Some Thoughts on Investing in the "Bottom" in Housing

Investor buying has helped put a floor under the housing market. The rental housing market is currently robust, but that is dependent on a highly artificial economy supported by unprecedented government stimulus and transfers.

In my previous entry on housing's presumptive "bottom," ( The Housing Recovery: Based on What? June 20, 2012), I showed that the conventional foundations of the housing market were impaired: demand was weakened by demographics and declining income/employment, and supply was still well above the organic growth of new household formation.

The housing "Bulls" who think the millions of young people living in basements can afford to buy a house despite having high student debt, little job security and declining incomes are either delusional or they are studiously ignoring the causal relation between buying a house and qualifying for a conventional mortgage, i.e. the financial factors of current debt loads, income, the need for a down payment, etc.

The majority of wage earners have seen real incomes decline and most households have high debt levels.

Not buying a house is a choice for a relatively few who qualify but who choose to rent. The vast majority of people who do qualify to own a home by conventional standards already own a home (65% of all households). Those who don't own generally do not qualify due to insufficient income, heavy debt loads, poor credit, etc.

There are two significant pools of buyers, however, who have become very active in the U.S. and Canadian real estate markets: domestic and overseas investors.Their buying has soaked up quite a bit of inventory--up to 40% of all home purchases in some areas have been all cash, a transaction that typifies investor buying rather than young people moving out of basements.

Each pool of investors is motivated by different forces. Domestically, the Federal Reserve's ZIRP (zero-interest rate policy) has turned cash into trash, and investors desperate for a return above 2% without the risks of the stock market casino have flooded into the rental housing market.

In California, roughly 30% of all house purchases have been for cash (investors). Some may be planning to improve and then "flip" the house as the market improves (the housing bubble redux strategy), while others are assembling a portfolio of rental properties.

I recently came across a local real estate listing in a desirable Bay Area (Northern California) location (near a University of California campus) for a multi-unit rental building: $4.9 million for 40 units, with a net of all expenses of $150,000 (not counting depreciation or tax benefits). That's a 3% return on a cash purchase, but the real yield is much higher if the buy is made with a 35% cash down payment and 65% mortgage. Regardless of the financing, the yield instantly doubles with depreciation and basic tax benefits, and could even be higher in some circumstances.

The higher yield and relatively low risk of owning rentals in a high-demand area make real estate more attractive than other investments such as 10-year bonds or dividends. As a bonus, if housing does recover, there is the potential for a capital gain.

The appeal of rental housing is understandable, and it has long been a favored investment for households (as opposed to institutional investors). According to a March 1996 report from the Census Bureau (I couldn't locate any more recent data), 92% of the nation's rental housing was owned by individual investors. In other words, owning rental property has long been a localized "Mom and Pop" enterprise.

Here is a Quick Fact Sheet on rentals in the U.S. from the National Multi-Housing Council (NMHC). According to this data, there are about 40 million households in rental housing and 78 million households in owner-occupied housing.

Owning rental property as an investment is not like owning a bond or stock or gold.Housing is a "real-world" investment that irrevocably decays with time. Heaters fail in the dead of winter, the roof eventually needs to be replaced, the yard must be maintained, and rapacious local governments generally view property owners as tax donkeys who they can load with ever-higher property taxes unless they are restrained by Prop 13-type limits.

Rental housing is also a "people business:" some tenants might disturb other tenants, others might not pay the rent, and so on. A renter is a customer, though newly minted landlords often seem to regard the tenant as an ATM machine whose only function in life is paying the rent.

The point here is the higher yield promised by rental property must be earned.Those with no experience in rental housing will learn this the hard way. All the rosy projections of steady profits vanish if vacancies rise above a very low level.

The price of rentals, like almost everything, is set on the margins. If the inventory of rentals rises above demand, then prices will eventually decline. In areas with limited inventory and strong demand (Manhattan, San Francisco, etc.), rents are generally high and the rental properties fetch a premium.

In areas without such geographical constraints, the market for rentals might not be so favorable.

In other words, it's quite possible to lose money buying and managing rental housing. There is nothing guaranteed about the return, as there are so many inputs and variables. It can be a profitable business, but that is not guaranteed.

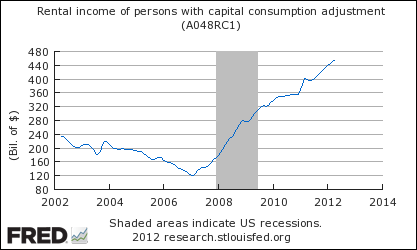

In this chart, we can see the decline in rental income as marginal buyers became homeowners in the housing bubble, and the subsequent rise in rental income as former homeowners returned to the rental housing market.

But this rise in rental income occurred in an era that has been distorted by unprecedented Federal transfer payments, stimulus, etc., and unprecedented intervention in capital and credit markets by the Federal Reserve. The total sum of "extra money" borrowed (or printed) and injected into the economy exceeds $8 trillion, and this does not count banking-sector backstops and guarantees. The U.S. economy was not allowed to experience a "burn the deadwood and rejuvenate the forest" recession, and demand for housing, owner-occupied and rental alike, has been artificially supported by near-zero interest rates, enormous deficit spending and transfer payments.

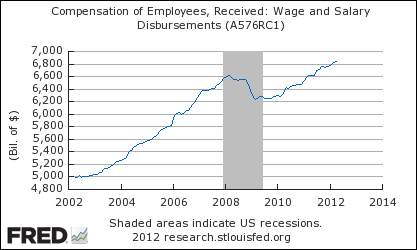

We can see some of the consequences of borrowing and spending $1.5 trillion a year in these charts. The first chart is employee compensation, wages and salaries. It has recovered smartly from its shallow recessionary trough and has risen above 2007 levels.

