, unlike with mainstream media). Alternatively one can read the commentary of experts (economists and the like) and be swayed back an forth by one side or another.

For a time I became captivated and obsessed with learning the answer to the question. Your submission has clarified and simplified the problem for me. However I cannot help thinking that there are still practical realities and impacts to me as an individual investor – depending on whether we experience hyper inflation generally, or a general decline in the cost of housing, consumable products, etc. brought about by an oversupply and a lack of demand (essentially because the spending mania has or will soon end).

First and foremost you are essentially correct. What matters to me, as an individual, is what my unique experience will be in the face of what is known and or can be reasonably projected (for example rising food prices, lower big screen TV prices, higher gas prices, and stable or falling house prices). It is clear to me (more clear after reading your blog) that their will be both gains and losses in purchasing power. It’s the net effect in your circumstance that matters most. For those that planned well there may be significant gains in purchasing power. I for example,

sold my house 18 months ago, rented a condo, invested one half of the equity in safe interest bearing vehicles and the other half in Gold and Oil/Gas investments. I am also a Canadian and we are fortunate that our currency has done well relative to the rest of the world – at least of late. So far so good. For perhaps many more individuals – who perhaps have not planned ahead, I fear that there will be a significant and continual loss of purchasing power.

Am I worried that my equity investments are susceptible to a potential deflationary spiral? Yes. The reason is that less purchasing power in the population generally, means less aggregate spending. Less spending means less demand for goods. Less demand means overcapacity. Overcapacity means lower prices. Eventually less demand for goods and services in general (and agreed not for everything like healthcare, gas, food, etc.), will mean lower corporate profits.

Lower corporate profits means lower stock market prices, fewer jobs, etc. One could then make the argument for a downward spiral ala Japan. If that is the consequence then my purchasing power has been negatively impacted if I do not prepare accordingly (e.g. increase the cash component).

One often reads that Bernake, as any good Central Banker would, fears “deflation”, and will flood the “system” with money thereby forestalling deflation but as a necessary consequence, will cause prices to increase (agreed the incorrect definition of inflation). Nobody has properly defined what “flooding the system with money” actually means. At least not to me. How does this money get into the hands of the debt satiated consumer who apparently is a key ingredient of the economy (to the tune of about 70% of GDP)?

Is it simply as easy as offering 1 % interest rates to the masses? Of course the deflationists take up the argument and say that you can lead a horse to water but you can’t make him drink (in other words lower rates and more and easy credit will not induce more spending) when (1) banks are not willing participants, (2) credit is “maxed out”, and (3) people suddenly “get” that it makes sense to save.

But what if the hyper-inflationists are right, and one last time the masses are granted this easy money and they in turn drive up the price of all goods. Not just gas, food and healthcare (that are clearly going there anyway) but stocks, Chinese made electronics, and perhaps even Real Estate once again? While I am confident that the value of my gold and gold stocks will appreciate at an even greater rate than general prices, I still have to prepare in a different way for this consequence, do I not? (e.g. decrease my cash component).

There are no easy answers, but at least you are bringing the debate down (from the lofty academic level) to the practical and individual level. I hope that you will continue the debate this topic in light of my questions and confusion - which I am sure is shared by many.

Perhaps it can be boiled down to one simple question. While the impact of whatever happens (inflation or deflation) is a function of each individual’s circumstances, is it not true that what happens to the general population (ie either a mass loss of purchasing power, or an illusionary increase in purchasing power through dollar devaluation) will in turn impact the individual investor and how they should plan?"

Excellent point. Scott. A cycle of hyper-inflation or deflation will certainly affect individual investors. I believe the following simple chart definitively answers the question of just how likely hyper-inflation might be.

The question this chart poses is this: would The Powers That Be who own the vast majority of the nation's wealth and influence its policies allow those policies to effectively destroy their wealth?

I think it is very safe to say the answer is "no."

