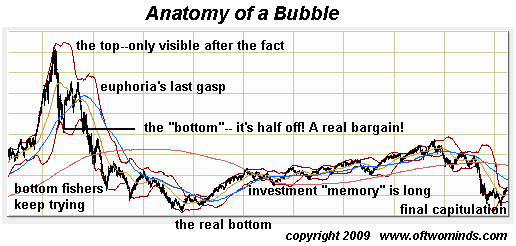

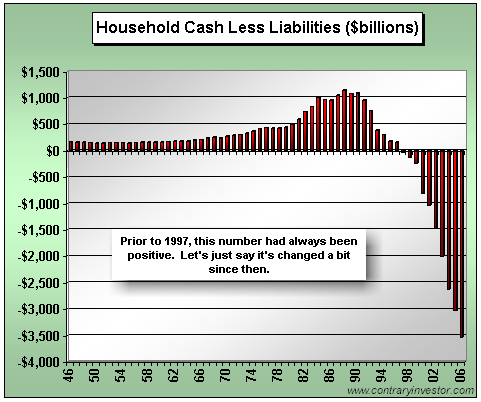

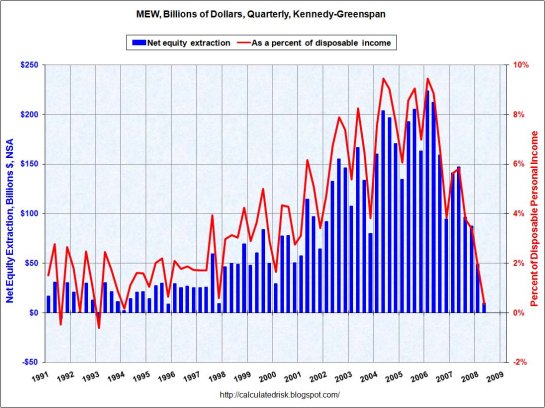

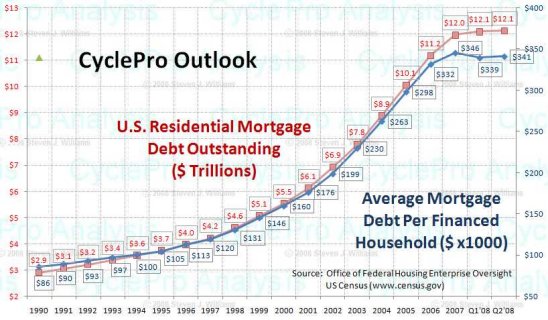

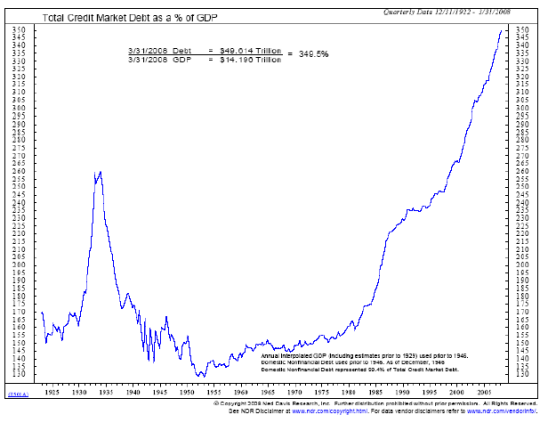

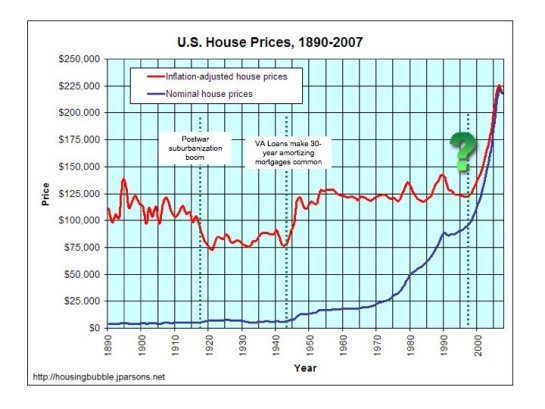

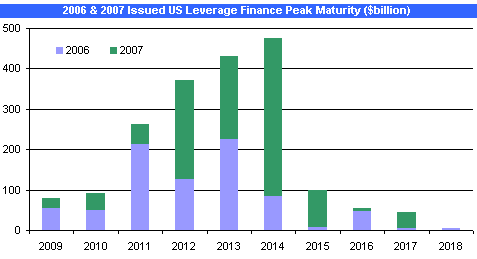

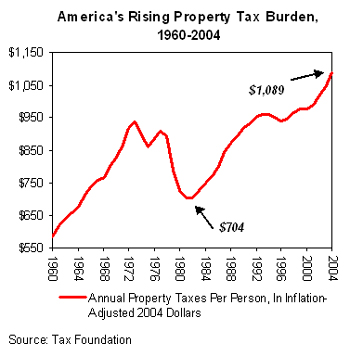

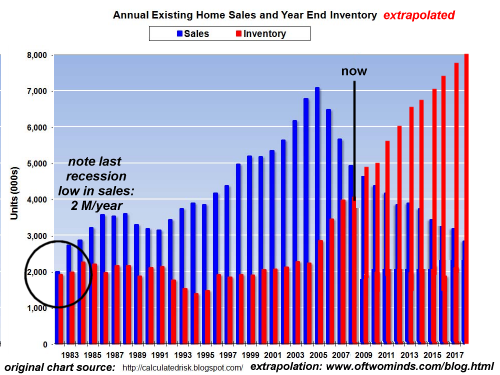

Why a 50% Drop in Housing Is Not the Bottom I recently saw a few minutes of a Nightly Business Report program on PBS in which a Florida broker was observing that homes which once commanded $350,000 at the bubble top were selling briskly now at $169,000 to investors from every part of the globe. In other words: "These homes are half off! They're screaming bargains! They can't get any cheaper than this!" The psychology behind this euphoria is accessible to us all. It's easy to forget where housing prices were before the bubble and focus instead on how much they've dropped from the bubble peak. The same is true in any bubble, be it collectables, real estate, stocks, or tulip bulbs. But valuation realities have no relation to bubble top pricing. Thus we should ground our analysis of housing valuations and what constitutes a "bottom" in metrics other than "it's 50% off it's top price." Let's start by considering just how high the bubble took housing valuations: This chart reveals that housing in California more than tripled at the bubble top. A fall of 50% from that peak (i.e. $275,000) is still 60% above the starting point. Let's consider a model of all bubbles, regardless of the asset or the era: No model can predict the timing, highs or lows of any bubble, but bubbles tend to follow a pattern traced in human psychology: 1. As euphoria grabs hold, prices rise in a steep ascent to a point at which "everyone" believes there is no end to the trend. 2. The initial descent from the bubble peak is a "shock" which leaves the bubble mentality intact, i.e. the Bull Market in tulip bulbs, real estate, tech stocks, etc. is only suffering a standard retracement/indigestion; the trend higher is still in place. 3. In housing, this psychology is embedded in such chestnuts as "they're not making any more land," "real estate always rises over time," "population growth means demand for housing will always rise," "the house is the foundation of middle class wealth appreciation," and so on. 4. At some point speculators who were left out of the initial explosive rise jump in because "prices are a real bargain now." 5. This buying pushes demand above supply briefly, and prices start rising again. 6. But the realities beneath price action have changed, and this bargain-hunting burst soon fades as demand falters, supply rises and prices renew their descent. 7. Speculators and investors' memory of the tremendous profits made on the way up remain firmly embedded, forming an "investment memory" which locks them into the view that the upward trend will resume at some point. This drives wave after wave of bottom fishing in which speculators buy into an apparent bottom only to be disappointed/ wiped out by a renewal of the downtrend. 