Homeownership and Wealth Accumulation/Destruction

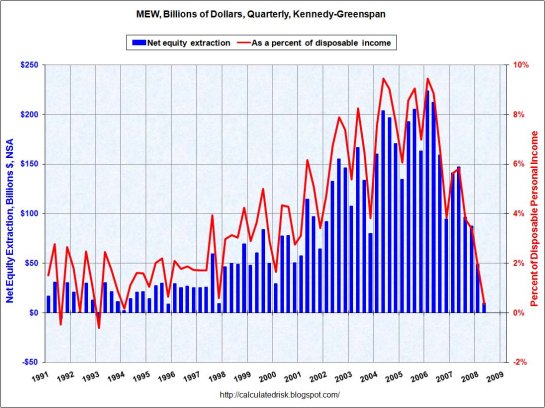

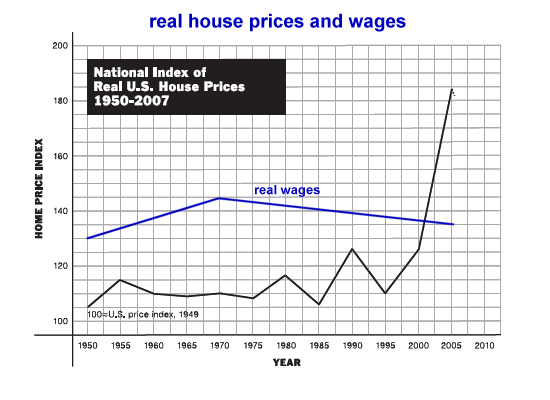

May 5, 2009 Once upon a time people spent decades paying off their home mortgages.That reduction in debt to zero left them equity. Those who paid rent for 30 years may have had lower costs of living (no maintenance costs or property taxes) but unless they saved religiously then they did not end up with the equivalent wealth of a typical homeowner who paid off the mortgage. Throughout the 1950s and 60s, homes prices and mortgage rates were remarkably stable. The idea that one's house could double in value in a few years was as nonsensical as the price falling in half. Houses cost about two or three times' average income, and over time they drifted higher (adjusted for the era's low inflation) at about 1% a year. As a result, speculation was nonexistent. Some enterprising handyperson might buy a rundown house for say $22,000, invest some money and sweat equity, and then be delighted to sell it for $25,000 some time later. The key to housing being the foundation of middle class wealth was not the rise in value--it was the reduction of debt to zero. Removing equity from one's home was unheard of--there were no HELOCs (home equity lines of credit) and second mortgages were modest; people took a second mortgage out to pay for major home improvements or a new roof, not for vacations, new cars, college, etc. Needless to say, the entire concept of "homes as the foundation of middle class wealth" has been radically modifed--and perhaps refuted. What was once rare--aging homeowners nearing retirement still holding large mortgages and modest equity--is now commonplace. The inconceivable has happened to homeowners in locales such as Detroit: paying off the mortgage did not build wealth, as the value of the home diminished to near-zero. In left and right coast locales, the inconceivable also happened: simple bungalows tripled in value in less than a decade, creating leveraged wealth far beyond any historical precedent. Under the influence of sharply rising inflation and the massive Baby Boom generation entering its prime homebuying years, housing shot up in the late 70s. This rapid rise in value was repeated in the late 80s as well, further priming the expectation that housing had changed from a rising-at-1%-per-year asset of slowly accumulated equity to a speculative vehicle in which a 20% down payment could be leveraged into 100% or even 200% gains in a few years. This changing character of "housing as wealth accumulation" thus set the psychological stage for the Great Housing Bubble of the 2000s, in which even the 20% down payment vanished and leverage approached infinity as "no down payment, no document verification" loans flourished. The "rational" response to low interest rates, easy credit and wildly climbing housing prices was to increase one's debt to the maximum and throw it all into real estate speculation. Thus we saw low-income households buying one or two McMansions to flip for quick profits, speculators putting a few thousand down on homes which had yet to be built and then selling the right to the house for stunning profits, and so on: a full speculative mania. This change in the nature of wealth accumulation from home ownership was profound. With interest rates low and real estate skyrocketing in value, paying down one's mortgage was considered backward and foolish; the rewarding strategy was to extract all of the new equity and use it for fun or further speculation in real estate (or collectibles, cars, stocks, etc.) But once housing prices began falling to earth, the perverse consequences of leveraged debt became evident. With home equity largely extracted during the boom years via refinancing and HELOCs, the remaining equity sitting atop a mountain of mortgage debt quickly shrank as prices fell. Despite the usual lies and legerdemain of the Federal Reserve, it now seems that home equity of those 50 million households with mortgages (25 million households own their homes free and clear) has shrunk to a decidely non-wealth-building 15%. As noted in a recent UP AND DOWN WALL STREET (Barrons): That the housing bubble was a one-off anomaly created by demographics, super-cheap money freely lent without regard to risk or prudence is now obvious. What is less obvious is a prime motivator behind the middle class fever to speculate in real estate: Real income (adjusted for inflation) has been falling for decades. Though masked by inflation and periodic (and temporary) increases in wealth from various bubbles in stocks and real estate, the reality is that the vast middle class has actually been losing ground since the early 1970s. Consider the consequences of this chart: In effect, the double-income high-earning households added enough income to bid up desirable real estate to absurd heights, as the lower income households were left to "catch up" via reckless speculation in housing. Which is not to say the top-income households didn't speculate just as recklessly; as delinquency rates for jumbo mortgages rise, the impact of a declining economy and deflating housing bubble is being felt even by higher-income households. What I think is poorly understood is the appeal of speculation as one's income and wealth fall in terms of purchasing power. When measured in purchasing power, the average income household has lost ground since the late 60s/early 