STVR/Airbnb Has Destroyed America's Resort Towns

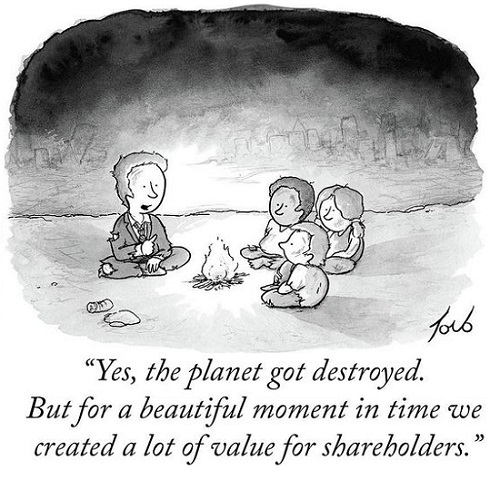

It turns out society isn't just the sum total of the Fed goosing "maximizing shareholder value." People actually have to live in the corrupt, bifurcated, distorted ghetto the Fed and "maximizing shareholder value" have created.

It's an old story, manifesting now in new ways. The rich, buoyed by inherited wealth and access to credit, find a locale with the qualities they desire, and buy the choicest properties for their own use, and a surrounding band of nearby properties so they won't be bothered by the bottom 99%.

This story has a new far more destructive chapter, generated by the boom in STVRs--short-term vacation rentals. The uber-wealthy don't need more money but they're trained, like hamsters in a lab, to seek ways to maximize their income and capital gains. STVRs--Airbnb et al.--are highly attractive investments to the wealthy and their money-managers--the hedge funds, private equity managers, family-wealth advisors, et al.

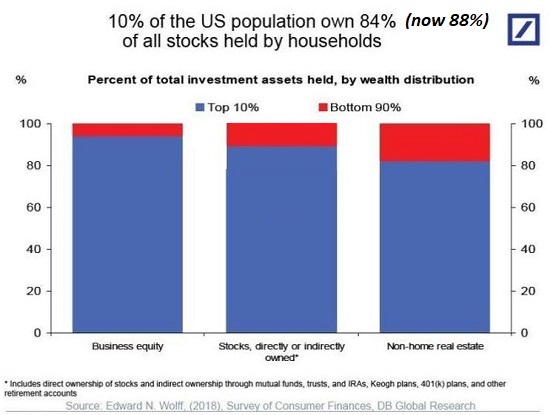

Residential real estate that can be converted to STVRs is well within reach of the top 10% households, who own between 80% and 90% of all income-producing assets such as housing rentals, stocks, bonds and business equity.

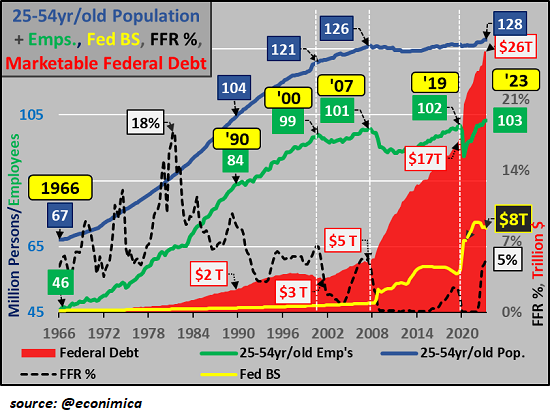

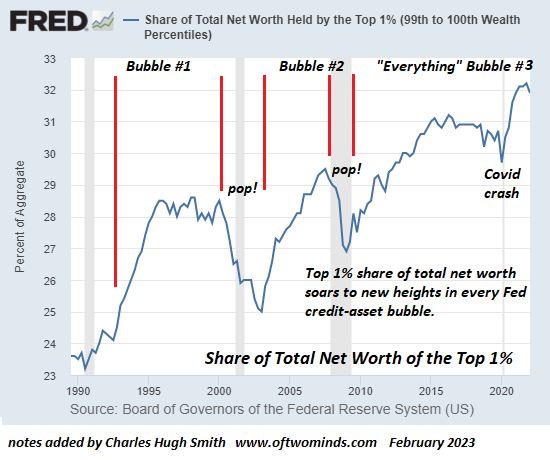

As the Federal Reserve has distorted credit markets with historically unprecedented low interest rates and "excess liquidity," the resulting asset bubbles widened the income-wealth gap between the top 10% who already owned most of the assets soaring in value and the bottom 90% who at best owned a family home with a mortgage.

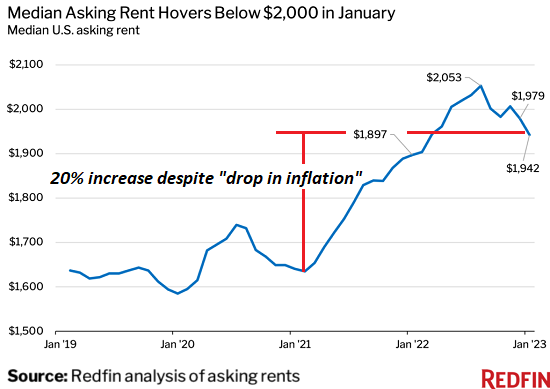

The top 10% saw super-low mortgage rates and the plump returns on STVRs and rushed to snap up any properties that could be converted from long-term rentals to short-term vacation rentals to get their share of the post-pandemic price-insensitive "revenge spending" we-need-a-vacation bonanza.

This mass conversion of long-term rentals for workers into vacation rentals has social and economic consequences. It's bifurcated America's desirable towns into luxe enclaves for the "haves" and ghettos for the working "have-nots." It was all fun and games seeking to "maximize shareholder value" and ride the next bubble to ever greater wealth and income, but the consequence is the destruction of the nation's social and economic fabric.