8. At some point, all the bottom fishers have expended their capital and prices retrace to the pre-bubble levels, or even lower. This is what can be called "the real bottom." 9. But the memory of past glories still remains in the minds of speculators/investors, and so a subdued uptrend starts as "hope springs eternal" buying kicks in. 10. Eventually this institutional/cultural "memory of an uptrend" fades as the "recovery" in prices fails. The truisms which fed the brief bubble and long post-bubble decline and recovery--that tech stocks were the future, real estate only goes up, the South Seas is the epic investment of all time, etc. are repudiated and lose favor. This is the ultimate bottom. Can a 10-year bubble reach this "ultimate bottom" in a mere two years? History suggests not. Then there's the preponderance of other evidence that the underpinnings of the housing bubble have irrevocably shifted. Let's review some charts: Household balance sheets are in terrible shape: This chart only reflects the extreme reached in 2006; it's undoubtedly even worse now. Personal savings rates have risen recently, but Americans will need to start saving roughly a trillion dollars a year to return to historic savings rates:and that means not borrowing a spending a trillion but withdrawing it from consuming. Meanwhile, the equity extraction game is over, and the stands are littered with broken dreams and busted bets: Mortgage debt has tripled from $4.2 trillion in 1997 to over $12 trillion: This explosion of debt is economy-wide, and is not limited to residential housing: How an economy foundering beneath stupendous debt can forcefeed housing prices higher via ever greater debt is unknown. Just as a refresher on the extremes the housing bubble reached even when adjusted for inflation: A significant percentage of this debt comes due in the years just ahead: Another standard measure of valuation, the price-to-rent ratio, also reached historic highs. In some areas of the nation, this might have already returned to the mean, but with property taxes skyhigh and the cost of renting dropping, it may well be the cost of renting is still significantly cheaper than owning. While this graph is a few years old, the trend to historic highs in property taxes is clearly illustrated. Yes, you can petition your county to lower your appraisal, but unless your state is protected from fast-rising property taxes via a Prop 13-type law, then brace yourself for local governments to make up their declinign tax revenues on the backs of property owners--plummeting prices be darned. With reports of banks holding some 600,000 foreclosed or distressed properties on their books and off the market in the news, it is a foregone conclusion that any blip up in demand for homes will be met with a tide of new supply. After the current "bargain buying" dries up, inventory will exceed demand and prices will resume their fall. And last but not least, let's note that we're dealing not just with the aftermath