Geithner's conclusion: current policy extremes, politics and astounding debt levels limit policymakers' emergency options in the next crisis.

Many of us disagree with the bloviated, self-congratulatory notion that the Federal Reserve and the U.S. Treasury saved the U.S. economy, capitalism and everything else in 2008-09 up to and including the Central Bank of Mars and the bat guano futures market.

That said, I found myself in agreement with Timothy Geithner's recent assessment of systemic risk and the limits of regulation published in Foreign Affairs magazine: Are We Safe Yet? How to Manage Financial Crises(subscription/registration required)

Geithner starts with some refreshingly straight talk: financial systems are inherently fragile and prone to panics and runs. This echoes what Alan Greenspan wrote in the pages of his own analysis of inherent financial fragility in Foreign Affairs Never Saw It Coming: Why the Financial Crisis Took Economists By Surprise.

"The danger is particularly acute in periods that see both large increases in wealth and optimistic beliefs about the economy--that the economy is safe, that risky assets will rise in value, that liquidity is freely available, and so on."

Like now, right? Geithner goes on to describe the unknown unknowns of risk-off contagion:

"Panics, although scary and dangerous, don’t inevitably end in economic crashes. Much of what determines the severity of the outcome is the quality of the policy choices made in the moment. When expected losses to the value of assets appear very large, there will be uncertainty about which party will bear those losses. This uncertainty can lead to a general reduction in funding for a broad range of financial institutions. That, in turn, can force those institutions to liquidate assets at fire-sale prices, which, if used to measure the riskiness of assets across the system, will make large parts of the financial system appear to be insolvent. This dynamic is not self-correcting. Left unchecked, it will simply accelerate.

Nor are the dynamics of contagion fully knowable in advance. To paraphrase Ernest Hemingway, runs happen gradually, then suddenly. Their characteristics and severity depend on how things evolve in the event and on what policymakers do in response. What matters most are not the first-round effects of direct losses from the defaults of the weakest firms or even the linkages among those firms. Rather, what drives contagion is an increase in the perceived risk that a large number of firms could fail."

While giving lip-service to the benefits of accepting losses, Geithner sees the state as the key player in any crisis. While I don't agree with the idea that the only way to avoid depression is for the state/central bank to backstop everyone, it's easy to see the logic once you accept Geithner's claim that policymakers "cannot eliminate the inherent fragility of the financial system, and they cannot escape the reality that its survival requires extraordinary intervention on the part of the state."

Where I once again find myself in agreement is when Geithner explains why additional regulation doesn't reduce systemic fragility--rather, it increases it:

"There is no reason to be more confident about policymakers’ ability to defuse financial booms or head off financial shocks preemptively. Central banks and international financial institutions have made huge investments in producing sophisticated charts aimed at identifying early warning indicators of systemic risks. But financial crises cannot be forecast. They happen because of inevitable failures of imagination and memory. Financial reforms cannot protect against every conceivable bad event. So it is important to recognize that the overall safety of the financial system--and the health of the broader economy--hinges on more than just the strength of financial regulation."

Geithner's conclusion: current policy extremes, politics and astounding debt levels limit policymakers' emergency options in the next crisis which Geithner concedes is inevitable given the inherent instability of our financial system.

"Solvency problems become more likely to be treated as liquidity problems. The government delays action until the only remaining options are even less politically appealing."

Geithner's proposed solution is basically unlimited state/central bank power to backstop anyone and everyone and create unlimited credit on demand:

"The right regime should recognize that successful crisis management requires allowing the government and the central bank to take risks that the market will not take and absorb losses that the market cannot absorb. It should allow the government to act early, before a panic gains momentum. And it should establish an overarching goal of preserving the stability of the whole system and restoring its capacity to function--not avoiding the failure of individual firms."

While I am not persuaded that repeating the unlimited liquidity/credit "fix" of 2008-09 will resolve the next crisis, I do agree that the room to maneuver is shrinking. The American public has little stomach for another massive bailout of super-wealthy bankers and financiers, and the public is equally wary of granting the Fed the ability to buy staggering quantities of stocks, empty malls, bat guano futures and everything else the Fed will have to buy to keep the markets aloft forever.

What Geithner is unwilling to say is what's obvious: now that policymakers have shot their wad and the room for maneuver is limited, there can't be a centralized, painless "fix" for the next inevitable financial crisis.

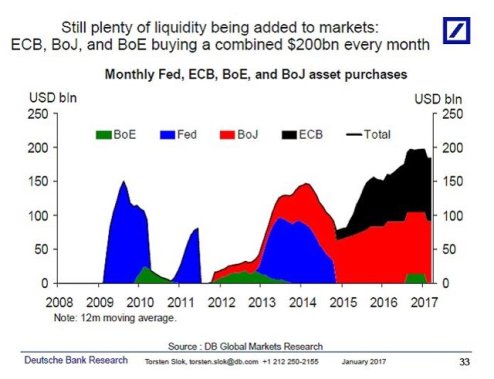

Eight years after the crisis of 2008-09, central banks are still propping up a fragile, sick-unto-death financial firetrap:

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com.

Check out both of my new books, Inequality and the Collapse of Privilege ($3.95 Kindle, $8.95 print) and Why Our Status Quo Failed and Is Beyond Reform ($3.95 Kindle, $8.95 print). For more, please visit the OTM essentials website.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Carol V.B. ($50), for your superbly generous contribution to this site -- I am greatly honored by your support and readership.

|

Thank you, Robert B. ($100), for your outrageously generous contribution to this site -- I am greatly honored by your steadfast support and readership.

|