"The Carrot's in Reach:" The Myth of a Self-Sustaining Recovery

The carrot of self-sustaining recovery will remain out of reach, for the policies presented as the path to recovery preclude the "virtuous cycle" everyone desires.

The enduring myth of the post-2008 era is that central-planning money printing and deficit spending would soon spark a self-sustaining recovery. Once consumers and businesses stepped up their own borrowing and spending, the central bank and state would then pare back money printing and deficit spending, as the increase in private-sector spending would fuel further borrowing and spending, i.e. become self-sustaining.

The reality is the mythical self-sustaining recovery is the carrot dangled in front of a credulous public:though we're constantly reassured "we're almost there" (the promised land of self-sustaining recovery), the mythical recovery remains out of reach, no matter how much money is printed or borrowed and blown in fiscal stimulus.

There are several key reasons for this.

1. As noted yesterday, consumption is not investment, no matter how many times you call consumption "an investment." Investment is planting one's seed corn (capital) wisely. Consumption ($300 million fighter aircraft, $70,000 biopsies, McMansions in the middle of nowhere, endless subsidies of housing and banking, etc.) is turning the seed corn into sour mash and indulging in a drunken orgy of squandered debt that cannot and will not be paid back in dollars with today's purchasing power.

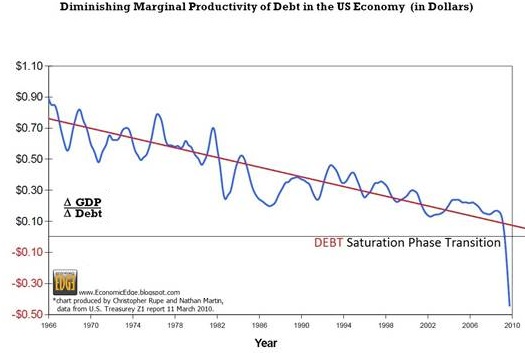

2. Borrowing money (debt) yields diminishing return. There's this funny little thing called interest that piles up in a borrowing spree that eventually siphons off much of the debtor's income stream, effectively impoverishing the borrower.

There's another funny thing called mal-investment or mis-allocation of capital: when the borrowed money is nearly free (low interest rates), then even poor quality bets (oops, I mean "investments") get funded. This is especially true if the winnings are yours to keep but any losses you incur are covered by Big Brother--the Federal Reserve or the U.S. Treasury--and the taxpayers the government has indentured to the banking sector.

3. Debt that cannot be written down because that would impair the politically powerful financial sector remains a tightening noose around the throat of the economy. Capitalism requires creative destruction, which includes the liquidation of bad bets and unpayable debt. Since that is verboten in our State-managed crony-capitalism system, the impaired debt remains on the books, supported by endless government subsidies.

Both the phantom collateral and the subsidies derange and distort the markets, leading to further bad decisions as risk has been obscured.

4. As analyst Ramsey Su recently observed, It is obvious that the central banks of the world have printed too much money, (which) all went into the wrong hands and now has nowhere to go. In the oft-propagated myth of central bank intervention, helicopters drop cash into the economy to stimulate demand for goods and services, sparking the "virtuous cycle" of a self-reinforcing recovery.

But the money isn't dropped into households or the real economy--it's dropped into banks, which use it for speculation or funding cronies' speculations and asset grabs. If the Federal Reserve had wanted to do a real helicopter drop of money, it could have sent $10,000 in cash to every taxpayer. Instead, it lavished at least $23 trillion in subsidies, backstops and guarantees on the Too Big To Fail banks and the mortgage industry.

This neofeudal distribution of $7 trillion in new Federal debt to taxpayers and the Fed's trillions in "free money" to the parasitic financial sector has carved out a vicious cycle of lower real household incomes, higher interest payments and new asset bubbles in stocks, bonds and housing. These trillions of dollars in freshly issued money have flowed to financiers who have used it to chase yield in one asset class or another.

As a result of these neofeudal policies, the economy is now perched precariously on the edge of multiple asset bubbles and demographically impossible-to-fulfill promises of entitlements and other giveaways (such as mortgage/housing subsidies and a variety of corporate welfare scams).

The carrot of self-sustaining recovery will remain out of reach, for the policies presented as the path to recovery preclude the "virtuous cycle" everyone desires.

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify or understand. We will cover the five core reasons why things are falling apart:

1. Debt and financialization

1. Debt and financialization2. Crony capitalism and the elimination of accountability

3. Diminishing returns

4. Centralization

5. Technological, financial and demographic changes in our economy

Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Not accepting responsibility and being powerless are two sides of the same coin: once we accept responsibility, we become powerful.

Kindle edition: $9.95 print edition: $24 on Amazon.com

To receive a 20% discount on the print edition: $19.20 (retail $24), follow the link, open a Createspace account and enter discount code SJRGPLAB. (This is the only way I can offer a discount.)

| Thank you, William B. ($100), for your outrageously generous contribution to this site -- I am greatly honored by your steadfast support and readership. | Thank you, Don B. ($50), for your supremely generous contribution to this site --I am greatly honored by your steadfast support and readership. |