Money Velocity Free-Fall and Federal Deficit Spending

The velocity of money is in free-fall, and borrowing, squandering and printing trillions of dollars to prop up a diminishing-return Status Quo won't reverse that historic collapse.

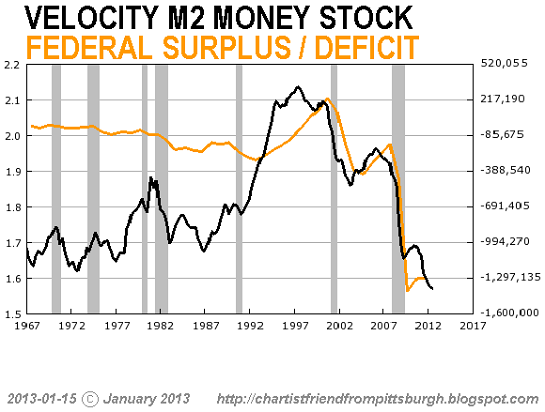

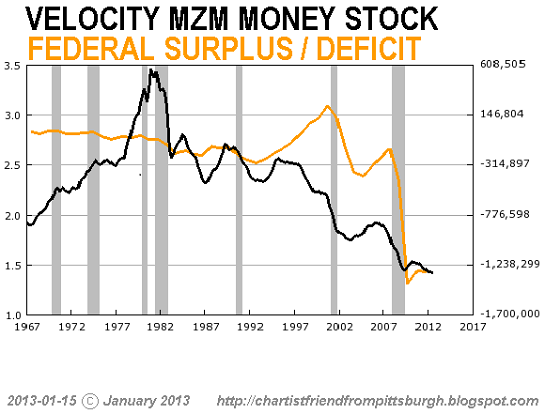

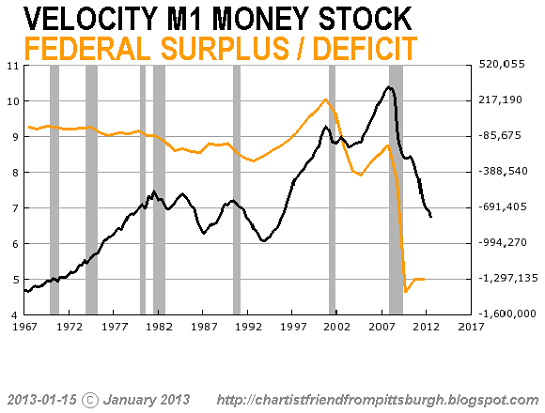

Courtesy of Chartist Friend from Pittsburgh, here are three charts overlaying the velocity of money and the Federal surplus/deficit. The charts display the three common measures of money: M1, M2 and MZM. From the St. Louis Federal Reserve site:

M1 includes funds that are readily accessible for spending. M1 consists of: (1) currency outside the U.S. Treasury, Federal Reserve Banks, and the vaults of depository institutions; (2) traveler's checks of nonbank issuers; (3) demand deposits; and (4) other checkable deposits (OCDs).

M2 includes a broader set of financial assets held principally by households. M2 consists of M1 plus: (1) savings deposits (which include money market deposit accounts, or MMDAs); (2) small-denomination time deposits (time deposits in amounts of less than $100,000); and (3) balances in retail money market mutual funds (MMMFs).

Money Zero Maturity (MZM) is M2 less small-denomination time deposits plus institutional money funds.

The correlation of deficit spending and money velocity is especially striking in the chart of M2 velocity.

Here is MZM velocity:

And M1 velocity:

Since correlation implies causation, ideologically unbiased observers will wonder: does declining money velocity lead to more deficit spending, or does deficit spending depress money velocity?

Alternatively, both declining money velocity and soaring deficits reflect a contracting, post-credit-bubble economy. It is interesting to compare when the various measures of money velocity bottomed and topped out:

-- M1 velocity rose straight through the inflationary 1970s (no surprise there), chopped around the expansionary 1980s and then climbed along with the Bull market in stocks from 1994 to a peak in 2007, matching the peak in stocks and housing almost perfectly.

