Are We (Collectively) Depressed?

We need to encourage honesty above optimism. Once we can speak honestly, there is a foundation for optimism.

Psychoanalysis teaches that one cause of depression is repressed anger.

The rising tide of collective anger is visible in many places: road rage, violent street clashes between groups seething for a fight, the destruction of friendships for holding the "incorrect" ideological views, and so on. I Think We Can Safely Say The American Culture War Has Been Taken As Far As It Can Go.

A coarsening of the entire social order is increasingly visible: The Age of Rudeness.

This raises a larger question: are we as a society becoming depressed as we repress our righteous anger and our sense of powerlessness as economic and social inequality rises?

Depression is a complex phenomenon, but it typically includes a loss of hope and vitality, absence of goals, the reinforcement of negative internal dialogs, and anhedonia, the loss of the joy of living (joie de vivre).

Depressive thoughts (and the emotions they generate) tend to be self-reinforcing, and this is why it's so difficult to break out of depression once in its grip.

One part of the healing process is to expose the sources of anger that we are repressing. As psychiatrist Karen Horney explained in her 1950 masterwork, Neurosis and Human Growth: The Struggle Towards Self-Realization, anger at ourselves sometimes arises from our failure to live up to the many "shoulds" we've internalized, and the idealized track we've laid out for ourselves and our lives.

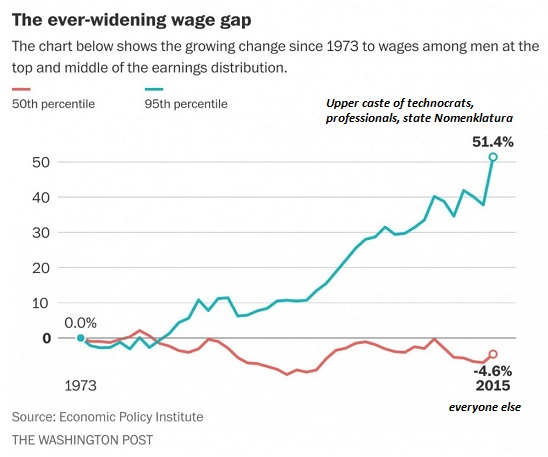

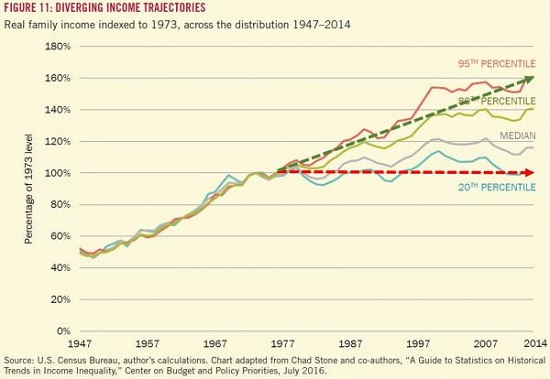

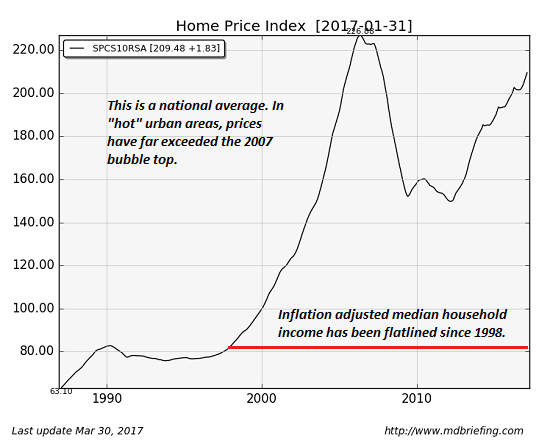

The recent article, The American Dream Is Killing Us does a good job of explaining how our failure to obtain the expected rewards of "doing all the right things"(getting a college degree, working hard, etc.) breeds resentment and despair.

Since we did the "right things," the system "should" deliver the financial rewards and security we expected. This systemic failure to deliver the promised rewards is eroding social mobility and the social contract while generating frustration, anger, etc.

We are increasingly angry at the system, but we reserve some anger for ourselves, because the mass-media trumpets how well the economy is doing and how some people are doing extremely well. Naturally, we wonder, why them and not us? The failure is thus internalized.

One response to this sense that the system no longer works as advertised is to seek the relative comfort of echo chambers--places we can go to hear confirmation that this systemic stagnation is the opposing political party's fault.

We don't just self-sort ourselves into political "tribes" online--we congregate in increasingly segregated communities and states: The Simple Reason Why A Second American Civil War May Be Inevitable.

Americans are moving to communities that align more with their politics. Liberals are moving to liberal areas, and conservatives are moving to conservative communities. It’s been going on for decades. When Jimmy Carter was elected in 1976, 26.8% of Americans lived in landslide counties; that is counties where the president won or lost by 20% of the vote.

By 2004, 48.3% of the population lived in these counties. This trend continues to worsen. As Americans move to their preferred geographic bubbles, they face less exposure to opposing viewpoints, and their own opinions become more extreme. This trend is at the heart of why politics have become so polarizing in America.

We’re self-sorting at every level. Because of this, Americans are only going to grow more extreme in their beliefs, and see people on the other side of the political spectrum as more alien."

Part of the American Exceptionalism we hear so much about is a can-do optimism: set your mind to it and everything is possible.

The failure to prosper as anticipated is generating a range of negative emotions that are "un-American": complaining that you didn't get a high-paying secure job despite having a college degree (or advanced degree) sounds like sour-grapes: the message is you didn't work hard enough, you didn't get the right diploma, etc.

It can't be the system that's failed, right? I discuss this in my book Why Our Status Quo Failed and Is Beyond Reform: the top 10% who are benefiting mightily dominate politics and the media, and their assumption is: the system is working great for me, so it must be working for everyone. That's the implicit narrative parroted by status quo mouthpieces.

The inability to express our despair and anger generates depression. Some people will redouble their efforts, others will seek to lay the blame on "the other" (some external group) and others will give up. What few people will do is look at the sources of systemic injustice.

Perhaps we need a national dialog about declining expectations, rising inequality and the failure of the status quo that avoids the blame-game and the internalization trap (i.e. it's your own fault you're not well-off).

We need ways to express our resentment, anger, despair, etc. that are directed at the source, the complex system we inhabit, not "the other." We need to encourage honesty above optimism. Once we can speak honestly, there is a foundation for optimism.

This essay was drawn from Musings Report 16. The weekly Musings Reports are emailed exclusively to major contributors/ subscribers /patrons ($5/month or $50/year).

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com.

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com.

Check out both of my new books, Inequality and the Collapse of Privilege ($3.95 Kindle, $8.95 print) and Why Our Status Quo Failed and Is Beyond Reform ($3.95 Kindle, $8.95 print, $5.95 audiobook) For more, please visit the OTM essentials website.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Chris H. ($100), for your outrageously generous contribution to this site -- I am greatly honored by your longstanding support and readership.

|

Thank you, Russ R. ($5/month), for your supremely generous renewed subscription to this site -- I am greatly honored by your steadfast support and readership.

|