End of Work, End of Affluence I: Cascading Job Losses

Job losses in a typical recession are centered in interest-sensitive sectors like building and autos. This recession/depression will be different.

In a classic business-cycle recession, a period of reduced savings and excessive borrowing, consumption and expansion is followed by a period of retrenchment: reduced borrowing and production and an increase of savings.

This time around, we have an implosion of both highly leveraged debt--much of which flowed into the bedrock of middle-class wealth, residential housing-- and the real estate bubble it inflated.

Thus we have not just a typical business-cycle retrenchment but an implosion of the investment/money-center/mortgage banking sectors and a massive erosion of middle-class wealth via the decimation of housing and the financially-dependent stock market (401K pension/retirement funds, IRAs, stock options, etc.)

To make matters worse, two long-term trends have been eroding middle-income household wealth for decades:

1. The American wage-earner has been losing purchasing power for the past 30 years, a trend I have often covered here.

2. Technology, mechanization and globalization has drastically reduced the number of working-class jobs which pay middle-class wages.

Since auto manufacturing is in the news, we should recall the most salient fact about modern auto production is how few workers are required compared to the heyday of U.S. production in the 1950s and 1960s.

The Workplace: Can people take place of robots? No.

"Why bother with million-dollar robots when you have people who will work for $10 a day?

The answer, say GM executives and other industry analysts, is that low-cost labor is not a panacea, especially in a relatively high-technology industry like carmaking. For a variety of reasons, including safety, automation is necessary even in countries where an army of low-paid workers is readily available.

There is a widely held perception in Europe and the United States that Asian countries progressively will win all manufacturing jobs because workers are prepared to toil for so little. But while companies in many industries have moved their operations to Asia, the complex equation of timeliness, quality control and cost in the auto industry dictates that car production is not as easily outsourced as sewing a shirt or a pair of pants.

Significantly, labor is a small fraction of the total cost of producing a car in rich and poor countries.

Deciding on the level of automation in these far-flung manufacturing plants depends on several factors, but the main consideration is volume: robots work much faster, more efficiently and with less risk of accident than humans in certain jobs, and they can make sure there are no bottlenecks in the process.

Yamamoto cites a more intriguing reason carmakers choose automation. Newly built Japanese factories in China use robots intensively despite relatively low labor costs, he said.

"The workers don't have much experience," Yamamoto said. "Instead of educating them, they prefer to use more robots."

In other words, regardless of the cost of wages, robots dominate auto manufacturing for many reasons. Nothing will change this reality.

One industry has dominated corporate profits for years: banking. It is now crippled, broken, reduced, never to rise to bubble heights in our lifetimes. Without 30-to-1 leverage and exotic/toxic derivatives to sell, investment banking's ability to generate profits is broken. With transactions down, even staid mortgage banking's ability to reap stupendous profits has fallen.

Housing is the bedrock not just of middle-class wealth but of local tax revenues. Government at all levels has relied on these two bubble sectors for tax revenues: capital gains taxes from all those "flippers" and bankers' stock sales, transaction taxes for real estate sales, and property taxes based on rapidly rising real estate valuations. All of these sources are either broken or deeply impaired.

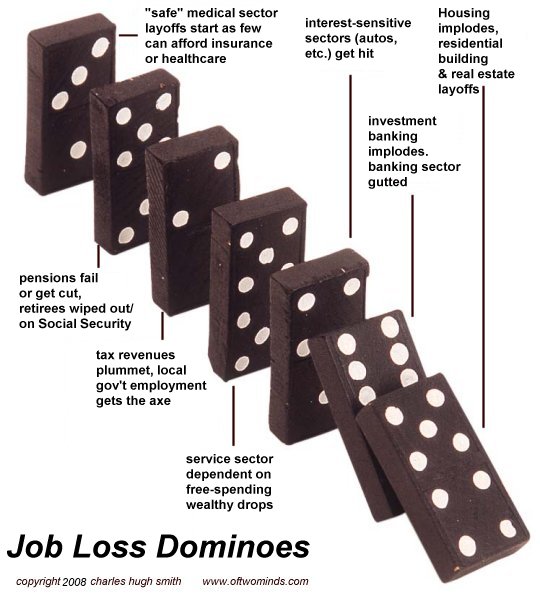

As a result, we face a cascade of job losses which can be likened to falling dominoes:

One way to conceptualize these cascading job losses is to distinguish the varying waves which are battering the U.S. economy. If you swim or surf in the open ocean, you know that waves tend to come in sets, which is just another way of saying various forces create waves of varying wave-lengths. Long wave-length waves will roll in from the open ocean, interacting with local forces such as wind, seabeds and currents to create a variety of waves, some in sets and occasionally, a freakishly massive rogue wave.

