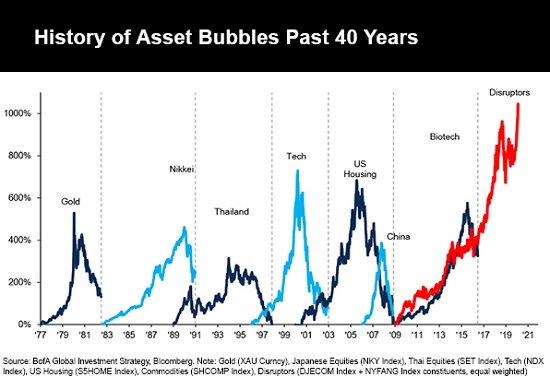

Bubbles always burst, and the confidence that "this isn't a bubble" and "the Fed has our back" are counter-indicators.

Here we go again: stocks have once again reached nosebleed valuations completely disconnected from reality--in other words a repeat of the speculative-frenzy bubble that reached its peak on February 19. Once again, stocks are sporting delusional GDP-to-valuation and P-E (price-earnings) ratios, all based (again) on the belief that nothing--certainly not revenues, profits, debt levels, etc.--matters; the only thing that matters is the Fed pimping stocks.

What might observant punters have learned from the February 19 bubble popping? For one thing, the complacent belief that every technician's target is guaranteed is suspect: at this writing, the vast majority of technical-analysis targets are much higher.

What's the basis for these higher targets? Nothing but the implicit quasi-religious faith in the Fed.

For another, the belief that the market will give every punter an ample opportunity to sell once those targets are reached is equally suspect. Wouldn't it be nice if every punter that sees a target for the 61.8% Fibonacci level, etc. can wait for that target and then cash out, as if nobody else (or ten thousand trading bots) aren't planning to sell at the same target?

One often overlooked characteristic of stock market bubbles is the extremely small exit for sellers trying to avoid becoming impoverished bagholders. Bubbles always present small exits because once sentiment turns, buyers vanish and so price goes over the waterfall and crashes on the rocks below (accompanied by the screams of all the punters who reckoned they'd exit at the top).

For an example, please review a chart of stock market action between March 1 and March 23.

But modern markets have characteristics which have further diminished the exit to a tiny pinhole. These include (but are not limited to):

1. The dominance of index funds. When shares of the index are sold, every constituent stock gets sold. This triggers cascades of selling that overwhelm "buy the dip" buying.

2. Computers do most of the trading, and the algorithms are set to follow trends with extreme ferocity. Once the trend is "sell," the program selling will self-reinforce the cascade.

3. Central banks have generated a mesmerizing moral-hazard propaganda field that implicitly suggests "we'll never stocks go down again, ever!" Yet the only way central banks can causally intervene is to buy stocks directly in size, i.e. in the trillions of dollars. (Recall U.S. stocks are around $30 trillion, global stock markets about $80 trillion. Yes, buying futures contracts through proxies works in stable markets, but not so much in panic cascades of selling.)

Beneath the illusory stability, modern markets are extremely illiquid, meaning that when the bubble pops and punters/money managers try to sell, there are no buyers at any price.

Liquidity in a crash depends on "buy the dip" bagholders. Once they've been destroyed, there are no more buyers at any price. The "buy the dip" crowd will be wiped out after the first spike higher fails, and then nobody will be left who's willing to catch the falling knife.

It's illuminating to go back to to former Federal Reserve chairman Alan Greenspan's 2014 belated bleatings in Foreign Affairs, Why I Didn't See the Crisis Coming. Greenspan presented one primary reason: the Fed's models failed to accurately account for "tail risk," (otherwise known as things that supposedly happen only rarely but when they do happen, they're a doozy), because guess what--they happen more often than statistical models predict.

"Tail risk" is a fancy way of saying that bagholders willing to buy the dip and be destroyed as the crash gathers momentum are too scarce to stop the waterfall of selling. That leaves everyone with a long position in stocks with a binary choice: either grasp the fleeting advantage of selling out in the first wave of selling--and by the way, there's no advantage unless every single share is sold--or become a hapless bagholder.

Bubbles always burst, and the confidence that "this isn't a bubble" and "the Fed has our back" are counter-indicators of just how crushing the pop will be: the greater the confidence/euphoria, the greater the crash.

Sober up, people. All bubbles pop, and the higher the extreme, the greater the crash. Only the first sellers will escape; everyone who hesitates or "buys the dip" will be crushed at the bottom of the waterfall.

If you want to sell your shares to bagholders, issue technical targets way above current levels and year-end targets at nonsensically lofty levels, then sell, sell, sell as the over-confident bagholders buy, buy, buy. ("But Mr. Pundit said the S&P 500 was gonna go higher, he promised!")

Who goes into the market planning to buy at technical levels where everybody else is selling? How many "dumb money bagholders" does everyone reckon will be anxious to buy their shares at the top of the craziest overvalued bubble ever?

Here we go again: only two months after "buy the dip" and "the Fed has our backs" failed, the pundits and money managers are falling over themselves to declare "the bottom is in," "there's now light at the end of the tunnel," and all the other reasons to complacently hold on and become a bagholder so the smart money can sell to you before the anointed TA targets are reached.

Audiobook edition now available:

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World ($13)

(Kindle $6.95, print $11.95) Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World ($13)

(Kindle $6.95, print $11.95) Read the first section for free (PDF).

Pathfinding our Destiny: Preventing the Final Fall of Our Democratic Republic ($6.95 (Kindle), $12 (print), $13.08 ( audiobook): Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake $1.29 (Kindle), $8.95 (print); read the first chapters for free (PDF)

Money and Work Unchained $6.95 (Kindle), $15 (print) Read the first section for free (PDF).

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com.

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Jesse R. ($5/month), for your superbly generous pledge to this site -- I am greatly honored by your support and readership.

|

Thank you, John L. ($5/month), for your splendidly generous pledge to this site -- I am greatly honored by your support and readership.

|