Deflation or Inflation: Who Cares?

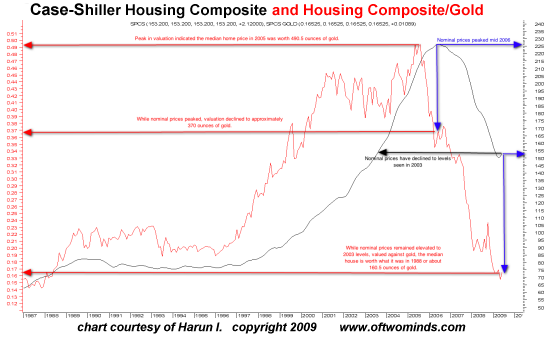

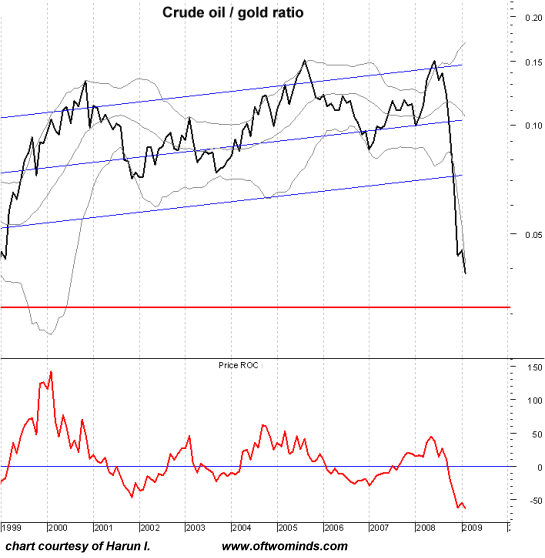

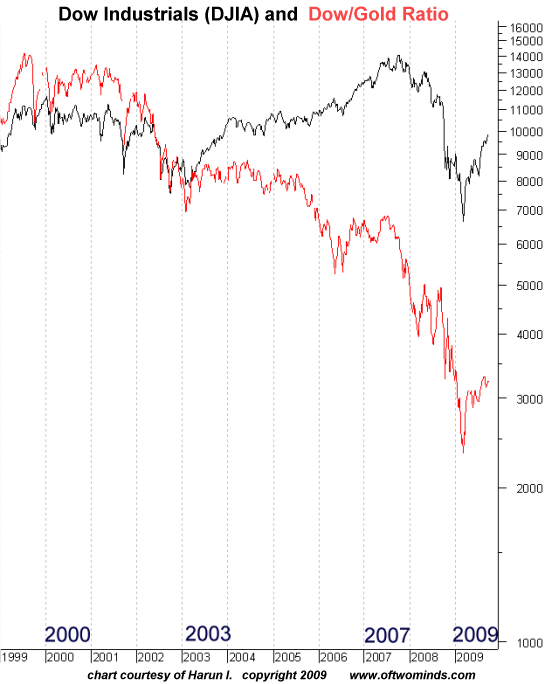

Posed as the great debate of the era, maybe the deflation-inflation debate offers little practical value to investors. Though they might disagree on what lies ahead, most financial pundits will agree on one thing: to make money in the next decade, you have to "get it right" on the deflation or inflation question. From at least one point of view, the debate is a red herring and a distraction. For supposedly being the global answer to investment decisions, the answer (whichever one you select) offers precious little guidance when it comes to actually making investment decisions. Will $100 buy more loaves of bread (i.e. wheat futures contracts) next year, or fewer loaves? The answer is supposed to be simple: in deflation, more loaves (cash rises in value); in inflation, fewer loaves (commodities rise faster than wages). But in the real world, drought could send the price of wheat skyrocketing even in a deflationary setting. A huge surplus could send prices down even in inflationary times. As often noted here, supply and demand still matter, regardless of the inflationary and deflationary pressures on the macro level. Consider oil--the essential industrial commodity. Cash could be gaining in purchasing power as deflationary forces weigh on commodity prices, but a sudden squeezing of supply (closing the Strait of Hormuz, for instance) could easily outstrip modest deflation with a sudden doubling or tripling of oil prices in all currencies. Alternatively, massive oversupply would outweigh modest inflationary pressure on oil prices. As noted here many times, purchasing power offers a more reliable real-world guide to wealth and income than any deflation-inflation metric such as "inflation-adjusted dollars." Even gold may rise or fall in response to factors beyond purely monetary deflation or inflation. Thus we can conclude: there are no simple global investment answers, there are only series of relative performance pairings. In other words, to assess if wheat is at an extreme valuation in dollars, we might view wheat priced in gold and wheat priced in euros. Is real estate "cheap"? Pairing real estate to dollars doesn't give us much insight; if the dollar is plummeting, then any modest increase in housing would be more than offset by the decline in purchasing power of the dollar. As discussed in When Housing Is Priced in Gold (September 23, 2009), a more insightful view can be reached by examining the housing index/gold ratio. Here are contributor Harun I.'s explanatory notes and chart: Click on chart for a full-sized version in a new browser window. At the peak in 2005, the median home price equaled 490 ounces of gold. The present median price is worth about 160 ounces of gold, or roughly the same valuation as 1988. Nominal housing prices have returned to 2003 levels. But when priced in gold, the 2003 valuation was 420 ounces of gold. Now that nominal prices have returned to that level today, the median house will only fetch 160 ounces of gold. Consider another example: the gold/oil pairing. Once again courtesy of contributor Harun I., here is a chart of the oil/gold ratio. This