Bernanke, Goldilocks and The Red Queen

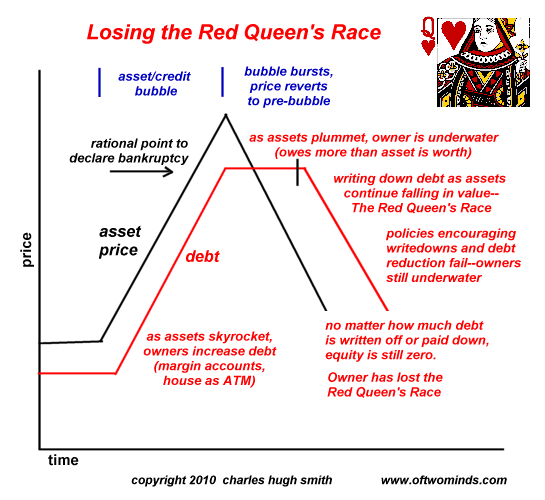

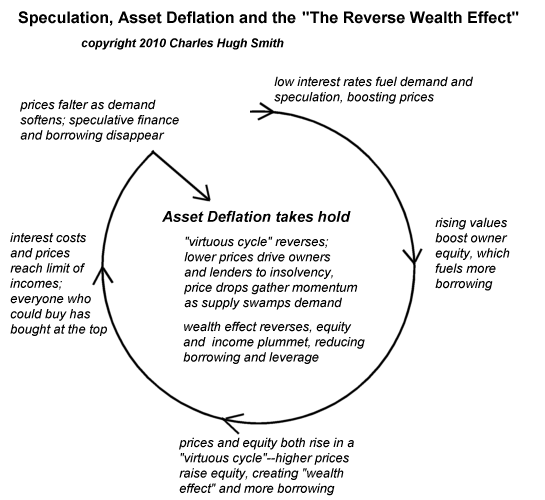

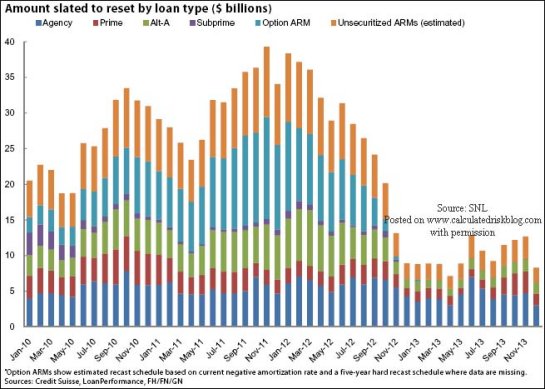

Bernanke has bet his bankroll on Goldilocks, but the Red Queen trumps the golden girl. You remember the "Goldilocks Economy:" not too hot (inflation), not too cold (low growth). That was the Greenspan era's great accomplishment: Federal Reserve manipulation--oops, I mean policy--kept the economy growing nicely but not "hot" enough to trigger inflation. At least that was the "story." The Global Financial Meltdown revealed the story as fiction rather than fact. Super-low interest rates, unlimited liquidity led to rising speculative debt and risk-taking and massive asset bubbles, which subsequently popped, like all such speculative bubbles. Which brings us to the second fictional female character of the story: The Red Queen. I covered the Red Queen's explanatory role in Losing the Red Queen's Race(February 17, 2010) Here's another look at the Red Queen's Race, a.k.a. the "reverse wealth effect:" Which brings us to Bernanke's "extend and pretend" policy--a variation on the Goldilocks story. The basic game plan was originated by former Fed Chairman Paul Volcker as a way of extracting U.S. global banks from insolvency back in the 1980s. The global banks couldn't resist gorging on high-yielding Latin America debt, and when "the music stopped" (heh) then the bagholders were the banks. In today's political environment, the banks would simply transfer the trillions in toxic debt to the government or its proxies, but Volcker conjured an "earnout" path out of the abyss: banks could "extend and pretend" their bad debt, writing off only as much as their earnings could offset. Volcker put the hammer on the banks' speculative instincts (profits are private, baby, but losses are public) as the "cost" for their big bets gone bad, and over time the insolvent giants earned their way to solvency. That is precisely the Bernanke game plan, with a Goldilocks twist: the plan is to keep the economy growing and inflation rising, but not too "hot," while avoiding the chill of deflation and recession. With zero-interest rate policy (ZIRP) in place, the banks can earn billions from skimming, enabling them to write down their monumental losses a bit at a time. In the meantime, all their impaired mortgages are kept on the books as "performing assets" or "real estate owned" at marked-to-2007-prices: the very acme of extend and pretend. The problem with Ben's strategy is the Red Queen trumps Goldilocks. Real estate assets are falling faster than debt is being written off, so the equity of homeowners and lenders remains unchanged--in many cases, less than zero. Mortgages have declined a meager $350 billion from the bubble top in 2007: mortgages totalled $10.5 trillion then and $10.15 trillion now. Meanwhile real estate has lost $8 trillion in value and homeowner's equity is hovering below 40%. Bernanke is trying to maintain a Goldilocks economy, but the conditions are different from the 1980s. 1. Reinflating asset bubbles to create a "wealth effect" has goosed commodities and inflation. The Fed's money-pumping has certainly goosed the stock market, but it's also goosed commodities, sending grain, sugar, copper, silver, rice etc. to the moon. Consumers are spending more for essentials, and paying sharply higher local government fees and taxes. As rising commodity prices and taxes sap the consumers' stagnant income, there is little left to support the self-sustaining slow-and-steady growth Goldilocks economy Bernanke wants. Rising prices and taxes are drags on an economy burdened by high debt: the Red Queen trumps again, as any modest increases in household income are siphoned off to pay higher prices and taxes. 2. The "growth" is all Fed and Federal government pumping. The banks' balance sheets may look better with the goosed assets rising, but the Goldilocks economy is experiencing no self-sustaining growth. The only thing keeping it warm is Federal and Fed stimulus: the government has borrowed and pumped $5 trillion into the economy since 2008, and trillions more in off-balance sheet financial guarantees and largesse to the banking sector. The Fed's balance sheet has ballooned by $2 trillion as it propped up the housing market and now the stock market. 