Following in Rome's Footsteps: Moral Decay, Rising Inequality

Here is the moral decay of America's ruling elites boiled down to a single word.

There are many reasons why Imperial Rome declined, but two primary causes that get relatively little attention are moral decay and soaring wealth inequality. The two are of course intimately connected: once the morals of the ruling Elites degrade, what's mine is mine and what's yours is mine, too.

I've previously covered two other key characteristics of an empire in terminal decline: complacency and intellectual sclerosis, what I have termed a failure of imagination.

Michael Grant described these causes of decline in his excellent account The Fall of the Roman Empire, a short book I have been recommending since 2009:

There was no room at all, in these ways of thinking, for the novel, apocalyptic situation which had now arisen, a situation which needed solutions as radical as itself. (The Status Quo) attitude is a complacent acceptance of things as they are, without a single new idea.

This acceptance was accompanied by greatly excessive optimism about the present and future. Even when the end was only sixty years away, and the Empire was already crumbling fast, Rutilius continued to address the spirit of Rome with the same supreme assurance.

This blind adherence to the ideas of the past ranks high among the principal causes of the downfall of Rome. If you were sufficiently lulled by these traditional fictions, there was no call to take any practical first-aid measures at all.

A lengthier book by Adrian Goldsworthy How Rome Fell: Death of a Superpower addresses the same issues from a slightly different perspective.

Glenn Stehle, commenting on a thread in the excellent website peakoilbarrel.com (operated by the estimable Ron Patterson) made a number of excellent points that I am taking the liberty of excerpting: (with thanks to correspondent Paul S.)

The set of values developed by the early Romans called mos maiorum, Peter Turchin explains in War and Peace and War: The Rise and Fall of Empires, was gradually replaced by one of personal greed and pursuit of self-interest.

“Probably the most important value was virtus (virtue), which derived from the word vir (man) and embodied all the qualities of a true man as a member of society,” explains Turchin.

“Virtus included the ability to distinguish between good and evil and to act in ways that promoted good, and especially the common good. Unlike Greeks, Romans did not stress individual prowess, as exhibited by Homeric heroes or Olympic champions. The ideal of hero was one whose courage, wisdom, and self-sacrifice saved his country in time of peril,” Turchin adds.

And as Turchin goes on to explain:

"Unlike the selfish elites of the later periods, the aristocracy of the early Republic did not spare its blood or treasure in the service of the common interest. When 50,000 Romans, a staggering one fifth of Rome’s total manpower, perished in the battle of Cannae, as mentioned previously, the senate lost almost one third of its membership.This suggests that the senatorial aristocracy was more likely to be killed in wars than the average citizen...

The wealthy classes were also the first to volunteer extra taxes when they were needed… A graduated scale was used in which the senators paid the most, followed by the knights, and then other citizens. In addition, officers and centurions (but not common soldiers!) served without pay, saving the state 20 percent of the legion’s payroll...

The richest 1 percent of the Romans during the early Republic was only 10 to 20 times as wealthy as an average Roman citizen."

Now compare that to the situation in Late Antiquity when

"an average Roman noble of senatorial class had property valued in the neighborhood of 20,000 Roman pounds of gold. There was no 'middle class' comparable to the small landholders of the third century B.C.; the huge majority of the population was made up of landless peasants working land that belonged to nobles. These peasants had hardly any property at all, but if we estimate it (very generously) at one tenth of a pound of gold, the wealth differential would be 200,000! Inequality grew both as a result of the rich getting richer (late imperial senators were 100 times wealthier than their Republican predecessors) and those of the middling wealth becoming poor."