was charted in February 2009, and you can see that as oil slipped in price and gold rose, the ratio plumbed historic lows, suggesting oil was a buy in the high $30s. Is the Dow Jones Industrial Average gaining in value? Let's look at the Dow/gold ratio. The Dow/gold ratio topped out in late 1999. When priced in gold, the current rally looks modest indeed. What I hope to illustrate in these examples is the idea that deflation or inflation are only two of many influences on relative performance and purchasing power. Certainly inflation influences purchasing power when it reaches hyper-inflationary levels, but credit-based economies don't go hyper-inflationary--that catastrophe is reserved for currency-based economies. As for deflation: if impaired debt totals $20 trillion, and the Fed creates $2 trillion, then the decline in the value of the debt will quickly overwhelm the inflationary forces of money creation. But regardless of deflationary pressures as credit contracts, purchasing power rises or falls in response to supply and demand and various other forces. The correct investing analogy to my mind is to catch the bus at extreme lows in relative valuation, ride it to increased purchasing power priced in real goods, then step off and catch the next "extreme valuation" bus, either on the short or long side. Harun's chart of housing and gold suggests housing could continue to decline, but it also suggests (as he pointed out to me) that the ratio might be approaching levels (operative word is might; please read the HUGE GIANT BIG FAT DISCLAIMERbelow) which suggest selling gold to buy real estate. This is NOT INVESTMENT ADVICE, and excuse me for shouting; it is merely the freely offered rantings of an amateur observer. We all want a simple investment strategy that works in all time frames and all eras--but no such strategy exists once you understand purchasing power and relative performance/ratios/ pairings. All we can do as investors and speculators is observe the extremes of various valuations and attempt to preserve or grow our purchasing power--be it in dollars, housing, gold, stocks, land, future contracts, oil, sugar or quatloos. I've been away from my desk for a week so I apologize for the tardy email responses. You can also find my work on AOL's Daily Finance and Seeking Alpha. "Your book is truly a revolutionary act." Kenneth R. Thank you, Michael H. ($15), for your second extremely generous donation to this site. I am greatly honored by your support and readership.The first chart is the S&P Case-Shiller House Price Composite (black line). The red line is an RS (relative-strength) of the composite to gold. Historical comparison suggests home prices are still overvalued. The red line indicates that homes are worth in gold what they were in the late 1980's while nominal prices remain elevated.

Permanent link: Deflation or Inflation: Who Cares?

Check out my article in American Conservative Magazine No Easy Money: The case for raising interest rates.

If you want more troubling/revolutionary/annoying analysis, please read Free eBook now available: HTML version: Survival+: Structuring Prosperity for Yourself and the Nation (PDF version (111 pages): Survival+)

Of Two Minds is now available via Kindle: Of Two Minds blog-Kindle