-- M2 velocity first peaked during the height of inflation in 1981 (when interest rates also peaked), bottomed in 1987 and then tracked the stock market and economy higher, reaching a much higher peak in 1997, much earlier than M1 velocity. M2 fell substantially to a low in 2002 and then rebounded modestly to a lower peak in 2007, after which it collapsed.

-- MZM velocity topped out in the inflationary surge of the early 1980s, like M2, but unlike the other measures, it did not ascend to new heights in the 1990s or 2000s; rather, it has fallen steadily for 30 years since its 1982 top.

The most striking feature of these charts is the complete collapse of money velocity. MZM and M2 have collapsed to historic lows, while M1 has fallen back to 1982 levels.

In this context, we can view unprecedented Federal deficit spending as a misguided attempt to compensate for the implosion of money velocity. I say "attempt" because the Treasury borrowing and blowing $6 trillion over the past five years and the Federal Reserve printing $2 trillion, backstopping the parasitic financial cartel with $16 trillion and buying over $1 trillion each of mortgage securities and Treasury bonds has only kept the economy stumbling along at essentially zero growth while real wages have declined by 7% to 9%.

This stupendous creation of money and unprecedented fiscal stimulus has had zero effect on money velocity. This conclusively shows that fiscal and monetary stimulus are not fixing what's broken with money velocity.

Please see these entries for more on why this is so:

Misunderstanding Austerity, Stimulus and Demand (January 17, 2013)

Why Expansionist Central States Inevitably Implode (January 15, 2013)

The Neoliberal Financial Skim (January 14, 2013)

Why Austerity Is Triggering a Crisis (January 7, 2013)

Keynesian stimulus policies (deficit spending and low-interest easy money) create speculative credit bubbles. As the above charts illustrate, post-bubble economies do not respond to additional stimulus because the economy is burdened by impaired debt and phantom collateral.

In sum, the U.S. economy is a neofeudal debt-serf wasteland with few opportunities for organic (non-Central Planning) expansion. As a result, the velocity of money is in free-fall, and borrowing, squandering and printing trillions of dollars to prop up a diminishing-return Status Quo won't reverse that historic collapse.

Put another way: we've run out of speculative credit bubbles to exploit.

New instrumental song (5:36) by CHS and Coconut Cosmos: Alex and Daz Theme (raggae/rock/jazz with a blistering solo--don't miss it!)

New instrumental song (5:36) by CHS and Coconut Cosmos: Alex and Daz Theme (raggae/rock/jazz with a blistering solo--don't miss it!)

LAST WEEK OF DISCOUNTS: My new book Why Things Are Falling Apart and What We Can Do About It is now available in print and Kindle editions--10% to 20% discounts.

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify or understand. We will cover the five core reasons why things are falling apart:

1. Debt and financialization

1. Debt and financialization

2. Crony capitalism and the elimination of accountability

3. Diminishing returns

4. Centralization

5. Technological, financial and demographic changes in our economyComplex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Not accepting responsibility and being powerless are two sides of the same coin: once we accept responsibility, we become powerful.

10% discount on the Kindle edition: $8.95(retail $9.95) print edition: $24 on Amazon.com

To receive a 20% discount on the print edition: $19.20 (retail $24), follow the link, open a Createspace account and enter discount code SJRGPLAB. (This is the only way I can offer a discount.)

1. Debt and financialization2. Crony capitalism and the elimination of accountability

3. Diminishing returns

4. Centralization

5. Technological, financial and demographic changes in our economyComplex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Not accepting responsibility and being powerless are two sides of the same coin: once we accept responsibility, we become powerful.

10% discount on the Kindle edition: $8.95(retail $9.95) print edition: $24 on Amazon.com

To receive a 20% discount on the print edition: $19.20 (retail $24), follow the link, open a Createspace account and enter discount code SJRGPLAB. (This is the only way I can offer a discount.)

| Thank you, Helen S.C. ($10), for yet another extremely generous contribution to this site -- I am greatly honored by your steadfast support and readership. | Thank you, Barney S. ($5), for yet another extremely generous contribution to this site --I am greatly honored by your continuing support and readership. |