of one historically extreme bubble, but three: one in stocks(shown here), one in housing (shown above) and another in bonds which have skyrocketed as yields drop to near-zero. The net result of declining asset values across all asset classes but gold is that there will be a global reduction in borrowing against assets. So add up the financial contexts which control real estate valuations: 1. Extreme bubble valuations must eventually retrace to the starting point, and in many cases they drop below the starting point. 2. Housing and real estate are based on the availability of cheap, plentiful debt. As economy-wide debt loads are at historic extremes, it is prudent to ask what conditions will enable trillions more in debt to be issued to buy inflated housing. 3. As the Federal government borrows trillions of dollars on the open market to fund its mega-stimulus-bailout debts (in the trillions and counting), then the government is competing with private borrowers for a dwindling pool of capital/savings. That will drive up rates, making mortgages more expensive. And since prices drop as rates rise, this global push on interest rates is a profound headwind for housing prices globally. 4. Paying a mortgage requires steady income, which for most citizens means a steady job. Rapidly rising unemployment reduces the pool of potential buyers and adds to the inventory as those losing their incomes also lose their homes. In short: with the national and household balance sheets at historic extremes of indebtedness it is difficult to see what fundamental financial foundation exists for higher housing prices. The only conclusion to be drawn from the above charts is that those currently buying "at bargain prices" will very likely be disappointed as prices renew their downtrend in the near future. Thank you to everyone who emailed me in the past two weeks. I will try to respond to everyone over the next week. Your patience and understanding are greatly appreciated. Thank you, Alexis H. ($10), for your very generous contribution to this site. I am greatly honored by your support and readership.

April 16, 2009

The psychology behind the idea that a 50% reduction in bubble-era housing prices constitutes a "bargain" is flawed for a number of reasons. (NOTE: to view charts in full, please go to my main blog page at http://www.oftwominds.com/blog.html .)

charles hugh smith

Self-Reliance in the 21st Century

Burnout: Reckoning and Renewal

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States

A Hacker's Teleology

Will You Be Richer or Poorer?

Pathfinding our Destiny

The Consulting Philosopher

Money and Work Unchained

Inequality and the Collapse of Privilege

Un Mundo Radicalmente Prospero

Why Our Status Quo Failed and Is Beyond Reform

A Radically Beneficial World

Get a Job, Build a Real Career and Defy a Bewildering Economy

The Nearly Free University

Resistance, Revolution, Liberation

Investing in troubled times

Survival +

Four Bidding For Love

Books & eBooks

As an Amazon Associate I earn from qualifying purchases.