Next, think about the banks. Let's say a bank has a $200,000 mortgage on a home and is making a nice safe return on that mortgage. Now let's say hyper-inflation explodes and the owner is "earning" $100,000 a month, soon to be $200,000/month. The owner peels off 10% of his pay and in a few months the mortgage is paid off. In terms of purchasing power, the bank received peanuts for what was once a substantial store of value.

If you're the banker, how can you make money in a hyper-inflationary cycle? Whatever money you loan today drops precipitously in value tomorrow, and so on, to near-zero.

The top 1% do own fixed assets, of course, just like the rest of us, and they are of course diversified around the globe. But their U.S. liquid assets would be rendered worthless by hyper-inflation. Why would they allow that cycle to take hold?

Finally, consider their position in a deflationary environment. Things are looking quite cheery for the super-wealthy in a deflationary cycle. All their liquid assets buy more real assets every month. Yes, perhaps there are another 30-40 million debt serfs struggling to make ends meet below them, but the poor have always been present and it hasn't really affected their wealth.

So which cycle serves the top 1%? The answer to that question is not hyper-inflation. Therefore policies will not enable, support or allow a hyper-inflationary cycle to take hold. It might be argued the policymakers are playing with a fire they don't understand; but my entire point is those who hold the nation's wealth do understand that fire, and they will never allow it to flare into a conflagration which destroys much of their wealth.

NOTE: contributions are humbly acknowledged in the order received.

Thank you, Renee S.-J. ($10), for your fifth donation in support of this humble site. I am greatly honored by your ongoing contribution and readership. All contributors are listed below in acknowledgement of my gratitude.

Reader M.G. sent me a link to a web-based cartoon site which declared a fund-raising goal of $20,000 for the year. A wealthy patron promptly sent in $20,000 in the first week. So wealthy patrons of this site (if any), how about doing the same for this site? Heck, $10,000 would meet my goals for the year. After all, I am not a talented cartoonist, just a poor dumb scribbler. So if $10K is a trivial amount to you, why not give a tip to the poor dumb writer?

Thursday, January 10, 2008

Stagflation: The Epic Battle Between Labor and Capital

Now that 25 years of high growth and benign inflation appears to be ending, the term stagflation--stagnant economic growth coupled with stubborn inflation--is once again in the news.

For a novel and perceptive interpretation of stagflation, we turn to frequent contributor Albert T.:

What is staflation really? High inflation and low growth is what we hear but why? The truth is stagflation is the battle between labor and capital for the share of the economic pie--wage share of income as we call it in one of my classes. (emphasis added--CHS)

This story is the trend in my view: Italians Dressed in Sunday Best Forced to Dine in Soup Kitchens

Dressed in his best Sunday suit, Fausto Cepponi took his wife and seven-year-old son out for dinner -- at a soup kitchen.

"I never thought I would be in this position,'' said Cepponi, 45, a security guard, dining in an 800-seat charity cafeteria near Rome's main train station. "I have a job, I had a car, but everything has become so expensive and what I earn just isn't enough. I panic every third week of the month.''

With salaries on hold, prices for staples such as pasta and bread rising and mortgages soaring, efforts to keep up appearances -- ``fare la bella figura'' in Italian -- can no longer disguise that thousands of job-holding Italians are failing to make ends meet. They've been labeled ``The New Poor,'' the title of a book published this year. "

The problem with inflation is that repricing of contracts (labor contract being one of them) is problematic unless you have leverage. Hence the writers strike and stagehands strikes (both have tremendous leverage).

Inflation is in essense a gambit of attacking your costs by raising prices, assuming your own costs will rise but fall short of the net benefit between the two increases. Unfortunately for capital in this battle my guess is the writers will win out in the end. However that doesn't mean that labor won't lose out to capital in other areas.

I personally think the coming bankruptcy of small cities and towns will make them merge and eliminate work force, ergo "civil servants" and those people will rejoin the world of the living.

You think large corporations got great tax breaks before for shifting new businesses to one state or another, just wait. We will see deals of the century; I am sure offers of 99 years without taxation perhaps even decades of subsidy and tax free bonds financing. Ergo capital for capital that is intensive will become very very low cost but labor will be driven into a state of frenzy so high that it will force politicians to compete to placate it's plight.