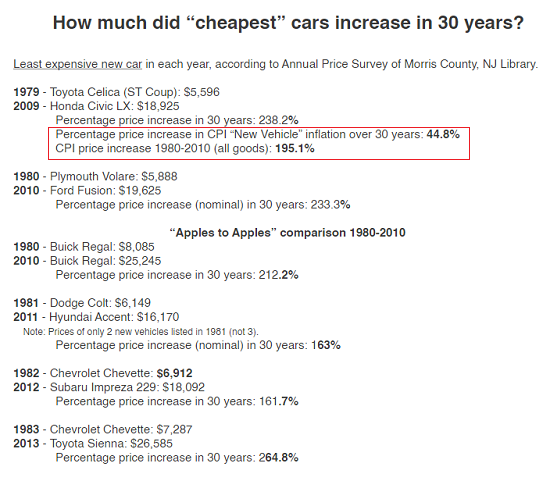

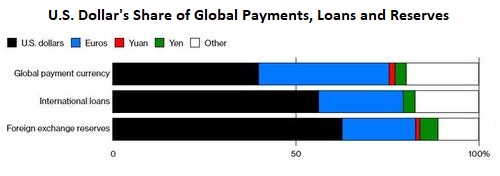

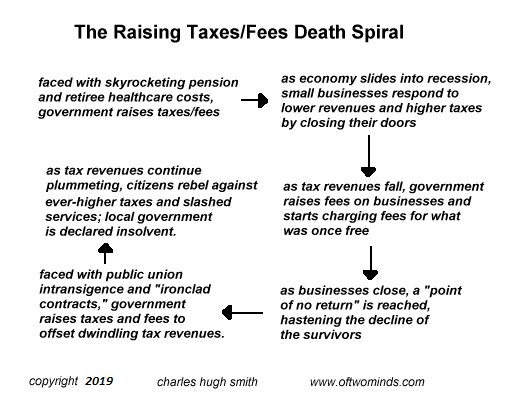

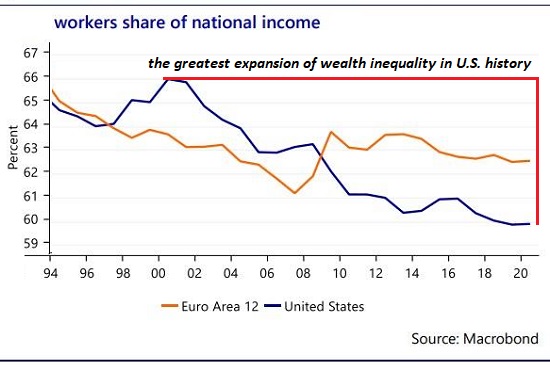

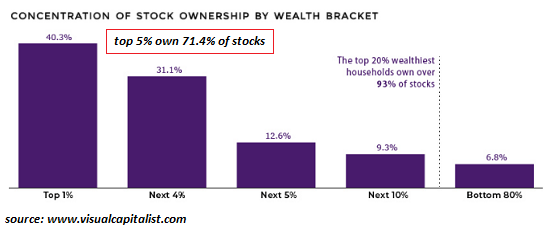

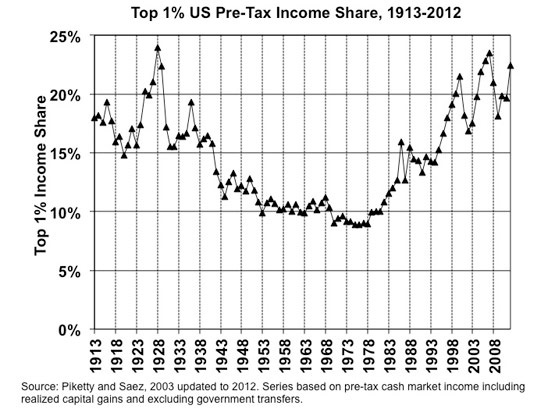

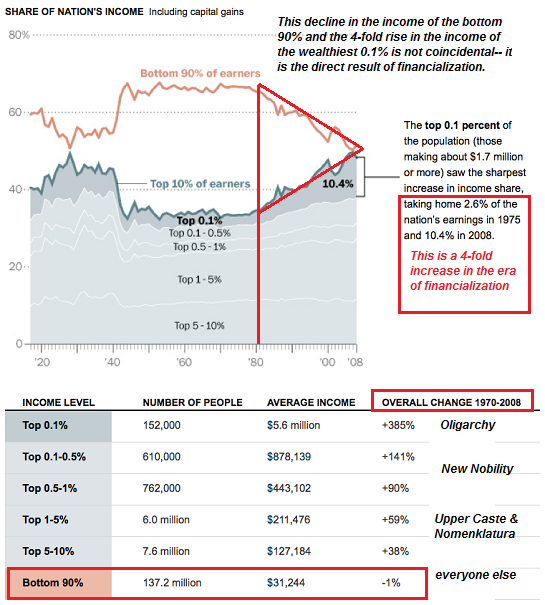

Do you see any similarities with the present-day realities depicted in these charts?

And how many congresspeople served in combat in Iraq or Afghanistan? How many presidential candidates had boots on the ground in combat theaters? The answer is one. Here is the moral decay of America's ruling elites boiled down to a single word.

Pathfinding our Destiny: Preventing the Final Fall of Our Democratic Republic ($6.95 ebook, $12 print, $13.08 audiobook): Read the first section for free in PDF format.

My new mystery The Adventures of the Consulting Philosopher: The Disappearance of Drake is a ridiculously affordable $1.29 (Kindle) or $8.95 (print); read the first chapters for free (PDF)

Pathfinding our Destiny: Preventing the Final Fall of Our Democratic Republic ($6.95 ebook, $12 print, $13.08 audiobook): Read the first section for free in PDF format.

My new mystery The Adventures of the Consulting Philosopher: The Disappearance of Drake is a ridiculously affordable $1.29 (Kindle) or $8.95 (print); read the first chapters for free (PDF)

My book Money and Work Unchained is now $6.95 for the Kindle ebook and $15 for the print edition. Read the first section for free in PDF format.

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com. New benefit for subscribers/patrons: a monthly Q&A where I respond to your questions/topics.

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com. New benefit for subscribers/patrons: a monthly Q&A where I respond to your questions/topics.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Charles R. ($200), for your beyond outrageously generous contribution to this site-- I am greatly honored by your steadfast support and readership.

|