You Can't Separate Empire, the State, Financialization and Crony Capitalism: It's One Indivisible System

The great irony is what's unsustainable melts into thin air no matter how many people want it to keep going.

Disagreement is part of discourse, and pursuing differing views of the best way forward is the heart of democracy. Disagreement is abundant, democracy is scarce, despite claims to the contrary.

If you think you can surgically extract Empire from the American System, force the State to serve the working/middle classes, end the stripmining of financialization, limit crony capitalism/regulatory capture and get Big Money out of politics--go ahead and do so. I'm not standing in your way--go for it.

But while you pursue your good governance, populist, Left/ Right /Socialist/ Libertarian, etc. reforms, please understand the system is indivisible: the Deep State, the Imperial Project (hegemony and power projection), the State, finance in all its tenacled control mechanisms (greetings, debt-serfs and student-loan-serfs), crony capitalism /regulatory capture, money buying political influence, media propaganda passing as "news", and the evisceration of democracy (something untoward could happen if the serfs could overthrow the Power Elite at the ballot box--can't let that happen)--it's all one system.

Should any one organ be ripped from the body, the entire body dies. The entire system defends each subsystem as integral as a matter of survival. As a result, the naive notion that big money can be excised with only positive consequences is false: restoring democracy places the entire system at risk of implosion.

No more bread and circuses, no more Social Security checks, no more state employee pensions--it all melts into air if any subsystem stops doing its job.

