When Housing Is Priced in Gold

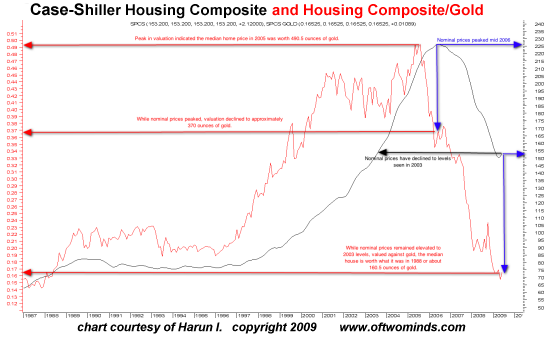

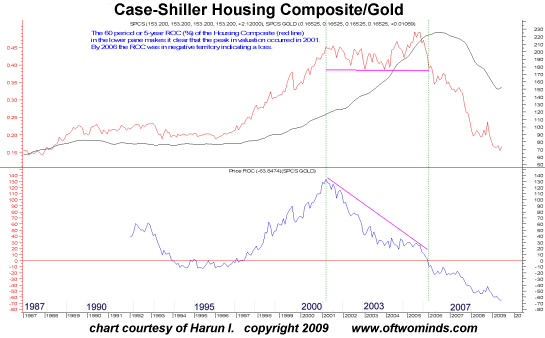

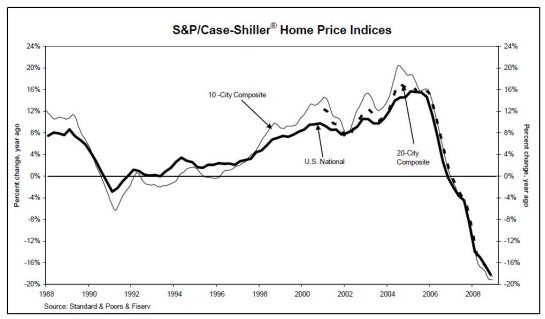

Pricing U.S. homes in gold reveals that housing has fallen by two-thirds from its 2005 peak. Frequent contributor Harun I. suggested an interesting relative-value experiment: how has housing performed in the past 20 years when priced in gold? Oftwominds.com readers know that relative performance/purchasing power has long been a theme of Harun's and of this site. Considering all metrics of value in terms of purchasing power reveals much more insightful measures of value than nominal prices. For instance, measuring the cost of housing in terms of "how many loaves of bread would be needed to buy a house?" is a more accurate measure of purchasing power and valuation than measuring housing in terms of dollars, which have lost 25% of their value to inflation in the past decade and much more when compared to other currencies. Since gold is a universal metric of money, let's see how housing has done when priced in gold. Yes, I understand you can't live in gold or plant trees in gold, but the exercise isn't to suggest housing is "only" an investment like gold--the point is to seek an understanding of the relative peaks and valleys in housing valuation. In other words, is housing "cheap" now? There are various accepted metrics of approaching this question, for instance, comparing the equivalent costs of renting versus buying. Another is to ask if buying a house and renting it out at current market rates would yield a profit, and if so, how does that profit compare to other alternative investments? Priced in gold, housing has already fallen 2/3 from its 2005 peak when priced in gold. Harun's charts are large-format, so I have posted thumbnail versions below. Just click on the thumbnail to open the full-sized chart in a new browser window. The charts plot the well-known Case-Shiller Housing Composite as the proxy for the U.S. housing market. Harun offered these comments on the charts and the housing/gold ratio (relative-strength). Click on chart for a full-sized version in a new browser window. At the peak in 2005, the median home price equaled 490 ounces of gold. The present median price is worth about 160 ounces of gold, or roughly the same valuation as 1988. Nominal housing prices have returned to 2003 levels. But when priced in gold, the 2003 valuation was 420 ounces of gold. Now that nominal prices have returned to that level today, the median house will only fetch 160 ounces of gold. But if nominal prices revert to pre-bubble valuations (1997-98), which is the typical course of popped asset bubbles, then we could see housing become even cheaper when priced in gold. That is, if gold continues rising and housing continues declining, then it is certainly possible that the median house price could fall to 100 ounces of gold--a mere 20% of its 2005 peak. Harun's second chart plots the housing/gold ratio's rate-of-change. Click on chart for a full-sized version in a new browser window. Here are Harun's comments: Stated another way the best time to sell your home and buy gold actually occurred in 2001; you would have received twice the gold which would have seen very handsome appreciation. The truth: the boom was over by the time everyone thought it had begun. Priced in gold, the median house bought 460 ounces of gold in 2001 and 490 ounces at the peak in 2005--a gain of 6%, considerably less than the nominal price in dollars. Had a homeowner eschewed the blandishments of the housing bubble in 2001 and sold his/her home for 460 ounces of gold and rented for eight years, he/she could now buy a home for 160 ounces of gold and have 300 ounces in hand. Here is a chart of the Case-Schiller Composite plotted in percentage points of rise or decline. If we looked only at this chart, we might reach the conclusion that housing has "bottomed" and that it's "cheap." But if we price housing in loaves of bread or gold, we might reach a completely different conclusion: priced in commodities or gold, housing may not have reached its nadir, and other stores of value might retain more purchasing power than housing. Should gold plummet, then of course housing would rise in relative performance even if it remained flatlined in nominal prices. If gold were about to fall dramatically, then this could be the relative valley in housing/gold valuations. But the more likely scenario remains a continuing decline in nominal housing prices back to pre-bubble valuations. In this case, even if gold remains flatlined at $1,000 an ounce, then it will take fewer ounces of gold to buy a house in the future. The point is to consider housing in relation to purchasing power/relative performance, not just in nominal dollar terms. Housing will always have value as shelter and land will always have value as productive dirt, but we must be skeptical of the constant hype that "a home is your best investment." For the past eight years, when priced in gold, that has been patently false. "Your book is truly a revolutionary act." Kenneth R. Thank you, Willard S. ($50), for your stupendously generous donation to this site. I am greatly honored by your support and readership.The first chart is the S&P Case-Shiller House Price Composite (black line). The red line is an RS (relative-strength) of the composite to gold. Historical comparison suggests home prices are still overvalued. The red line indicates that homes are worth in gold what they were in the late 1980's while nominal prices remain elevated.

In 2001 the median house fetched 460 ounces of gold and the median price was about $115,000, a 4-to-1 ratio ounces of gold per dollar of house value. By the valuation peak in 2005 that ratio had fallen to 2.17-to-1. The boom period actually saw an overall loss in value.

Permanent link: When Housing Is Priced in Gold

If you want more troubling/revolutionary/annoying analysis, please read Free eBook now available: HTML version: Survival+: Structuring Prosperity for Yourself and the Nation (PDF version (111 pages): Survival+)

Of Two Minds is now available via Kindle: Of Two Minds blog-Kindle