Imagine having a tough time buying food like the people in the story above and I am sure any wage where you can buy food will look good. That is what we call subsistance wage in one of my classes. Subsistance wage is where you cover your necessities but have no money at all for savings--just like the U.S. wage earner on average--many Americans now live paycheck to paycheck.

Although some of us are thriftier and do choose to save, that choice will soon be gone for the majority. The wonderful point about subsistance wage is that is where the capital return is highest for capital.

It might seem odd that everything is falling around us but if we think about it the world is making perfect sense. Assets are repricing because they are being sold off by those whom aren't capital holders. People who are laid off by the job cuts in banks etc will probably sell off any 401k they managed to bulk up to pay for the mortgage or daily expenses until they get a job. I would be very reluctant to go to a lower paying job until all my savings were gone too, or if I didn't live with my parents. Prices take a long time to adjust.

Italy truck strike ends -- for now

The short end of the story is basically truckers in Italy stoped all traffic for about 3 days + with food shortages and store shelves going empty along with gas pumps, etc... To get higher wages ofcourse because their income hasn't kept pace with inflation.

Germany: Train Drivers Strike Again

German train drivers brought local rail services across the country to a standstill to press their demand for higher wages. The railway has refused to meet the union’s demands for a wage increase of as much as 31 percent.

Train strike brings Germany to standstill

French rail authority says labor unions announce plan for 36-hour strike next week

(French and German unions have struck before and continued to strike until their wages were bumped up or some other economic benefit is provided to keep pace with inflation.)

Thank you, Albert, for a very insightful and deeply provocative interpretation. Now I get to add my three cents. (It used to be two cents but costs have risen.)

Albert makes some key macro points. The first is what he calls labor leverage. Albert's example is the current Hollywood writers strike. The writers have leverage because the production companies are bound by contract to hire union writers. Legally, they cannot just go hire new screenwriters from Bollywood for a hundred bucks a movie/TV show. There is also a fraternal system in Hollywood which does not lend itself to outsourcing of creative material.

In other words, the writers have leverage. Eventually the media companies run out of new content and their advertisers go away. Corporate income drops, the stockholders scream, the head honchos' heads roll, and new management cuts a deal to restore profitability. If labor has a stranglehold on corporate revenue/profits, they can actually win. That's leverage. If not, they lose.

(NOTE: I think you can guess where my sympathies lie in this dispute. Recording artists receive income for decades from their original material, yet writers are supposed to give up their electronic (future) rights for nothing? Gee, I wonder why the media corporations are fighting so desperately for 100% of future electronic profits.)

The opposite of leverage is wage arbitrage. This is the term for moving factories and call centers to places with lower labor costs. Thus the factory moves from the U.S. to China, from Dusseldorf to Bulgaria, from Italy to Sri Lanka, and so on--in an endless chain which eventually leads--and has already led in some cases--to factories in "high cost" China being moved to "low cost" Vietnam.

How many jobs in the U.S. are vulnerable to wage arbitrage? A lot. Manufacturing jobs in the U.S. total about 14 million now, while China has about 110 million factory jobs. In one sense, this makes China far more vulnerable to wage arbitrage than the U.S. All the U.S. manufacturing jobs which could be shifted to cut costs have already been moved; those 14 million manufacturing jobs still here are here for a reason.

Like what? Like the materials are too heavy and the labor costs too small a percentage of the final cost to make offshoring the plant worthwhile. Examples include glass (heavy and brittle, often requires high-tech coatings better done here by robots), lumber products and various pharmaceuticals. (Pirating in China has destroyed many brands and pharmaceutical products' markets, so why bother even making stuff there?)

Meanwhile, we have friends whose family business manufactures specialty steel products. They have already moved their factory from China to Vietnam, and they are not alone. There are plenty of stories about wages rising in China to the point that wage abritrage is now a factor in China's growth as well.

