Why We Cannot Print/Borrow/Spend Our Way to Prosperity

Ballooning government deficit spending and debt has a negative effect on private GDP, money supply, money velocity and wages.

I have often explained why the Keynesian belief that the government can print/ borrow and spend enough money to trigger self-sustaining prosperity is a nonsensical, magical-thinking Cargo Cult.

The Federal Reserve's Cargo Cult Magic: Housing Will Lift the Economy (Again) (September 11, 2012)

The Dangerous Blindspots of Clueless Keynesians (January 2, 2013)

Misunderstanding Austerity, Stimulus and Demand (January 17, 2013)

The following charts show why printing/borrowing and spending our way to self-sustaining prosperity has failed, and why it will continue to fail, with eventually catastrophic results: the returns on this unprecedented borrow-spend policy are diminishing to near-zero or negative.

Humanity has an innate attraction to conspiracy and complexity. Humans have been selected to seek patterns in Nature and in the behavior of the humans around them. No wonder humans are drawn to detective stories, puzzles and conspiracies.

While conspiracies are indeed a part of the human experience, focusing on human intent and collusion can distract us from the impersonal systems that dominate economic history.

In a similar fashion, an obsession with complexity distracts us from what is blindingly obvious. Just as the alcoholic refuses to admit his addiction lest he be forced to tackle his self-destruction, so too do we avoid the financially obvious lest we be forced to surrender our ardent hope that the increasingly fragile Status Quo we depend on is enduring and secure.

As long as the interest rate on debt is low, the path of least resistance is to keep borrowing to support politically untouchable fiefdoms, cartels and constituencies. Eventually, the cost of servicing the debt overwhelms the diminishing returns on the debt-based spending.

Let's start by admitting the unprecedented rise of government debt in the past decade.Here is the Federal debt, not including the bogus inter-governmental debts (mostly money owed to the illusory Social Security Trust Fund).

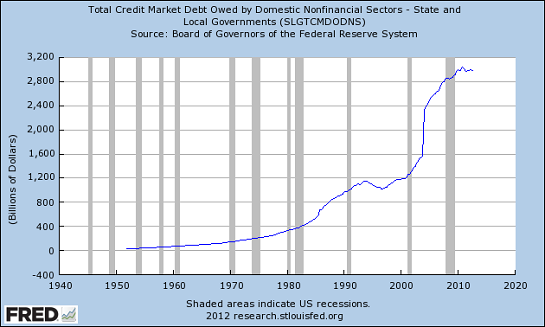

Everyone knows Federal debt has skyrocketed, but so has the debt of state and local governments: state and local government debt has risen by 250% just since 2002.

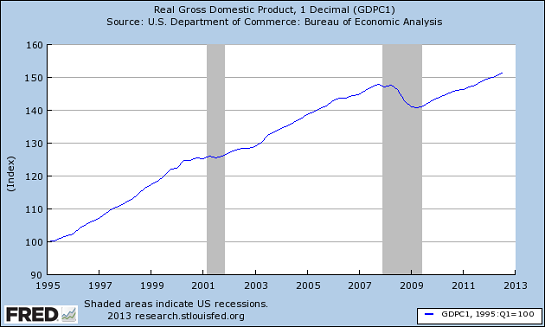

GDP includes government spending; this vast expansion of debt-based spending has had a very modest positive impact on GDP:

Courtesy of longtime correspondent B.C., here are five insightful charts. The first displays the ratio of GDP minus government spending to total Federal debt. This reveals the effect of massive Federal borrowing on the private sector--the non-government part of the economy.

When the line is rising, private GDP is expanding even as Federal debt increases. Thus the private economy expanded smartly from 1959 to 1973 while the Federal government ran relatively modest deficits. If we look at the first chart above, total Federal debt, we see that it was basically flatlined in this period--the deficits of this period barely moved the needle on total Federal debt.

As Federal deficits and debt increased in the 1980s, private GDP was negatively impacted. Only the twin speculative bubbles of the late 1990s to mid-2000s (dot-com and housing) reversed the trend. Once the housing bubble popped, the effect of rapidly rising Federal debt has had a very negative correlation to private GDP.

It's even worse when state and local government debt is added:

What is the correlation of rapidly rising Federal debt and money supply? It appears ballooning Federal spending/debt no longer boosts money supply much:

As B.C. observes: The purchasing power of wages is in freefall vs. the growth of debt-money. Increasing Federal debt and spending is not boosting wages.

The effect of rising government debt on wages has been declining for 40 years, a trend interrupted only by brief speculative bubbles.

Meanwhile, massive Federal borrowing and deficit spending has opened a structural deficit of monumental proportions: anyone claiming this is sustainable or healthy is either in a drunken daze or mesmerized by Cargo Cult magical thinking.

As government borrowing and spending skyrocketed since 2002, household income flatlined during the housing bubble and then fell off a cliff as the State-enforced financialization of the economy hollowed out household wealth and income. In a Central State/cartel capitalism system like America's, the cost basis for both enterprises and households constantly rises, pressuring wages lower for the majority of wage earners. We see this clearly on this chart:

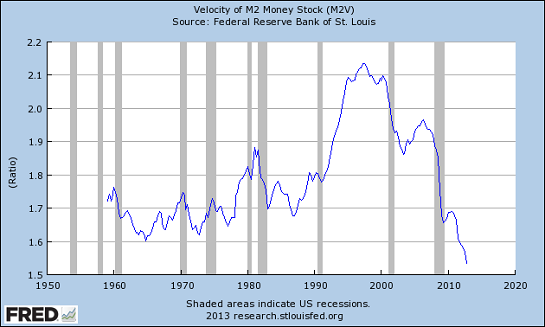

What effect has this unprecedented expansion of government deficit spending and debt had on the all-important velocity of money? Catastrophically negative: Money Velocity Free-Fall and Federal Deficit Spending (January 18, 2013)

Ballooning government deficit spending and debt have a negative effect on private GDP, money supply, money velocity and wages. Printing money does not make us wealthier, nor does borrowing and squandering money on consumption and malinvestment make us wealthier.

That which we sow now we shall reap later.

NEW VIDEO: A DELUSIONAL & DYSFUNCTIONAL STATE (29 minutes, 25 slides)

NEW VIDEO: A DELUSIONAL & DYSFUNCTIONAL STATE (29 minutes, 25 slides)

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify or understand. We will cover the five core reasons why things are falling apart:

1. Debt and financialization

1. Debt and financialization2. Crony capitalism and the elimination of accountability

3. Diminishing returns

4. Centralization

5. Technological, financial and demographic changes in our economy

Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Not accepting responsibility and being powerless are two sides of the same coin: once we accept responsibility, we become powerful.

Kindle edition: $9.95 print edition: $24 on Amazon.com

To receive a 20% discount on the print edition: $19.20 (retail $24), follow the link, open a Createspace account and enter discount code SJRGPLAB. (This is the only way I can offer a discount.)

| Thank you, Clifford S. ($25), for your most generous contribution to this site -- I am greatly honored by your support and readership. | Thank you, Jonathan F. ($100), for your outrageously generous contribution to this site --I am greatly honored by your support and readership. |

Read more...