Let's list the forces at work, each one of which generates a job-loss wave of varying length and influence:

1. Housing implosion: jobs in real estate, lending and real estate were the first to go after the housing bubble burst in 2006. But the layoffs haven't ended; surviving homebuilders are still trimming staff, realtors are finally giving up and leaving the industry, etc.

2. Investment/money-center/mortgage banking implosion. When firms go bankrupt, the layoffs are immediate. But that doesn't mean the layoffs are finished; they're just getting started as consolidation, further declines in revenues, etc. force survivors to trim staff at every level of the remaining business.

The one growth sector in the industry is the "clean-up crew": foreclosure/short-sales staff, FDIC regulators, auditors, bankruptcy attorneys, etc.

3. The free-spending bankers, realtors, house flippers, etc. supported an entire ecology of jobs dependent solely on their largesse: dog walkers, maids, high-end restaurants, boutiques, antique dealers, personal trainers, private-jet pilots, etc. etc.

Correspondent Richard Metzger recommended this Vanity Fair piece on the meltdown's adverse consequences for both the absurdly wealthy players in the high-finance realm and all those who depended on them for their livelihoods: Profiles in Panic.

So those jobs are vanishing as as fast as the wealth itself. Restaurant revenues here in the San Francisco Bay Area are already off 10%-40%, and the real declines have yet to begin. Why?

4. Every domino that falls takes down another layer of retail, services and restaurants; the housing meltdown took down furniture sales, which then take down everyone who sold anything to those employees and store owners. As neighborhood restaurants fold, their workers spend less in the neighborhood, too.

The depth and reach of the job losses will be fearsome for the reason that the losses are coming in the very bedrock layers of our economy: middle-class wealth, the vast majority of which is housing or stock holdings in retirement funds, and the banking sector,which generated much of the profit in the entire stock market Bull run, and all of its financing and leverage.

You break lending/risk/leverage and housing, and you've broken the keel of the entire U.S. economy.

5. Local and state government revenues are generally dependent on property taxes and transaction-generated wealth: capital gains paid when stock or real estate is sold, and direct transaction fees paid when properties are developed, built or sold.

As risk aversion cripples lending and leverage, transactions dry up, and as bubbles deflate, profits are replaced which stupendous losses which don't generate tax revenues.

Here too waves of various lengths are rolling in. Capital gains taxes are the first to decline to near-zero, followed by transaction fees, building permits, etc. As jobs are lost and sales decline, sales taxes plummet, followed by a large drop in income taxes. Finally, as declines in real estate values filter down to county tax appraisals, property tax revenue will start falling.

Foreclosures and abandoned properties muddy the property tax collection process, too; if the owner and lender both disappear, then who pays the back taxes? What happens when properties fall 50% or more? The lag time between the fall of housing values and the decline in property tax revenue may be months or even years, suggesting that government tax revenues could continue declining for years.

6. Other spending sources are longer term, but they too will eventually be depleted. Local government municipal bonds are a good example; billions of dollars in infrastructure bonds are approved by voters and subsequently spent over time on roads, schools, libraries, parks, etc.

With the credit markets dried up or frozen, municipal bonds are no longer an easy sell; so as old bond money is spent, few new bonds are being approved or sold to replenish the local coffers of money to be spent on infrastructure projects. Once the bond financing is gone, so are the jobs they supported.

This is why job losses can continue mounting even years after the initial layoffs began.

7. Pension plans are under-funded; some will fail while others will be trimmed. The bottom line is promises that were made in flush times cannot be kept in the Coming Depression, and so many retirees will have to get by with less income than they expected. Sadly, stories already abound of retirees losing both their homes and their 401K retirement nesteggs, and these pension failures/cutbacks/losses will squeeze spending, triggering ever more losses in retailers, restaurants, nail salons, etc.

8. By some accounts, all job growth in the 2001-2008 period came from government and healthcare. If we consider Medicare and Medicaid, that is basically the same thing.

While Medicare will remain a "sure thing" for a few more years, the rest of the bloated, insanely expensive/irrational "healthcare" system will start getting squeezed. As millions lose their jobs, they also lose whatever health insurance they had; all private and non-profit health providers will start finding less money flowing through the system.

Recently, Kaiser Permanente Healthcare, one of the largest non-profit healthcare providers in the nation (I am a member, as long as I can afford the outrageous insurance fees for the self-employed), reported a $300+ million loss--and this was well before the real meltdown in the economy even started.