Albert makes repeated mention of labor union strikes in Europe--especially those in transport. Municipal labor unions have plenty of leverage over public transport and services, as we all know. Subway/train and garbage strikes are usually quickly resolved in the unions' favor.

But as Albert points out, what happens on a macro level when cities and public agencies go bankrupt? As readers know, I have been forecasting just such a tidal wave of public bankruptcies for several years.

The problem for public unions is they don't control or even influence the revenue side of public agencies' ledgers. The basic model for the past 25 years of union contracts has been this: when unions strike, the easiest way to lower the pain (public outcry at the disruptions, etc.) for agency managers has been to cave in and agree to higher wages/benefits. Then the agency raises ticket prices or taxes. The public has grumbled but never revolted.

That will change once people find they can't afford food by the third week of the month. Their sympathy for well-paid transit and public union workers will vanish, and they may, for the first time, refuse to pay the higher ticket prices or higher property taxes.

If politicians start losing elections for trying to raise taxes, then agency heads will also roll. Bottom line: it's the politicians who control the revenue stream, and the public has the ultimate leverage on them.

If we wander back down memory lane, we can recall that President Reagan was faced by what appeared to be a union with tremendous leverage: the air traffic controllers. Now the air traffic control system is in dire need of a complete (and costly) overhaul, and I am not knowledgeable enough to say whether the union being busted was a good thing for the nation or not.

My point is simply this: public officials can stand up to public unions when pushed beyond a certain point--and when the public supports the officials. Europe and the U.S. have a different mix of public and private labor. About 40% of the French workforce is public or semi-public employees. That's a high enough percentage that they can practically control elections and vote in tax increases as a policy of self-interest.

But at some point, the private corporations and businesses who are paying the high taxes may rebel, and either close down (in the case of cafes and small businesses) or leave for more hospitable climes--wage and tax arbitrage, another issue Albert raised so preciently.

If public revenue (taxes) cannot keep pace with public union demands, then something will have to give. I would anticipate a situation in which transit/rail workers go on strike, demanding higher wages. This is a strategy which has worked exceedingly well for 60 years (since 1945). But alas, they will be told by bankrupt public authorities there simply is no more money. The unions will have a difficult time grasping this strangulation of the public revenue stream. But can't you raise taxes on someone, somewhere? No; all the productive businesses have left, exploiting global wage and tax arbitrage.

Many observers in California have noted the flow of jobs from California to other states--that is, wage and tax arbitrage within the U.S. Businesses and jobs leave California for lower-cost states. At an even finer-grained level, businesses leave high-cost San Francisco for lower cost suburbs. Like water flowing to the lowest level, businesses flow to the areas with the lowest wages and taxes. In many cases, they really have no choice; their competitors are already reaping the benefits of lower wages and taxes, and they can cut prices and increase profits as a result.

So the question for each of us becomes: how much leverage do we really have?

Readers Journal has been updated! An important new essay and many excellent comments on Can a Fragmented Culture Find Common Ground? and inflation/deflation.

Readers commentaries

Thoughts on a Common Culture (Chuck D.)

NOTE: contributions are humbly acknowledged in the order received.

Thank you, Jennifer K. ($10), for your most-welcome support of this humble site. I am greatly honored by your contribution and readership. All contributors are listed below in acknowledgement of my gratitude.

Wednesday, January 09, 2008

Inflation/Deflation and Purchasing Power

A great debate rages about whether the future holds runaway inflation, Japan-style deflation, or stagflation. Every time I write about the notion of inflation and deflation co-existing, e.g. biflation, or stagflation, I am informed that inflation and deflation reflect only money supply, not price or supply and demand.

My problem with setting money supply as the defining measure of inflation and deflation is practical. This pronouncement leads to an obsession with measuring money supply rather than with the relative loss or gain of purchasing power.

Purchasing power, which reflects plain old supply and demand and the relative store of value of a currency or other money, matters more in the "lived" economy than money supply. In this view, both inflation and deflation are misleading concepts and should be set aside as such.