Our Kindle ebooks:

Self-Reliance in the 21st Century

Our Kindle ebooks:

Self-Reliance in the 21st Century

When You Can't Go On: Burnout, Reckoning and Renewal

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States

A Hacker's Teleology: Sharing the Wealth of Our Shrinking Planet

Will You Be Richer or Poorer? Profit, Power and A.I. in a Traumatized World ($6.95)

Pathfinding our Destiny ($6.95)

Money and Work Unchained ($6.95)

Inequality and the Collapse of Privilege ($3.95)

Spanish edition: Un Mundo Radicalmente Prospero ($9.95)

Why Our Status Quo Failed and Is Beyond Reform ($3.95)

A Radically Beneficial World: Automation, Technology and Creating Jobs for All ($6.95)

Get a Job, Build a Real Career and Defy a Bewildering Economy ($6.95)

The Nearly Free University and The Emerging Economy ($6.95)

Resistance, Revolution, Liberation ($6.95)

An Unconventional Guide to Investing in Troubled Times ($6.95) Survival+: Structuring Prosperity for Yourself and the Nation ($9.95)Survival+ The Primer ($3.95)

Weblogs & New Media: Marketing in Crisis ($3.95)

The Adventures of the Consulting Philosopher ($1.29)

Four Bidding For Love ($1.29)

Claire's Great Adventure ($1.29)

Verona in Spring ($1.29)

For My Daughter ($1.29)

I-State Lines ($9.95)

When You Can't Go On: Burnout, Reckoning and Renewal

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States

A Hacker’s Teleology: Sharing the Wealth of Our Shrinking Planet

Will You Be Richer or Poorer?: Profit, Power and A.I. in a Traumatized World ($12.95)

Pathfinding our Destiny: Preventing the Final Fall of Our Democratic Republic ($12.95)

Money and Work Unchained ($15)

Inequality and the Collapse of Privilege ($8.95)

Why Our Status Quo Failed and Is Beyond Reform ($8.95)

A Radically Beneficial World: Automation, Technology and Creating Jobs for All ($15)

Get a Job, Build a Real Career and Defy a Bewildering Economy ($15)

The Nearly Free University and the Emerging Economy ($15)

Resistance, Revolution, Liberation: A Model for Positive Change

($15)

An Unconventional Guide to Investing in Troubled Times ($15)

Survival+ (US)

$19.95 Structuring prosperity

Survival+ The Primer $8.95

Weblogs & New Media: Marketing in Crisis

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the U.S.

A Hacker's Teleology: Sharing the Wealth of Our Shrinking Planet ($17.46)

Will You Be Richer or Poorer? Profit, Power, and AI in a Traumatized World

Pathfinding our Destiny: Preventing the Final Fall of Our Democratic Republic

Inequality and the Collapse of Privilege

Why Our Status Quo Failed and Is Beyond Reform

A Radically Beneficial World: Automation, Technology and Creating Jobs for All

Get a Job, Build a Real Career and Defy a Bewildering Economy

Four Bidding For Love ($16.99)

romantic screwball comedy

Claire's Great Adventure

$16.99 2 stowaway girls + pirates

Kama Sutra Cadillac

Of Two Minds

Verona in Spring

$13.99 29-year old Verona is in a romantic tangle

For My Daughter

$12.99 Iraq vet, Burma, saving dolphins and his marriage

I-State Lines

Download the free Kindle reader for any device: Windows or Mac OS, iPads, iPhones and Android.

Kindle for PC

Kindle for Mac

Kindle for iPhone

Kindle for iPad

Kindle for Android

give a Kindle ebook as a gift

Our print books:

Self-Reliance in the 21st Century

$8.95 Leverage the Web

Audiobooks

When You Can't Go On: Burnout, Reckoning and Renewal

NOVELS

The Adventures of the Consulting Philosopher: ($8.95)

$12.99 sex + zaniness

$13.99 ESP, espionage + twists

($20) Alex & Daz on the road

Click here for sample chapters of all novels

Add Of Two Minds to your reader:

CHS

Weekly Musings Reports

Subscribers ($5/mo) receive weekly Musings Reports. At readers' request, there is also a $10/month subscription option.

What subscribers are saying about the Musings (read samples):

"What makes you a channel worth paying for? It's actually pretty simple - you possess a clarity of thought that most of us can only dream of, and a perspective that allows you to focus on the truth with laser-like precision." Jim S.

The "unsubscribe" link is for when you find the usual drivel here insufferable.

2010

2015

2020