I asked longtime correspondent W.S., who has witnessed the transformation in Colorado over the decades, to describe the reality generated by the mass conversion of long-term rentals to STVRs. Here is his account:

"Airbnb has devastated Colorado's resort towns.

It's always been expensive to live in places that wealthy people decided they wanted to visit regularly.

Real estate speculators figure out where the money is quickly enough, buy up property, subdivide it and sell lots to their friends, who build second homes, like the single family castles in Beaver Creek and Vail. They build condos and duplexes and sell them to less wealthy folks who want to live in these places and to small investors who rent them to the people who do the actual work in these communities; our teachers, police and fire fighters, hotel and restaurant and small business operators and their staff, the 'essential services' folks that nobody thinks much about until one day, a pandemic comes along.

In Colorado, the attraction for the past 50 years has been downhill skiing and while rents always were higher than most places, the folks that moved up to the mountains and worked at the skico and surrounding small businesses generally skied for free - a season pass was a more common benefit than a healthcare plan - and the 'locals' lived to ride. Snowboards. Skis. It was a worthwhile trade off.

That era ended completely with AirBnb.

Over the past few years virtually all of the 'locals' housing in Vail, the duplexes in nearby Eagle Vail, the houses in Edwards - everything in the upper Eagle River Valley where locals lived - has been purchased - often sight unseen - by hedge funds, private capital and wealthy full and part time homeowners. It has all immediately been turned into short term rental properties (STVRs) - Airbnb, VRBO, etc.

Why rent a two bedroom apartment to a teacher for $1,500 a month when you can Airbnb the same 40 year old unit for $2,500 a week?

Except now, there are literally no housing units available.

Ok, a few pop up now and then but for $3,750 to $4,000 a month, since the work at home class has bid up the price of everything in resort towns with fast internet, and all of them have it. Even if they don't, Starlink is $120 a month for 50-200 MBPS connectivity. (I have it, it's flawless.)

Local teachers with masters degrees start at $45,000 a year, fresh out of school.

A $3,750 per month rental requires about $11,000 to move in, first and last plus the security deposit. The annual rent comes to $45,000. Thats the gross pay for new hires, which we need annually as our experienced educators retire, or sell their homes they bought a few years ago for huge gains and move elsewhere.

We can't hire teachers.

We can't hire snow plow operators, who are sort of essential in the high country.

Can't hire substitute teachers at $100 a day.

Can't hire bus drivers.

Nobody making under $250,000 can buy a house and live here anymore. Wendy's pays $19 an hour to start - but you can't work there unless you live with your folks or 4 roommates (maybe).

It's so bad in Eagle County that the school district is bringing new teachers, fresh graduates from the Philippines. The district is building 37 apartments for them to live in, dorm style. Teaching has become a job only workers imported from other countries can afford to do here, like picking vegetables.

Sure, house prices have gone up a lot because of the influx of work at homers. They'll probably stay, as heat refugees from the southwest begin to migrate to higher altitudes. But the 20-30 year old former rental units the locals started off in? Sorry. They're Airbnb.

With no working people to staff the grocery stores, these mountain towns might not be the refuge the heat refugees seek."

Thank you, W.S., for this insightful on-the-ground report. Is it really that surprising that those who still have to work for a living resent being crammed into ghettos while America's elite class enjoys their Fed-bubble generated wealth and soaring income?

Is it really that surprising that towns swamped with an influx of visitors and wealthy owners are being fouled as their infrastructure is overwhelmed and their natural wealth exploited / stripmined to "maximize shareholder value"?

The Wealthy Are Not Like You and Me--Our Terminally Stratified Society (8/3/23)

Development In A Wealthy Montana Boom Town Is Fouling A World-Class Trout River

There's Gonna be a War in Montana

It turns out society isn't just the sum total of the Fed goosing "maximizing shareholder value." People actually have to live in the corrupt, bifurcated, distorted ghetto the Fed and "maximizing shareholder value" have created.

My new book is now available at a 10% discount ($8.95 ebook, $18 print):

Self-Reliance in the 21st Century.

My new book is now available at a 10% discount ($8.95 ebook, $18 print):

Self-Reliance in the 21st Century.

Read the first chapter for free (PDF)

Read excerpts of all three chapters

Podcast with Richard Bonugli: Self Reliance in the 21st Century (43 min)

My recent books:

The Asian Heroine Who Seduced Me

(Novel) print $10.95,

Kindle $6.95

Read an excerpt for free (PDF)

When You Can't Go On: Burnout, Reckoning and Renewal

$18 print, $8.95 Kindle ebook;

audiobook

Read the first section for free (PDF)

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States

(Kindle $9.95, print $24, audiobook)

Read Chapter One for free (PDF).

A Hacker's Teleology: Sharing the Wealth of Our Shrinking Planet

(Kindle $8.95, print $20,

audiobook $17.46)

Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $5, print $10, audiobook)

Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake (Novel)

$4.95 Kindle, $10.95 print);

read the first chapters

for free (PDF)

Money and Work Unchained $6.95 Kindle, $15 print)

Read the first section for free

Become

a $1/month patron of my work via patreon.com.

Subscribe to my Substack for free

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

|

Thank you, gotomgo ($50), for your magnificently generous Substack subscription to this site -- I am greatly honored by your support and readership. |

Thank you, gunsamerica ($50), for your superbly generous Substack subscription to this site -- I am greatly honored by your support and readership. |

|

|

Thank you, jebervein ($50), for your splendidly generous Substack subscription to this site -- I am greatly honored by your support and readership. |

Thank you, Jim1318 ($50), for your marvelously generous Substack subscription to this site -- I am greatly honored by your support and readership. |