Living on Uneasy Street

It's nice to anticipate sunny weather, but it's a good idea to carry an umbrella just in case the forecasts prove overly optimistic.

Yes, the market will rally if World War III didn't start last night. The market will also rally if World War III does start, because the Federal Reserve will surely lower interest rates.

We chuckle uneasily at gallows humor here on Uneasy Street because we're still required to maintain an upbeat veneer of endlessly cheerful optimism even as we sense that the forces currently in play are beyond the control of individuals or groups, no matter how powerful they may be, and that these forces will follow a course to an end no one can predict with any degree of upbeat confidence.

Back when we lived on Easy Street, things were getting better for everyone in varying degrees and the ladder of social mobility was available to all: anyone could improve their prospects by putting in the effort.

Fortunes were being minted, lists of reasons to be optimistic proliferated like overfed rabbits and spots of bother ran off the road on their own, requiring nothing of us.

Life on Uneasy Street is, well, different. The lists of reasons to be optimistic are still everywhere, but they now ring hollow, as those conjuring the lists sound increasingly frantic: come on, people, get with the program, it's all gonna be wunnerful, AI, AI, AI, Roaring 20s, blah blah blah.

The only true believers are those paid to shill the optimism by those seeking to maximize their profits via selling the sizzle rather than the actual steak. The entire exercise of trying to convince us that we still live on Easy Street is simply more evidence that Easy Street is a figment of imagination.

Now that various forces have been unleashed, gravity and the lay of the land will dictate the course of history. Yes, yes, our technological powers are god-like, we're going to Mars, there's a new (and immensely profitable, of course) technological solution to every problem, so just buy, buy, buy the latest gadget or med: imagine that, you can talk to your refrigerator! Wow. That solves a ton of pressing problems.

Too bad the fridge fails in a few years and has to be replaced, the med must be taken forever or your ill health returns, the side effects require a couple more meds, each of which has their own side effects, and going to Mars has no causal connection to actually solving problems here on Earth with some new technology.

Cycles play out despite our cheerleading inspirational rah-rah. Humans respond the same old way to the tightening of various screws: they start hoarding what's scarce, start seeing conquest and war as the go-to solutions to scarcities and rivalries, reasons to cooperate wither under the relentless sun of crisis while reasons to disagree proliferate most disagreeably like noxious weeds.

Just like all the other creatures on the planet, humans expand their consumption and numbers in times of plenty and are unprepared for the inevitable asymmetries of supply (stagnant or declining) and demand--forever rising, as growth is the one essential for the status quo, regardless of ideological type or label.

As supplies no longer exceed demand, inflation (loss of purchasing power of wages) eats the bottom 90% alive, while the rise of debt that so wondrously expanded the asset wealth of the top 10% starts eating its own tail, as interest rises faster than wages or actual production.

Various grandiose solutions are promoted that claim to fix the pressing problems. Some are absurd techno-fantasies (huge mirrors to deflect solar radiation--never mind the increasingly untenable cloud of space junk orbiting Earth), and some sound appealing but are not as painless as advertised, for example, the clearing away of all debt with a jubilee in which all debts are instantly forgiven.

A debt jubilee is certainly appealing to debtors and those who see the cliff ahead, but recall that all debt is an asset that is holding up an asset class far larger than the debt itself: mortgage debt is what props up the entire global real estate market, and what happens to valuations when debt ceases to exist?

Those who see jubilee as a solution also tend to ignore that all this debt is an asset of which 90% is owned by the wealthy class who run the status quo. Every bond, every mortgage-backed security and every bundled student loan / auto loan is an asset owned by someone or some entity who depends on that asset and its income stream for their wealth and thus their political power.

To hazard a guess based on human history, the wealthy / powerful will probably not be too keen to surrender the vast majority of their wealth and thus their power in the laudable pursuit of eliminating all debt and starting over.

Again based on the usual human responses to decay, decline, scarcities and threats to "what's mine," we can anticipate the elite's preference for a messy, chaotic form of jubilee in which various borrowers default and the underlying assets that provided collateral for the loan will be liquidated.

The elite hope that this messy, chaotic form of jubilee will reduce the debt so gradually that the system that benefits them will continue on its merry way. This hope is misplaced, however, for when collateral gets auctioned off at bargain prices, the value of all other similar assets drops accordingly.

And since nobody wants to catch the falling knife of crashing valuations, buyers are scarce, so the selling begets more selling and prices are pressured lower. Those who reckoned they were "buying the bottom" are wiped out, increasing the reluctance of survivors to take the risk of buying assets which could get much cheaper.

Soaring defaults tend to self-reinforce via feedback as the herd gets skittish and the appetite for risk vanishes like early morning mist in Death Valley. As buyers of crashing assets are carried out on stretchers, those who still own the sinking assets are watching their treasured wealth disappear, so they sell--at first with high expectations, and eventually in pure panic.