One would hope that borrowing and spending trillions of dollars would support employment, but the question raised here is whether the stimulus required to keep employment aloft is sustainable.

Here is a chart of personal transfers, cash transferred by the government to individuals. This has risen by $1 trillion a year in a decade, and roughly $400 billion since late 2007.

If we subtract transfer payments from real personal income, we get a more realistic snapshot of the household economy: minus government transfers, personal income is still about $400 billion below its pre-cression peak.

Thus the rental housing market has yet to experience a "real recession." When it does, household formation may well decline or even go negative and rents may well decline as demand falls and supply of rentals rises as millions of previously owner-occupied units go on the market as rentals.

There are a number of potential (but by no means guaranteed) secondary forces that may influence rents and the value of rental property.

1. Some new landlords may realize the business isn't as easy as expected. Some may decide to cut their losses by dumping their property back on the market.

2. Investors who planned to improve and "flip" the unit may find they can't unload the property, and so they become reluctant (and thus very possibly incompetent) landlords.

3. A peculiar feedback loop may arise as the rental market is flooded with new investor-owned inventory. Rents start declining as landlords tire of vacancy-created losses, and that pushes the value of all homes in the area down, owner-occupied and rentals alike.

4. The trend to "double up" and rent out rooms could go mainstream. These "informal" rentals are already standard practice in high-rent areas such as those found around large universities and geographically constrained markets. For example, it is not unusual for four co-eds to share a 2-bedroom apartment.

Outside these high-demand markets, people who lose their job or see their hours cut to the point they cannot afford their own apartment will move in with family or friends. Anecdotally, I have heard of Mom clearing out the dining room for a returning son and his family.

There are roughly 19 million vacant dwellings in the U.S., of which around 4 million are second homes and a million or two are on the market. Let's stipulate that several million more are in areas with very low demand (i.e. few want to live there year-round). Let's also stipulate that several million more are in the "shadow inventory" of homes that are neither on the market nor even officially in the foreclosure pipeline, i.e. zombie homes.

Even if you account for 9 million of these homes, that still leaves 10 million vacant dwellings in the U.S. which could be occupied. That means 1 in 12 of all dwellings are vacant. Even if you discount this by half, that still leaves 5 million vacant dwellings that could be occupied. Given that the total rental market is 40 million households, that constitutes a very large inventory of supply that remains untapped.

Lastly, it is important to note that the ratio of residents to dwellings is rather low in the U.S., with millions of single-person households and large homes occupied by one or two people. The potential pool of existing homeowners who could enter the "informal" rental market by offering bedrooms, basements and even enclosed garages for rent is extremely large, and that is a difficult-to-count "shadow" inventory of potential rentals.

All of these forces will play out differently in each neighborhood, town and city, depending on the inventory of rentals, the geographical constraints, the employment picture and a host of other factors. The key point here is that the rental market's current robustness is at least partially dependent on unprecedented government stimulus/transfers. The current strength may be temporary rather than permanent.

The second take-away is that demand could weaken considerably in a "real recession" even as supply increases due to millions of investor-owned properties hitting the rental market and the "informal rental" market expanding as people with mostly empty houses seek additional income or accept relatives/friends with a need for shelter.

GARDEN SEED SPECIAL--10% OFF ALL EVERLASTING SEEDS--all seeds are organic.Here is a snapshot of Everlasting Seeds' zucchini coming up in my little urban garden a week ago. This wonderful variety produces all the way into autumn. (ES-seed beets are visible in the foreground.)

My gardening style aims at maximizing opportunities for pollinators and birds, so I let California poppy and alyssum volunteers flower alongside vegetables, and I let plants that produce abundant seeds for birds (chard and kale) go to seed. As a result, our little garden is always busy with pollinator insects and birds. It is a delight to simply watch Nature at work.

So for goodness sake, if you don't have even a single veggie planted yet, order some Everlasting Seeds today and get planting. The rewards are immense.

For small gardens: The Simple Garden - Special price: $29.95 + $8.00 shipping

Contains 30 seeds of each: Corn Broccoli Pea Onion Radish Carrot Cabbage Tomato Cauliflower Spinach Lettuce Pole Bean

Contains 30 seeds of each: Corn Broccoli Pea Onion Radish Carrot Cabbage Tomato Cauliflower Spinach Lettuce Pole Bean

Resistance, Revolution, Liberation: A Model for Positive Change (print $25)

Resistance, Revolution, Liberation: A Model for Positive Change (print $25)(Kindle eBook $9.95)

We are like passengers on the Titanic ten minutes after its fatal encounter with the iceberg: though our financial system seems unsinkable, its reliance on debt and financialization has already doomed it.We cannot know when the Central State and financial system will destabilize, we only know they will destabilize. We cannot know which of the State’s fast-rising debts and obligations will be renounced; we only know they will be renounced in one fashion or another.

The process of the unsustainable collapsing and a new, more sustainable model emerging is called revolution, and it combines cultural, technological, financial and political elements in a dynamic flux.History is not fixed; it is in our hands. We cannot await a remote future transition to transform our lives. Revolution begins with our internal understanding and reaches fruition in our coherently directed daily actions in the lived-in world.

| Thank you, Sriram E. ($100), for your outrageously generous contribution to this site--I am greatly honored by your support and readership. |