Financialization = Inequality

Financialization is the disease eating away the heart of the economy and what's left of democracy.

There are a number of factors behind the widening canyon of economic inequality, but the primary driver is financialization. Financialization has given those with capital and access to financier expertise ways to skim great wealth from the system without creating any value whatsoever.

Those with a home that is owned free and clear and $500,000+ in a 401K or retirement account have more capital than the vast majority of Americans, but members of the upper-middle class have no access to the leverage and tools of financialization.

In other words, financialization isn't a consequence of having capital: it's the consequence of having access to unlimited credit, leverage and low-risk, low-tax skimming operations (for example, tax codes enable hedge funds to declare income as low-tax long-term capital gains).

From the financier point of view, the upper-middle class tax donkeys who keep all their investment capital in mutual funds are the marks who supply liquidity to the system. The wealthy who park money in hedge funds are marks of a higher order, as their cash enables fund managers to gamble with other people's money and then return a thin slice of the gains (if any, after fees) back to the investors.

A carry trade is a classic skimming operation. The term is based on the difference between the costs of holding (carrying) one position and the gains earned by investing the proceeds elsewhere.

A typical example has been borrowing money for near-zero interest in Japan (yen) and using the proceeds to buy higher yielding Treasury bonds in the U.S. Here is Dan Norcini's description:

To define this term, "carry trade", for those who are a bit newer to the markets, it consists of borrowing large amounts of Yen for extremely low costs due to the miniscule short term interest rate in that nation, and taking those proceeds, exchanging it into different currencies and then using that money to make investments elsewhere where higher yields may be obtained. If that is not risky enough, most of these hedge funds then leverage their speculative bets in the hopes of compounding their gains.

There is a risk to currency carry trades: if the currency you borrow appreciates, then the trade blows up as the exchange rate loss exceeds your interest rate gain. The yen carry trade expanded to an estimated $1 trillion because the dollar/yen exchange rates were relatively stable.

The sweetest carry trades occur when two currencies are officially pegged but there is a big difference in interest rates between the two currencies. The lack of volatility in the exchange rate lowers the risk of this trade to near-zero--until the peg blows up.

You Don’t Really Understand the Carry Trade, Do You? (Yahoo Finance)

Would you like to leverage a carry trade 10 to 1? Hmm, who will loan you $1,000,000 based on $100,000 collateral? That's a key feature of financialization: the real power--leverage and access to global markets--is not available to you. The skimming operations are only open to the financier class.

Leveraging phantom collateral is another feature of financialization. Commoners were allowed a taste of this when subprime lenders were offering no-document, no-down payment mortgages back in 2004-2007. Phantom income was posted as collateral for the nothing-but-leverage loan.

The same sort of trade appears to be occurring in China, where a warehouse of copper is pledged as collateral for a legitimate bank loan at a rate of 4.5%. The proceeds are then loaned out at 10% (or higher) in the shadow banking sector of informal, unregulated credit.

What's to keep several people from pledging the same warehouse of copper? Nothing.

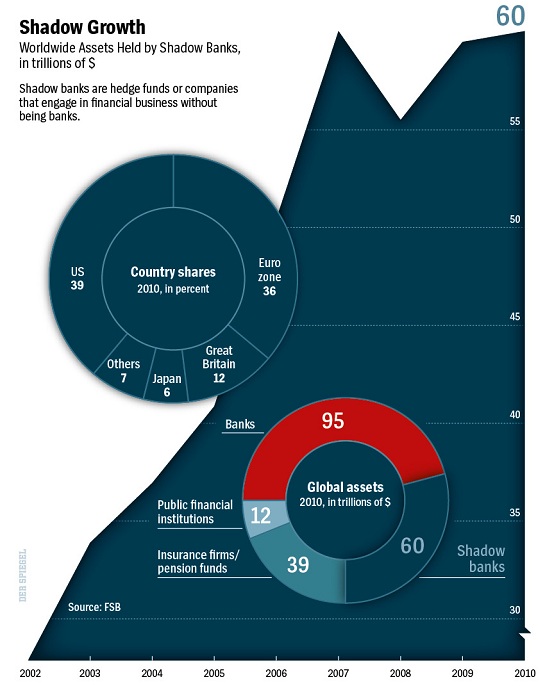

The carry trade blows up when the shadow-banking borrower defaults. Globally, the shadow banking system has ballooned to almost unimaginable proportions as financiers have sought out skimming operations:

Leverage and high-finance skim operations do not require much capital. It takes essentially no capital to originate a derivative; just craft the thing to protect your interests and sell it to some money manager as a valuable hedge.

If you have the right position and tools, it doesn't even require collateral to access gargantuan trading lines of credit.

The point is financialization is about leverage and skimming the existing system for immense profits. It's not about hedging legitimate industries' risks or investing in productive enterprises; it's all about skimming wealth while providing no value to the real economy or society.

The hidden toxin in financialization is the resulting concentration of wealth can buy concentrations of political power. Financialization is thus self-perpetuating: once the skimming operations generate billions of dollars in profit, it only takes a relatively small piece of these profits to buy/influence the political class. Once the politicos are in your pocket, the regulators and judiciary fall into line or are marginalized by new statutes or gutted budgets.

When Congress dared to question hedge funds' primary tax break (declaring income as long-term capital gains), the industry went apoplectic and declared capitalism, Mom and apple pie were all at grave risk if their skimming operations were taxed at the same rate you and I pay on our income.

Financialization is the disease eating away the heart of the economy and what's left of democracy.

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify or understand. We will cover the five core reasons why things are falling apart:

1. Debt and financialization

1. Debt and financialization2. Crony capitalism and the elimination of accountability

3. Diminishing returns

4. Centralization

5. Technological, financial and demographic changes in our economy

Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Not accepting responsibility and being powerless are two sides of the same coin: once we accept responsibility, we become powerful.

Kindle edition: $9.95 print edition: $24 on Amazon.com

To receive a 20% discount on the print edition: $19.20 (retail $24), follow the link, open a Createspace account and enter discount code SJRGPLAB. (This is the only way I can offer a discount.)

| Thank you, Peter G. ($20), for your extremely generous contribution to this site -- I am greatly honored by your support and readership. | Thank you, James A. ($10/month), for your outrageously generous subscription to this site -- I am greatly honored by your support and readership. |