70s: From this perspective, the speculative mania in housing was fundamentally a tragic last-gasp effort to make up lost ground via speculation in housing--an extension of "housing is the foundation of middle class wealth." But as housing bubble valuations slowly recede to historic means, this entire premise is being invalidated. Paying off a $300,000 mortgage on a house which is worth $200,000 is not the road to wealth; it is a slow and painful road to penury. If a buyer overpaid for the property, then paying off the mortage will still eventually result in the accumulation of equity via the reduction of debt to zero (assuming the value of the property does not also fall to zero). But as over-leveraged Baby Boomers are learning, the combination of huge mortgages which will never be paid off and declining housing prices is not a formula for accumulating wealth. It is a formula for a Capital Trap in which one's income drains away in debt repayment with little to show for the "investment." Housing Bulls are positive "the bottom is in" and a rising population, newly "fixed" banking sector and restored consumer confidence will soon lead to a restoration of bubble-era valuations. But if the Great Housing Bubble was a one-off anomaly which will never come round again, then the entire premise of "home ownership as the foundation of middle class wealth" is now suspect. Steve T. (re: the stock market's melt-up) Riley T. Everyone understood financial leverage up, when I would ask about leverage down, the answer would be "what's that?" John B. You danced around the issue and even kind of mentioned it a couple of times but really never got to the heart of the matter in my opinion. All the automakers and most other US companies made a similar error in the 60's or early 70's sometime. We shifted from engineering to marketing. Engineering requires long term thinking and marketing requires short term thinking. Part of marketing is financing. Good engineering is coming up with a good design to begin with and work with it over the years to steadily improve it by reinvesting in it. Instead we come up with a good design and take the capital it throughs off to put into some other venture. Even though you are critical of European cars, I would say look at the basic model of the 911 Porsche which the body style really goes back to the 356 B. Very little external changes but continuing refinement. In addition, very little marketing. One of the problems with Mercedes is they shifted to the American model. I have a 1983 Porsche which I have had since 1984 (one year old). Some minor things have been done to it but the same transmission and the same engine. Some of the strap on items have been replaced (like the air conditioning compressor after 20 years or so). Noted the Honda is far less over all cost, but the 911 still has one antribute, I can sell it for more than I paid for it! The funny thing about long term thinking is after a few years with continual focus on it, the quarterly profits just roll in quarter after quarter. While on the short term thinking each quarter is a struggle. I have been at both types of companies even though the first one is much harder to find anymore. I believe this marketing thinking (otherwise known as snake oil salesmen) permeates everything in America and is probably our number one problem. We have become the most dishonest group of people to walk this world. Thank you, readers, for these comments. The End of Overeating: Taking Control of the Insatiable American Appetite Dark Age Ahead Jane Jacob Coercion Douglas Ruskoff The Limits to Capital, New Edition (an explication of Marx's Capital) Sustainable Energy - Without the Hot Air I Will Bear Witness 1942-1945: A Diary of the Nazi Years The Predator State: How Conservatives Abandoned the Free Market and Why Liberals Should Too The Predators' Ball: The Inside Story of Drexel Burnham and the Rise of the Junk Bond Raiders The Printing Press as an Agent of Change (Volumes 1 and 2 in One) Thank you, Peter C. ($5), for your most-welcome generous contribution to this site. I am greatly honored by your support and readership.

The nature of "homeownership is the foundation of middle class wealth" has changed from accumulating wealth by paying off a mortgage to speculating in housing by taking on more debt.

As to the Fed's claim that the equity of homeowners as a group stands at 43%, she points out that what the Fed neglects to tell you is that roughly a third of them have their houses free and clear. Lo and behold, some basic arithmetic reveals that 67% of homeowners with mortgages have equity of less than 15%. That, Stephanie comments drily, suggests the "destruction priced into the credit markets hardly seems out of whack with potential reality."

I Received several incisive emails recently:The house of cards is driving concrete pilings into the ground, but the ground is still only quicksand.

In 30 plus years of designing financial systems a huge amount of money and effort was put in to make sure the system would "scale up" not a word was every said about "scale down".

I read your article on the automakers and here is my thought for a long time.

Looking for something new to read? Scan these recent additions to our "recommended" list: (Many recommended by other readers) Elizabeth Eisenstein

Our previous list of hot reading (check them out at your local library if you don't want to own a copy) can be found at Books and Films