The future looks cloudy here on Uneasy Street, and everyone's still hoping for sunny days rather than a deluge. It's nice to anticipate sunny weather, but it's a good idea to carry an umbrella just in case the forecasts prove overly optimistic.

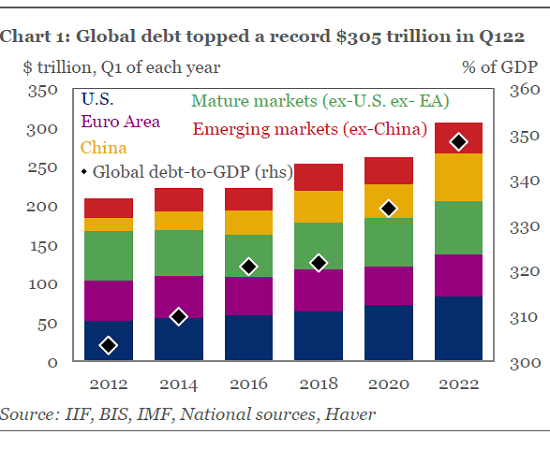

Here are three snapshots of what we're told is Easy Street: global debt skyrocketing:

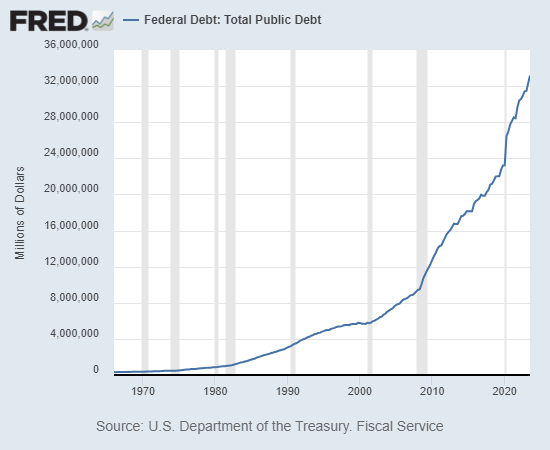

Federal debt skyrocketing:

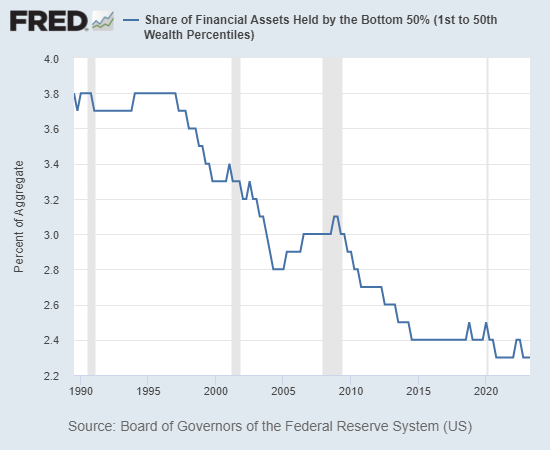

Financial wealth of the bottom 50% plummeting:

But think of the opportunities pre-cliff-dive:

As assets are liquidated, look for "likes" and upbeat Yelp reviews:

My recent books:

Disclosure: As an Amazon Associate I earn from qualifying purchases originated via links to Amazon products on this site.

Self-Reliance in the 21st Century print $18, (Kindle $8.95, audiobook $13.08 (96 pages, 2022) Read the first chapter for free (PDF)

The Asian Heroine Who Seduced Me (Novel) print $10.95, Kindle $6.95 Read an excerpt for free (PDF)

When You Can't Go On: Burnout, Reckoning and Renewal $18 print, $8.95 Kindle ebook; audiobook Read the first section for free (PDF)

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States (Kindle $9.95, print $24, audiobook) Read Chapter One for free (PDF).

A Hacker's Teleology: Sharing the Wealth of Our Shrinking Planet (Kindle $8.95, print $20, audiobook $17.46) Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $5, print $10, audiobook) Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake (Novel) $4.95 Kindle, $10.95 print); read the first chapters for free (PDF)

Money and Work Unchained $6.95 Kindle, $15 print) Read the first section for free

Become a $3/month patron of my work via patreon.com.

Subscribe to my Substack for free

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Suzanne S. ($70), for your magnificantly generous subscription to this site -- I am greatly honored by your steadfast support and readership. |

Thank you, Herb S. ($150), for your outrageously generous subscription to this site -- I am greatly honored by your steadfast support and readership. |

|

|

Thank you, Mike S. ($70), for your splendidly generous subscription to this site -- I am greatly honored by your steadfast support and readership. |

Thank you, Sebastian S. ($70), for your superbly generous subscription to this site -- I am greatly honored by your steadfast support and readership. |