The Keynesian Project Is Psychotic

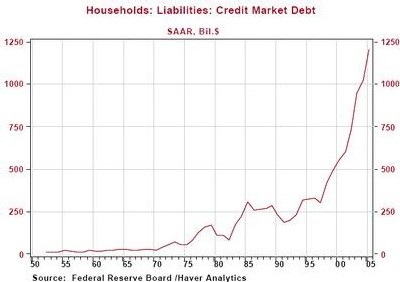

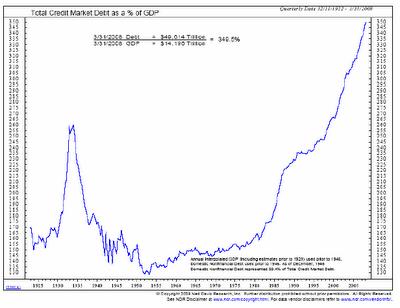

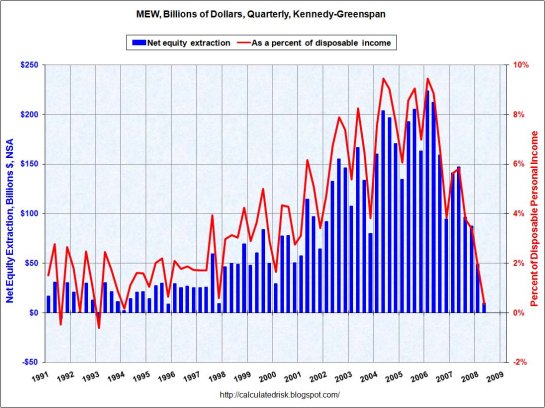

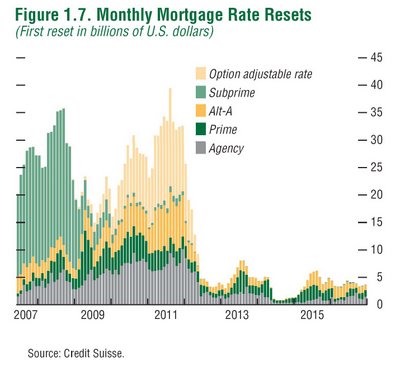

This Week's Theme: "I've got a bad feeling about this..." The Keynesians, though well-meaning, suffer from a psychotic disconnect between their "project" of reinflating private borrowing and consumption and financial reality. I've got a bad feeling about the Keynesian "project" of reinflating private borrowing and consumption by borrowing and squandering trillions of dollars of public funds and by maintaining "quantitative easing" and the Fed's zero interest rate policy (ZIRP). While it's clear the Keynesians are well-meaning--they truly want to minimize suffering and to "restart" private borrowing and consumption--their grasp of reality is so tenuous that it qualifies as psychotic. Let's review the assumptions, implicit and explicit, of the Keynesian project. 1. The Keynesian project is founded on the belief that consumers want to borrow and consume more, and the only impediment to their wishes is the cost of borrowing money and the availability of money. Psychotic disconnects from reality: A. most middle-income Americans have little need for more stuff or more services (they already have too much junk in their lives as it is); they want savings and cash, not more "consumer" crap from overseas or a second house, fourth vehicle, etc. B. Americans either cannot borrow more due to the plummeting value of their assets and income or their present debt levels are so astronomical that only an insane institution with no regard to risk (the Fed?) would even dream of loaning them more money even at zero interest. C. Middle-aged Americans who could perhaps borrow a little more have no interest in doing so as they can see a demographic cliff ahead: they need cash and savings for the future, not more "consumer" crap from overseas or a second house, fourth vehicle, etc. D. Some 40% of the populace does not even pay Federal income tax; they are unlikely to have the spare ("discretionary") income to support borrowing, even at low interest rates. E. The "bottom 90%" of the populace own a mere 7% of the financial liquid assets of the nation; the top 10% own 93% and the top 1% own some 60%. (Source: Who Rules America? (G. William Domhoff). And where is the personal income to support new borrowing and debt servicing? This means that the vast majority of Americans have few assets except their home--and since the housing/credit bubble popped, tens of millions of homeowners (about 64% of the households own dwellings) have zero or negative equity in their homes. In sum: Only a psychotic person could believe most Americans are qualified to borrow more money or are interested in borrowing/spending more money. There is literally no evidence to support the Keynesian orthodoxy and abundant evidence that reality is light years away from their blithe assumptions. Americans pulled the equity from their homes long ago: F. Americans whose chief asset is their home are about to become even poorer as mortgage resets, "shadow inventory" and foreclosures boost supply as demand falters, pushing housing prices lower into 2011 and 2012. There are almost 19 million vacant dwellings in the U.S.--a massive oversupply that is almost beyond comprehension. G. Incomes of the working poor and lower middle class are being squeezed to insolvency by rising sales taxes, vehicle taxes, junk fees, parking tickets, speeding tickets, unaffordable healthcare (get sick, go bankrupt) and outrageous higher-education costs. Only someone completely detached from reality enjoying a plump Ivory Tower professorship or plum post in D.C. could believe the average American has the assets, creditworthiness, income or desire to borrow more and then blow that borrowed money on needless consumption. 