3. Housing is still in a supply-demand downtrend. Despite buying $1.2 trillion in impaired mortgage-backed securities from the banks to take the bad debt off their books, the housing market's organic (once the intervention ends) trend is down. There is too much inventory, too much impaired debt, etc., and the mortgage resets keep coming: Resets of adjustable loans to fixed-rate loans are not a problem with rates being low; the problem is ARMs (adjustable rate mortgages) which are moving from near-zero "teaser" rates to market rates of 5%, or interest-only loans which are resetting to pay principal. The payments are those loans will leap up signficantly, pushing more marginal homeowners into default and foreclosure. 4. Interest rates and yields are rising despite Fed manipulation, and that matters in an economy burdened with unprecedented debt. The household may be lightening credit cards by trivial sums, but it's still being crushed by sagging house prices and high mortgage debt. Corporations have induldged in a veritable orgy of debt as rates fell, and the Federal government has tripled its external debt from $3.3 trillion to $9.5 trillion in a few short years--and it's adding to that mountain at the rate of $1.5 trillion a year, 11% of the nation's GDP, with no end in sight. The bond market isn't buying the idea that the Fed can keep interest rates at near-zero forever, or that the Fed's massive interventions are truly creating self-sustaining growth. So interest rates are rising, meaning that current bond holders of long-term Treasury debt (including the Fed) will take a horrendous 40% haircut as rates rise from 3% to 5%. A $100 bond paying 3% will drop to $60 when yields rise to 5%, as buyers will demand the same 5% yield as they can get with newly issued bonds. Rising rates will crush the asset base of all long-term bond holders. The Red Queen trumps again: you try to race ahead of falling asset prices by lowering interest rates to zero, all you do is set up a crushing decline in bond values later when rates inevitably climb back to historic levels. 5. Rising rates and commodity prices are crushing profit margins. The basic idea in a Goldilocks economy is that low interest rates will encourage households and businesses to spend more and expand, but not so fast that inflation is aroused from its slumber. The cheap money isn't flowing into consumption--the "house as ATM machine" is gone. It's flowing into speculation and into rolling over old debt, at least for those who can qualify for the new cheap debt. That speculation is creating new asset bubbles in commodities and stocks, but there is no Goldilocks effect from these bubbles: only 20% of households own enough financial assets to feel any 'wealth effect," and it's really only the top 10% who are significantly wealthier as a result of the reinflation bubbles. Meanwhile, the bottom 90% are paying higher prices and fees as their incomes stagnate. The "wealth effect" has failed to "trickle down." Businesses' wholesale costs are rising, but they can't pass those costs on to retail as the average household's disposable income is stagnant or down. So the net result of speculative bubble blowing is margin collapse, which will take away the one leg holding up the "stocks are going to the moon" story. The banks are profiting handsomely from the reflated assets bubbles, but this isn't a Goldiocks scenario: it's a Red Queen setup. Once the newly reflated speculative bubbles pop, then the banks will be back to running in place as their assets are falling faster than their writedowns. Bernanke, you will lose your $2 trillion gamble: the Red Queen trumped Goldilocks. New recipes on What's for Dinner at Your House?--Elsewhere Cafe Muffins, and Louisa's Vegetarian Baked Beans Of Two Minds is also available via Kindle: Of Two Minds blog-KindleThe Red Queen's race refers to running very fast to stay in the same place. As asset values fall globally (except where massive government stimulus has pushed the day of reckoning forward a bit), debt holders are frantically paying down or writing down debt--running very fast--but finding themselves in the same place--zero equity--despite their prodigious efforts.

If you would like to post a comment, please go to DailyJava.net.

Order Survival+: Structuring Prosperity for Yourself and the Nation or Survival+ The Primer from your local bookseller or from amazon.com or in ebook and Kindle formats.A 20% discount is available from the publisher.Thank you, Robert H. ($20), for your most generous contribution to this site-- I am honored by support and readership. Thank you, Michael M. ($50), for your astoundingly generous contributions to this site-- I am greatly honored by your correspondence and readership.