The First Domino to Fall: Retail-CRE (Commercial Real Estate)

The domino of retail CRE will not fall in isolation; it will topple the domino of debt next to it.

That the retail trade is stagnating has been well-established: for example, The Retail Death Rattle (The Burning Platform).

Equally well-established is the vulnerability of the bricks-n-mortar commercial real estate sector to this downturn: yesterday's analysis by Mark G. makes the case:After Seven Lean Years, Part 2: US Commercial Real Estate: The Present Position and Future Prospects.

I'd like to extend Mark's excellent analysis a bit because it suggests that the retail CRE (commercial real estate) sector will likely be the first domino to fall in the next financial crisis--the one we all know is brewing.

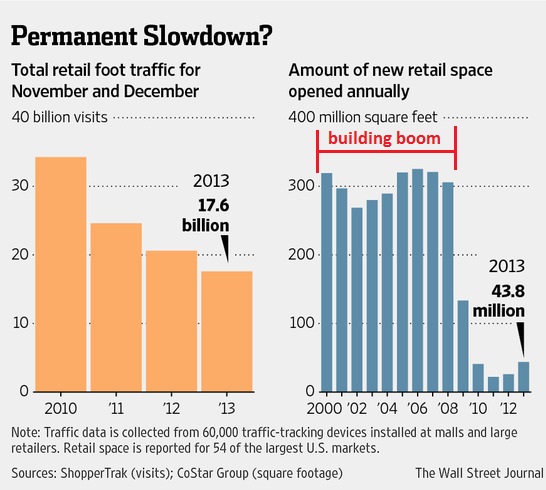

Let's start with two charts of retail that I have marked up: the first is a chart of retail traffic from The Burning Platform story above. Note the phenomenal building boom in retail space from 2000 to 2008: nine straight years of adding about 300 million square feet of retail space each year.

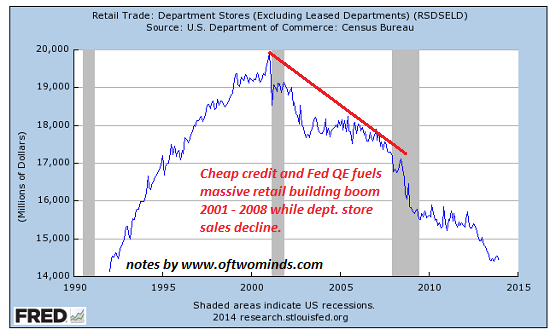

The second chart shows department store sales, which fell by 15% during the retail building boom.

It might be possible to argue that this additional 2.7 billion square feet of retail space was needed as competitors ate the department store chains' lunches, but let's start by considering the foundation of retail sales: consumer income and credit.

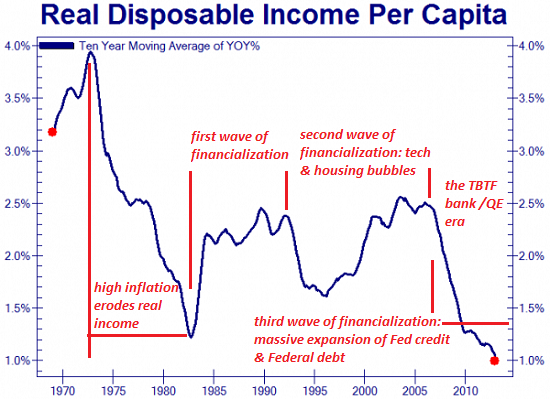

One way to measure income to adjust it for inflation (i.e. real income) and measure it per person (per capita) on a year-over-year (YoY) basis. Notice how real income per capita has absolutely cratered in the "too big to fail" quantitative easing (QE) era masterminded by the Federal Reserve: if this is success, I'd hate to see failure.

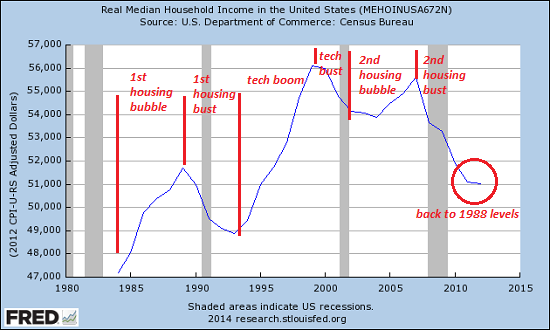

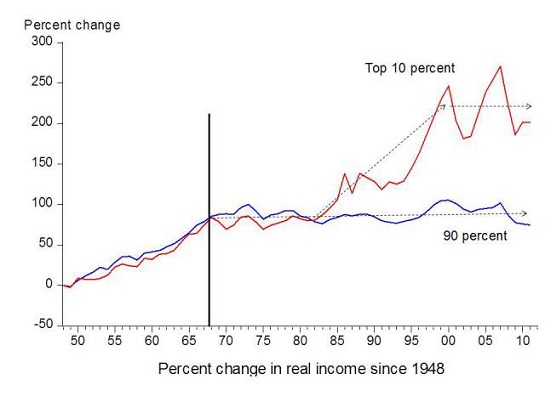

Another way to measure median household income:

Notice how the income of the top 10% diverged from the bottom 90% once the era of financialization and asset bubbles started in the early 1980s. Each asset bubble--housing in the late 1980s, tech in the 1990s and housing again in the 2000s--nudged the incomes of the bottom 90% briefly into marginally positive territory while it spiked the incomes of the top 10% into the stratosphere.

There are only two ways households can buy stuff: with income or credit/debt, as in charging purchases on credit cards. We've seen that income has tanked for the bottom 90%; how about credit/debt?