2. The Keynesian project believes that zero interest rate policy (ZIRP) and QE (quantitative easing) are necessary and benign ways to boost bank lending and consumer borrowing. Psychotic disconnects from reality: A. Kansas City Federal Reserve Bank President Thomas Hoenig has said that an extended period of ultra-low interest rates invites speculative behavior. Everyone knows the Greenspan era's super-low rates and easing of lending standards ("easy money") created history's biggest credit/housing bubble, and yet the Keynesian project wants to maintain the same disastrous policy for as long as it takes to reinflate assets and spark renewed consumer borrowing. As my esteemed colleague Karl Denninger has explained very cogently in the problem with ZIRP, zero interest incentivizes speculation as owners of capital are forced to desperately seek some return, any return, which means taking on risk and increasing the instability of the entire system. ZIRP also creates a pernicious disincentive to saving and capital formation: and capital (not debt) is the very foundation of capitalism. Destroy the incentives to create capital via savings and you destroy capitalism. In its stead we now have a State-managed system based on exponential expansion of credit. B. As Karl also explained, interest on mortgages, credit cards, auto loans, student loans, etc. etc. remove funds from the consumers' income, making them poorer. With consumer debt at unprecedented levels, then a huge percentage of household income already goes to debt service. If you scrape off the top 10% of households (those earning $135K and up), then the percentage of income spent on debt service really climbs. What households need is less debt, not more. Only a psychotic believes Americans can afford more debt, that they need more houses (how about the 19 million we already have which are empty?), that inflation is benign (local government junk fees, tuition, medical costs, garbage collection, sales taxes, vehicle registration fees, etc., are rising at double-digit rates) and that the "solution" to the Great Recession is a massively pernicious and destructive ZIRP/QE policy. C. In case nobody noticed, banks are sitting on trillions of dollars in uncollectable/ impaired debt, and loaning them Fed money at zero interest does not improve their fundamental insolvency: Banks Out of the Woods? Maybe Not. In keeping with the Survival+ analysis, we need to ask cui bono of the Keynesian project: who benefits from QE/ZIRP, credit/asset bubbles and rising household debt? The Keynesians--well-meaning psychotics that they are--would like us to believe it is "the average American household." Here is the real answer: DailyJava.net is now open for aggregating our collective intelligence. Of Two Minds is now available via Kindle: Of Two Minds blog-Kindle

This week's theme will be familiar to anyone who has seen the original Star Wars films in which Luke, Leia or Hans Solo utter the ominous words "I've got a bad feeling about this..." just before a crisis strikes.

NOTE: Due to work overload and obligations in the real world, my time online will be severely limited this month. My apologies for being unable to respond to all email and thank you for your readership.

If you haven't visited the forum, here's a place to start. Click on the link below and then select "new posts." You'll get to see what other oftwominds.com readers and contributors are discussing/sharing.

Order Survival+: Structuring Prosperity for Yourself and the Nation and/or Survival+ The Primer from your local bookseller or from amazon.com or in ebook and Kindle formats.A 20% discount is available from the publisher.

Thank you, Sreenivasulu S. ($25), for your exceedingly generous donation to this site. I am greatly honored by your support and readership. Thank you, Eugenio M. ($20), for your exceptionally generous donation--one of so many you have bestowed on the site. I am greatly honored by your support and readership.