How Much of Your "Wealth" Is Hostage to Bubbles and Impossible Promises?

All asset "wealth" in credit-asset bubble dependent economies is contingent and ephemeral.

A funny thing happens to "wealth" in a bubble economy: it only remains "wealth" if the owner sells at the top of the bubble and invests the proceeds in an asset which isn't losing purchasing power.

Transferring "wealth" to another asset bubble that is also deflating doesn't preserve the "wealth" from evaporation.

All the ironclad promises made in bubble economies ultimately depend on credit-asset bubbles never popping--but sadly, all credit-asset bubbles pop. So all the promises--which are of course politically impossible to revoke--will be broken as all the credit-asset bubbles that created the "wealth" that was to be redistributed--pensions, retirement benefits, etc.--deflate.

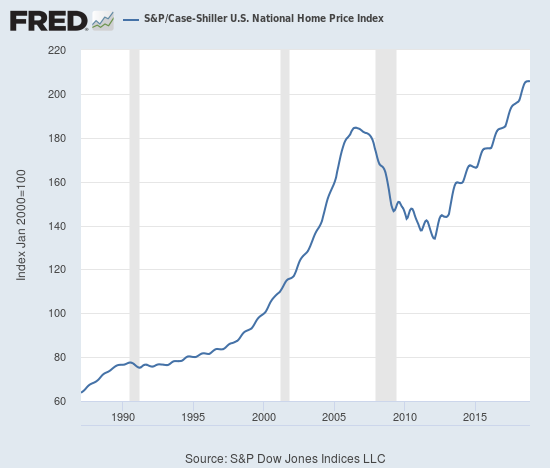

Consider the Case-Shiller housing index chart below. Housing is an asset that has reached the apex of a second bubble. (Stocks are reaching the apex of a third bubble.)

It is widely viewed as "impossible" for the housing market to lose 50% to 75% of its value. It is equally widely viewed as "impossible" for the stock market to lose 50% to 75% of its value.

Yet all credit-asset bubbles pop and lose 50% to 75% of their value--or even more. What's "impossible" isn't the bubbles popping--what's impossible is for bubbles to inflate forever and never pop.

Yet this impossibility is the foundation of all pensions and other promises: the pensions are only payable if all the credit-asset bubbles keep on expanding and never pop. They're also equally dependent on marginal borrowers never defaulting, marginal companies never going belly-up, and marginal speculations never going bust.

But this is precisely what marginal borrowers, companies and speculative ventures do--they blow up and default, delivering neutron-bomb like losses to the lenders: the physical assets remain, but the the "wealth" has been utterly destroyed.

Meanwhile, back at the government ranch, the vast majority of tax revenues are also dependent on credit-asset bubbles never popping. Most of the capital gains taxes reaped in bubbles dry up and blow away, high-earners who pay most of the income taxes lose their jobs or bonuses, and absurdly overvalued real estate that generated outlandish property taxes loses half its value, slashing property tax valuations.

Two retracement levels beckon on the Case-Shiller Home Price Index: a retrace to the previous Bubble #1 lows--a roughly 33% decline--or a full retrace back to pre-Bubble #1 levels, about a 60% drop from current levels.

In bubblicious regions that have seen decaying bungalows on postage-stamp lots rise 10-fold from $100,000 to $1 million, an 80% drop would be expected if history is any guide. This will be quite a shock to buyers who assumed that their home "wealth" would double from $1 million to $2 million.

All asset "wealth" in credit-asset bubble dependent economies is contingent and ephemeral. "Sure things" become less sure when credit bubbles pop and self-reinforcing defaults topple an ever widening circle of dominoes.

How much of your "wealth" is tied up in bubbles and impossible-to-keep promises? Only those who sell at the top before the herd panics and move their "wealth" into the few assets that are maintaining or gaining their purchasing power will still have their "wealth" after the conflagration turns credit-bubble "wealth"into ashes.

Pathfinding our Destiny: Preventing the Final Fall of Our Democratic Republic ($6.95 ebook, $12 print, $13.08 audiobook): Read the first section for free in PDF format.

My new mystery The Adventures of the Consulting Philosopher: The Disappearance of Drake is a ridiculously affordable $1.29 (Kindle) or $8.95 (print); read the first chapters for free (PDF)

Pathfinding our Destiny: Preventing the Final Fall of Our Democratic Republic ($6.95 ebook, $12 print, $13.08 audiobook): Read the first section for free in PDF format.

My new mystery The Adventures of the Consulting Philosopher: The Disappearance of Drake is a ridiculously affordable $1.29 (Kindle) or $8.95 (print); read the first chapters for free (PDF)

My book Money and Work Unchained is now $6.95 for the Kindle ebook and $15 for the print edition. Read the first section for free in PDF format.

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com. New benefit for subscribers/patrons: a monthly Q&A where I respond to your questions/topics.

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com. New benefit for subscribers/patrons: a monthly Q&A where I respond to your questions/topics.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Creedon M. ($20), for your most generous contribution to this site-- I am greatly honored by your support and readership.

|