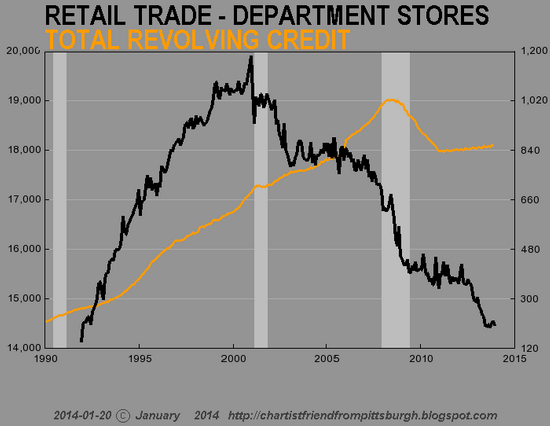

Courtesy of Chartist Friend from Pittsburgh, we can see that revolving consumer credit has flatlined:

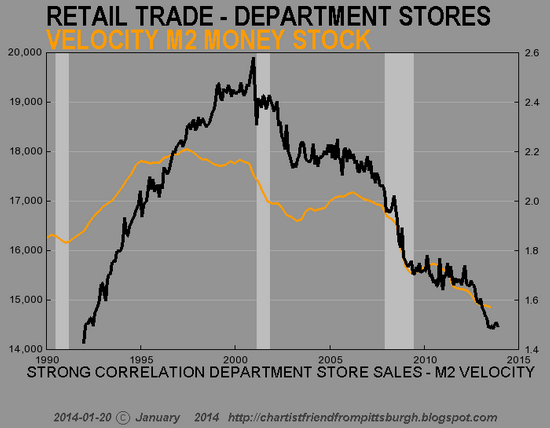

There's another component to the erosion of bricks-n-mortar and the ascent of eCommerce, as Chartist Friend from Pittsburgh explains:

This M2 (money) velocity chart is better because it reminds us of the days when you would drive to the mall to make a purchase, and while you were there you'd stop at the food court to have lunch, and then maybe you'd walk around afterwards and see some other item you wanted to buy, or run into friends and decide to catch a movie or have a drink, etc. At the mall there are lots of ways for money to change hands - online not so much.

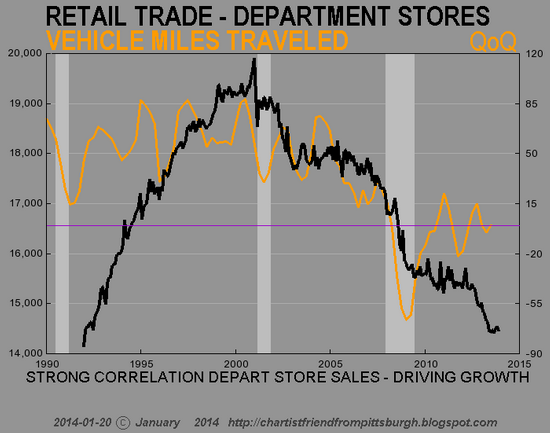

Fewer trips to the mall (correlated to maxed out credit cards, declining real disposable income and the ease of online shopping) also translates into fewer miles driven and fewer gallons of gasoline purchased:

All this boils down to one simple question: can the top 10% (roughly 11 million households) support the billions of square feet of retail space that were added in the 2000s? If the answer is no, as it clearly is, then the retail CRE sector is doomed to implode.

Let's try a second simple question: what's holding the retail CRE sector up?Answer: leases that will soon expire or be voided by insolvency, bankruptcy, etc. as retailers close stores and shutter their businesses.

One last question: who's holding all the immense debt that's piled on top of this soon-to-collapse sector? The domino of retail CRE will not fall in isolation; it will topple the domino of debt next to it, and that will topple the lenders who are bankrupted by the implosion of retail-CRE debt. And once that domino falls, it will take what's left of the nation's illusory financial stability down with it.

The Nearly Free University and The Emerging Economy:

The Revolution in Higher Education

Reconnecting higher education, livelihoods and the economyWith the soaring cost of higher education, has the value a college degree been turned upside down? College tuition and fees are up 1000% since 1980. Half of all recent college graduates are jobless or underemployed, revealing a deep disconnect between higher education and the job market.

It is no surprise everyone is asking: Where is the return on investment? Is the assumption that higher education returns greater prosperity no longer true? And if this is the case, how does this impact you, your children and grandchildren?

We must thoroughly understand the twin revolutions now fundamentally changing our world: The true cost of higher education and an economy that seems to re-shape itself minute to minute.

The Nearly Free University and the Emerging Economy clearly describes the underlying dynamics at work - and, more importantly, lays out a new low-cost model for higher education: how digital technology is enabling a revolution in higher education that dramatically lowers costs while expanding the opportunities for students of all ages.

The Nearly Free University and the Emerging Economy provides clarity and optimism in a period of the greatest change our educational systems and society have seen, and offers everyone the tools needed to prosper in the Emerging Economy.

Read Chapter 1/Table of Contents

print ($20) Kindle ($9.95)

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify. We will cover the five core reasons why things are falling apart:

1. Debt and financialization

1. Debt and financialization2. Crony capitalism

3. Diminishing returns

4. Centralization

5. Technological, financial and demographic changes in our economy

Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Once we accept responsibility, we become powerful.

Read the Introduction/Table of ContentsKindle: $9.95 print: $24

| Thank you, Eric T. ($100), for your outrageously generous contribution to this site-- I am greatly honored by your steadfast support and readership. |