Withdrawing from the Rat Race Is Going Global

Mere mortals are left in a hopeless situation. In response, they're withdrawing from the competition en masse.

The world has changed over the past two generations in ways that don't fit the heavily promoted narratives of "growth" and "progress." The "growth" and "progress" narratives hold that everything is getting better in every way and every day--next stop, Mars!--but if we consider everyday life, a much different picture emerges.

1. Globalization shifted high-pay work overseas to the benefit of capital, who reaped the profits from global wage arbitrage and to the detriment of workers in developed-nation economies.

The conventional-economic apologists glorified this as a net positive: everyone who lost their jobs to globalization would move up the food chain and get jobs as currency traders, highly paid tech workers, etc.

2. In reality, most were left with lower pay, precarious jobs as developed economies were producing ever larger cohorts of elites--college graduates and increasingly, those with advanced degrees--competing for those highly paid jobs.

Laid-off production-service workers could not compete with the growing army of credentialed elites for the remaining secure, highly paid jobs.

3. At the same time, the lower levels of the university-educated elites could no longer compete due to the overproduction of elites described by historian-author Peter Turchin as a key destabilizing dynamic in eras of social disorder. Two generations ago, a PhD was scarce enough to guarantee a secure job in academia, government or industry. Today, even a PhD from an elite university is little more than a ticket to enter the next round of cut-throat competition for the few tenure-track positions available.

4. This competition for the remaining secure, highly paid jobs was intensified by another change: the mass entry of women into the labor force in the 1970s led to the rise of households in which both spouses had well-compensated jobs in the upper reaches of the economy. These households had far more resources to pour into the advancement of their children, and a heightened awareness of the winner-take-all nature of elite competition.

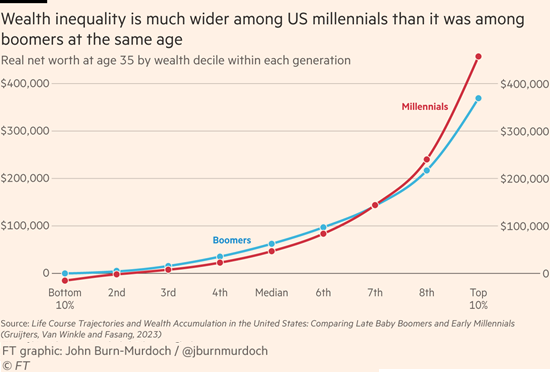

5. As this chart from a Financial Times article depicts, the net result is the Millennial generation is highly unequal in wealth and prospects. Two generations ago, about 20% of the workforce had a college diploma; that percentage has roughly doubled, even as the number of jobs that actually require a university education to do the job has declined. Those with the support of two professional parents entered the competition as early as kindergarten and continued apace into their mid-20s, leaving their less-prepared competitors in the dust.

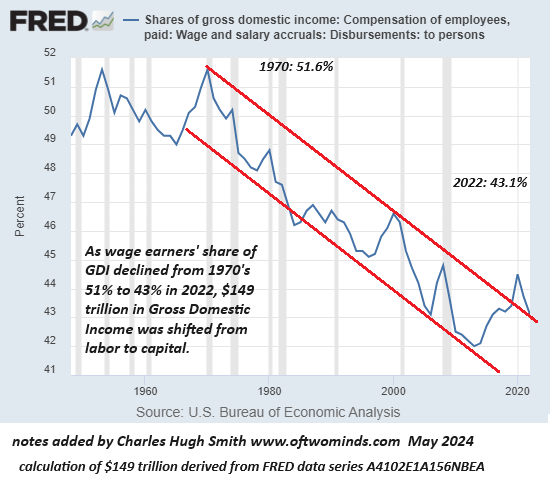

Meanwhile, labor's share of the economy's income has been declining for 50 years, leaving less income, fewer benefits and less security to divide among the workforce.

6. Concurrent with hyper-globalization, the hyper-financialization of the economy generated competition for productive assets and real-world assets such as housing. Workers in the low-pay, insecure reaches of the economy cannot compete with the wealthy elites (the top 10% own 90% of financial assets) for housing or other assets, while this credit-driven bubble has pushed prices higher, further reducing the purchasing power of wages.

Where one secure income was once enough to support a middle class household that owned the family home and sent the children to college, it now takes two secure incomes to support even the lowest rung of middle class expectations.

7. At the same time, society lost respect for essential work in favor of digital visibility. Validation, respect and being recognized for one's work are no longer available for those doing the work that keeps civilization functioning; recognition and admiration--and envy--are reserved for those with high visibility on social media or mass media.

8. This competition for visibility is not only cut-throat, it is artificial. Reserving recognition and respect for the few with high visibility in the world of screens has generated a great many perverse outcomes. Since mere mortals cannot possibly compete, every competitor must present an artificial self that is a pastiche of what's considered essential to gain media visibility: not just being attractive, but super-attractive, not just wealthy but super-wealthy, not just talented but super-talented, and so on.

Mere mortals are left in a hopeless situation. In response, they're withdrawing from the competition en masse. This abandonment of the competition is largely beneath the surface, as the apologists' happy-story narrative collapses once we recognize the hopelessness and the solution--withdrawal from the economy and society.

I'll have more to say on this in my next post.

New podcast: CHS on Leafbox (1:20 hrs)--authentic community, going grey, Doom Loops and more.

My recent books:

Disclosure: As an Amazon Associate I earn from qualifying purchases originated via links to Amazon products on this site.

Self-Reliance in the 21st Century print $18, (Kindle $8.95, audiobook $13.08 (96 pages, 2022) Read the first chapter for free (PDF)

The Asian Heroine Who Seduced Me (Novel) print $10.95, Kindle $6.95 Read an excerpt for free (PDF)

When You Can't Go On: Burnout, Reckoning and Renewal $18 print, $8.95 Kindle ebook; audiobook Read the first section for free (PDF)

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States (Kindle $9.95, print $24, audiobook) Read Chapter One for free (PDF).

A Hacker's Teleology: Sharing the Wealth of Our Shrinking Planet (Kindle $8.95, print $20, audiobook $17.46) Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $5, print $10, audiobook) Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake (Novel) $4.95 Kindle, $10.95 print); read the first chapters for free (PDF)

Money and Work Unchained $6.95 Kindle, $15 print) Read the first section for free

Become a $3/month patron of my work via patreon.com.

Subscribe to my Substack for free

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Gupatii ($70), for your splendidly generous subscription to this site -- I am greatly honored by your support and readership. |

Thank you, Mimi A. ($7/month), for your magnificently generous subscription to this site -- I am greatly honored by your support and readership. |

|

|

Thank you, Paulsat ($70), for your marvelously generous subscription to this site -- I am greatly honored by your support and readership. |

Thank you, Pete T. ($70), for your monstrously generous subscription to this site -- I am greatly honored by your support and readership. |