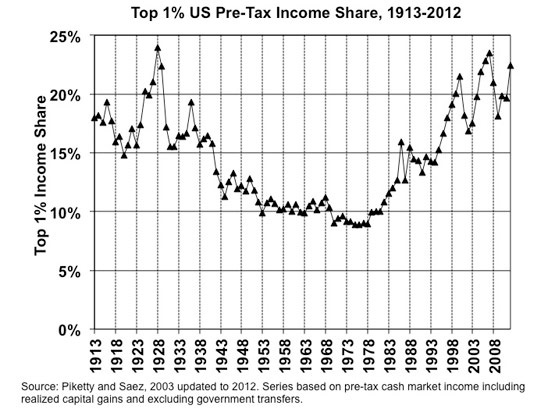

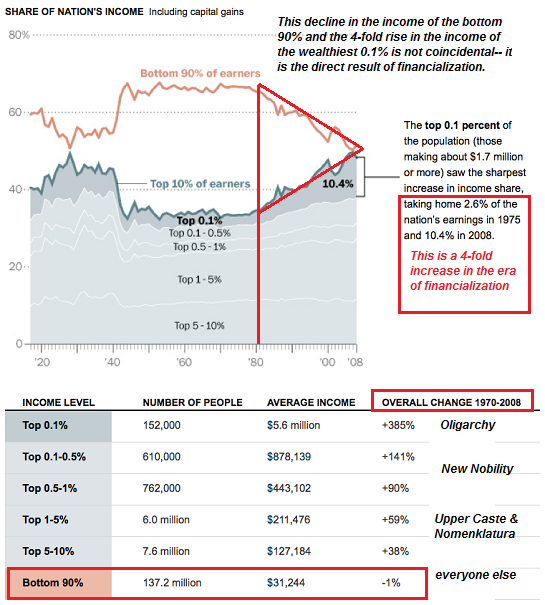

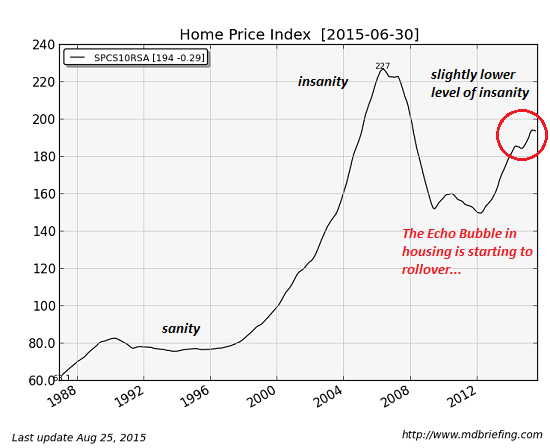

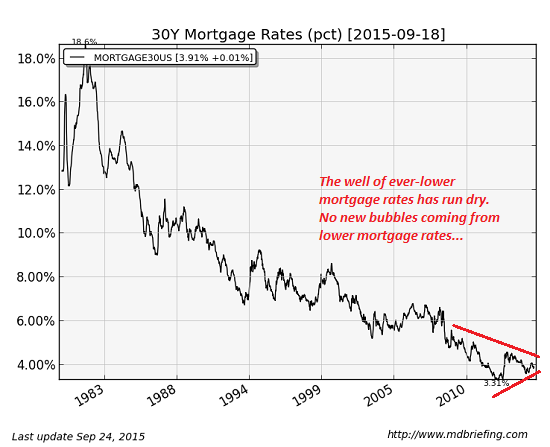

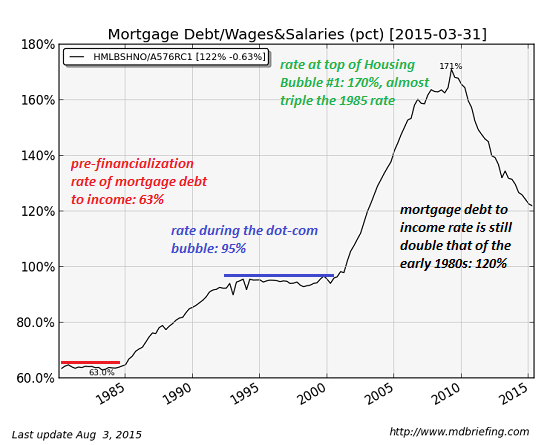

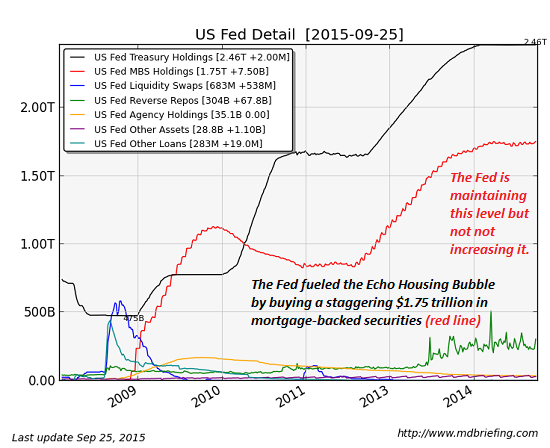

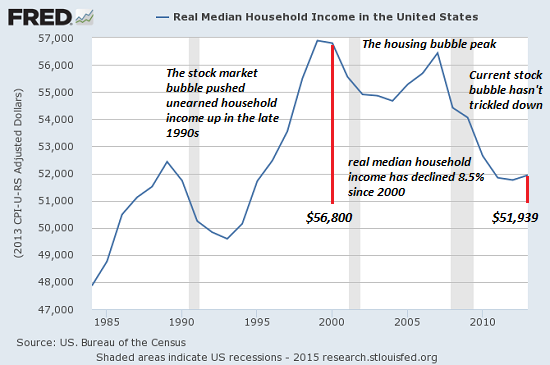

The system is interdependent. Each subsystem needs the others to function. I drew up a chart of the major components (but by no means all) of the system:

The system is a machine in which each gear serves the whole. So go ahead and try to "reform" the system by extracting whatever gear you don't approve of: the Deep State components, the Security State organs, the Federal Reserve, cartels/monopolies enforced by the State, the suppression of democracy, crony capitalism, whatever.

The machine will resist your "reform" to the death because should you succeed, the machine will implode. Take out the financialization gear and the financial system collapses.

So go ahead and reform to your heart's content. Go ahead and believe the system is reformable, if it makes you feel better. Vote for Bernie or The Donald or whomever. Go ahead and disagree with me. Prove me wrong. Prove the State really, really, really wants to serve the working/middle class rather than the Empire that it is. Pursue your Left/ Right/ Socialist/ Libertarian fantasies of righting the Imperial Project by ripping the gears out of the very center of the machine.

It doesn't work that way. We can't remove the gears we find distasteful. Either the machine grinds on and we get our share of the swag--bread and circuses, corporate welfare, State jobs and pensions, Medicaid and Medicare, and all the rest of the immense swag of hegemony and the Imperial Project--or the system implodes and all the swag melts into air.

The great irony is what's unsustainable melts into thin air no matter how many people want it to keep going.

But go ahead and disagree. It's your right, by golly. Go ahead and try to "reform" the system and see how far you get.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Michael M. ($50), for yet another fabulously generous contribution to this site -- I am greatly honored by your steadfast support and readership.

|

Thank you, Seth F. ($5), for your most generous contribution to this site -- I am greatly honored by your support and readership.

|