The New Normal: Extremes of Neofeudalism, Incompetence, Authoritarianism and Relocalization

The pendulum swung to an extreme of globalization, financialization, centralization and monopoly, all of which created extreme systemic fragility.

Here's what to expect in the rapidly evolving New Normal: extremes become even more extreme as the status quo attempts to force compliance with its last-ditch schemes to preserve what was always unsustainable while painting a happy face on the stock market, the one thing they can push higher as the global economy unravels.

Mark, Jesse and I discuss this dynamic in Salon #10: Remember when Maximum Pessimism and Irrational Exuberance were mutually exclusive? (54 minutes): realistic pessimism is lashed to the mast with the irrational exuberance of stock market soothsayers, central bank cheerleaders and the organs of propaganda (Wall Street) and control of the narratives (social media and search monopolies).

Cognitive dissonance? Yes. Schizophrenia? Sure. Crazy-making? Undoubtedly. So the default "solution" is petty Authoritarianism to ensure we only see approved narratives, that we focus on the happy-happy signal of the glorious stock market (best rally ever!), that we pay higher taxes without complaint, and so on.

And of course, buy, buy, buy and borrow, borrow, borrow, lest the flimsy house of cards collapse.

As I explain in my book Why Our Status Quo Failed and Is Beyond Reform, the only possible output of central bank monetary stimulus is financialization, and the only possible output of financialization is unprecedented wealth and income inequality.

As Max Keiser, Stacy Herbert and I discuss in Fractals of Incompetence (15:30), the problem with pushing extremes is the system is incompetent at every level, from school boards to the Federal Reserve. Rather than solve problems, our institutions have devolved into mechanisms to protect clerisy / insiders from transparency and accountability.

In the New Normal, systemic incompetence isn't going to magically transform into competence, it's going to reach new extremes of incompetence and self-serving hubris.

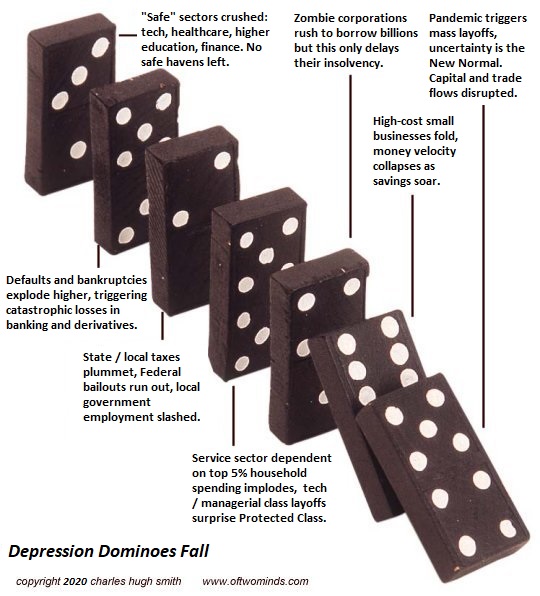

My term for servitude via debt and taxes is neofeudalism, and neofeudalism is the default setting of the New Normal as the super-wealthy can buy even more of the nation's assets thanks to the Federal Reserve's free money for financiers, leaving the peasantry the owners of debt rather than assets.

The only way to escape neofeudal servitude is to figure out some way to live on a fraction of what the conventional lifestyle requires, i.e. radical frugality. Radical frugality will also be a permanent part of the New Normal, either voluntary or imposed by circumstances.

The silver lining in all this is the potential to relocalize essential elements of our economy, a subject Richard and I discuss in The New Normal (37 minutes). The pendulum swung to an extreme of globalization, financialization, centralization and monopoly, all of which created extreme systemic fragility.

In the New Normal, the pendulum will finally start moving away from globalization, financialization, centralization and monopoly to decentralized, relocalized economic activity, which is the core dynamic in doing more with less and regaining agency.

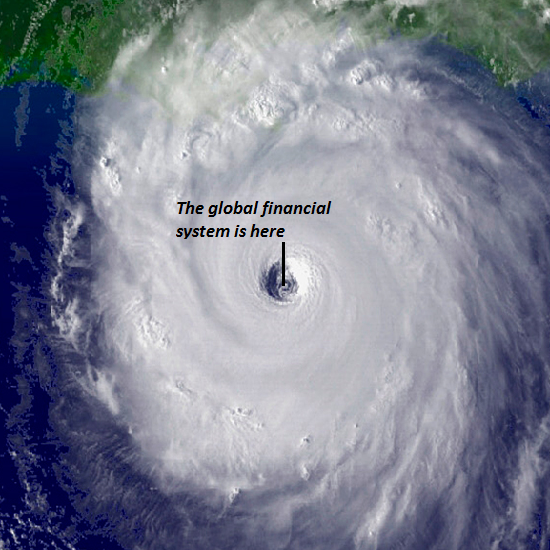

The New Normal has yet to fully impact the global financial system, which is still in the eye of the hurricane, magnificently confident that the Federal Reserve's money-printing is the most powerful force in the Universe. The stock market's hubris is begging the gods for retribution, and we may not have to wait too long for the karmic hammer to crush the hubris and the irrational exuberance, as Adam, Mike, John and I discuss in Three major risks the markets are not pricing in yet (39 minutes).

The winds are picking up, and the flimsy shacks of the Fed and Wall Street are no match for the real world.

Recent Podcasts:

Fractals of Incompetence (15:30)

AxisOfEasy Salon #10: Remember when Maximum Pessimism and Irrational Exuberance were mutually exclusive? (54 minutes)

Charles Hugh Smith on the New Normal (37 minutes)

Audiobook edition now available:

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World ($13)

(Kindle $6.95, print $11.95) Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World ($13)

(Kindle $6.95, print $11.95) Read the first section for free (PDF).

Pathfinding our Destiny: Preventing the Final Fall of Our Democratic Republic ($6.95 (Kindle), $12 (print), $13.08 ( audiobook): Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake $1.29 (Kindle), $8.95 (print); read the first chapters for free (PDF)

Money and Work Unchained $6.95 (Kindle), $15 (print) Read the first section for free (PDF).

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com.

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, James B. ($100), for your outrageously generous contribution to this site -- I am greatly honored by your support and readership.

|

Thank you, Paul M. ($75), for your outrageously generous contribution to this site -- I am greatly honored by your support and readership.

|