The bastion of healthcare has yet to crumble, but the waves that will crash through its defenses are on the horizon and drawing ever nearer.

All the waves are self-reinforcing/accumulative. The laid-off worker has no health insurance, so the insurer loses income and has to lay off workers, who then have no income to spend on retail, nail salons, movies, eating out, etc. Since the waves are rolling in at various velocities and with varying destructiveness, the job losses will be coming for years, not months; some months, a trickle, other months, a flood, but always more, for a long time to come.

CHS NOTES: New link in the blog-roll: Jesse's Cafe Americain, a site of consistently unique insights into markets, currencies, policies and much more. Hats off, ladies and gentlemen, to Jesse.

This weeks' topics may strike some as gloomy--Last Christmas in America, anyone?--but reality trumps fantasy every time... and next week I promise some coverage of ways to counter/survive the Coming Depression.

Anyone insane enough (I was accused of being high on LSD, among other things, for posting this) to heed my Dec. 1, 2008 call for a huge stock market rally is about to be richly rewarded--just you watch....

My apologies for falling behind in email; I just finished a 93,000 word novel entitled Bidding for Love, a romantic comedy set is San Francisco, which required a large number of 12-16 hour days...(about 200, though I don't really count; it's all in good fun).

Thank you, readers, for your contributions of cold, hard cash these past few months; there is no encouragement like cash, and I thank you most sincerely for your boundless generosity. I will endeavor to provide value, though it is a hit-or-miss affair as you know from past performance....

And here is Part II of Chris Sullins' strategic action thriller, Operation SERF:

Operation SERF, Part II(Chris Sullins, December 6, 2008)

It was a half hour after dawn and the early morning light provided enough illumination to the living room via the large broken picture window and open doorway to Eduard Morgan’s home. Mark had regretted allowing his aunt Maria to come back to the home with him to check things out. She was now knees down on the carpet next to Eduard’s body sobbing with her face buried in her hands.

Operation SERF, Part I

Readers' commentaries 12/2/08--check it out!

Holiday gift announcement: maximum two signed books per customer: Signed copies of Claire's Great Adventure (perfect for that impossible teen on your "gotta get them something, arggh" list) are limited to two per customer: $12 for one (includes $2.58 postage), $22 for two.

The regular price on amazon.com is $16.99; the $12 (incl. shipping/postage) is a special offer I am making to readers. Please send $12 via check (email me for an address) or via my Paypal account with instructions on how to inscribe the book, and I will mail the book(s) directly to you. If you'd like to read other readers' reviews before buying a copy, the cover image below links to the amazon.com page and two readers' reviews. Read the first chapter.

Book Notes: My "little book of big ideas," Weblogs & New Media: Marketing in Crisis is now available on amazon.com for $10.99.

"Charles Hugh Smith's Weblogs & New Media: Marketing in Crisis is one of the most important business analyses I have ever read. It is the first to squarely face converging global crises from a business perspective: peak oil, climate change, resource depletion, and the junction of key social cycles will radically alter the business landscape in coming decades...."

Thank you, Julie M. ($25) for your very much-appreciated generous donation to this site via check/mail. I am greatly honored by your support and readership.

Thank you, Guy T. ($40) for your second exceedingly generous contribution to this site. (May I send you a book as a token of my appreciation?) I am greatly honored by your support and readership.

charles hugh smith

Investing In Revolution

Ultra-Processed Life

The Mythology of Progress

Self-Reliance in the 21st Century

Burnout: Reckoning and Renewal

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States

A Hacker's Teleology

Will You Be Richer or Poorer?

Pathfinding our Destiny

The Consulting Philosopher

Money and Work Unchained

Inequality and the Collapse of Privilege

Why Our Status Quo Failed and Is Beyond Reform

A Radically Beneficial World

Get a Job, Build a Real Career and Defy a Bewildering Economy

The Nearly Free University

Resistance, Revolution, Liberation

Investing in troubled times

Survival +

Add Of Two Minds to your reader:

CHS

Weekly Musings Reports

Subscribers ($5/mo) receive weekly Musings Reports. At readers' request, there is also a $10/month subscription option.

What subscribers are saying about the Musings (read samples):

"What makes you a channel worth paying for? It's actually pretty simple - you possess a clarity of thought that most of us can only dream of, and a perspective that allows you to focus on the truth with laser-like precision." Jim S.

The "unsubscribe" link is for when you find the usual drivel here insufferable.

2005

2010

2015

2020

2025