How Incremental Increases Can Lead to Systemic Collapse

Healthcare insurance illustrates how incremental increases can lead to systemic collapse.

My father's paystubs from the 1940s, 50s and 60s shed light on the way seemingly modest incremental increases can lead to systemic collapse. My father used his G.I. Bill education benefits to attend college after the end of World War II in 1945, but left to join Sears, Roebuck and Company in 1947. He worked for Sears until the mid-1960s.

I think we can safely assume Sears was a typical corporate employer of the day. It was known at the time for a generous profit-sharing program and well-regarded management training program to recruit management from within the ranks.

My father's paystub from June 1947 was handwritten. There is a box for "hospital group insurance" but there was no deduction made. The stub indicates my father worked 40 hours that week and earned $36 gross income. After deductions of $4.40 for income tax, 36 cents for unemployment insurance, etc., his net pay was $30.88.

Since he was unmarried, I assume he'd opted out of the hospital group insurance.

By 1951, he was married and had one child, and his July 1951 paystub shows 88 hours worked (working Saturdays was typical in retail), earning a gross pay of $166.40 and a $3 deduction for hospital group insurance. How much Sears paid (if any) of this policy premium is unknown. The $3 works out to 1.8% of his gross pay.

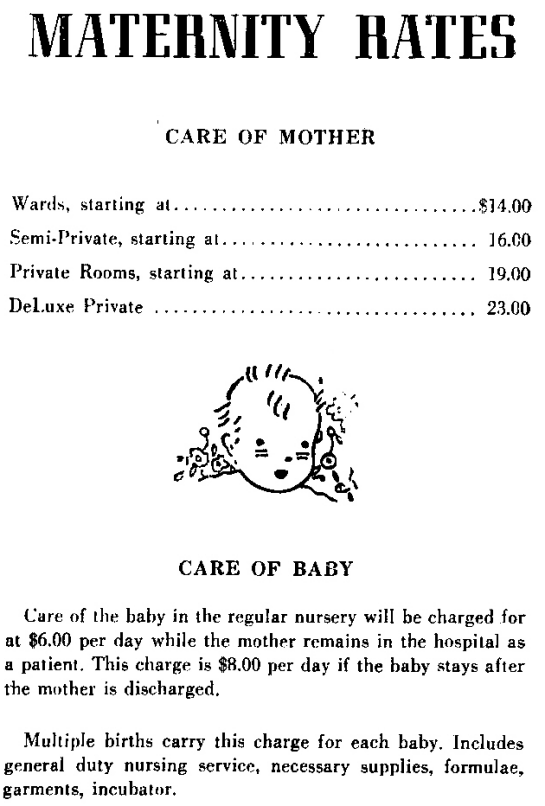

My second sister was born less than a year later in March 1952. Here are the total costs of her birth at one of the finest hospitals on the West Coast, The Santa Monica Hospital:

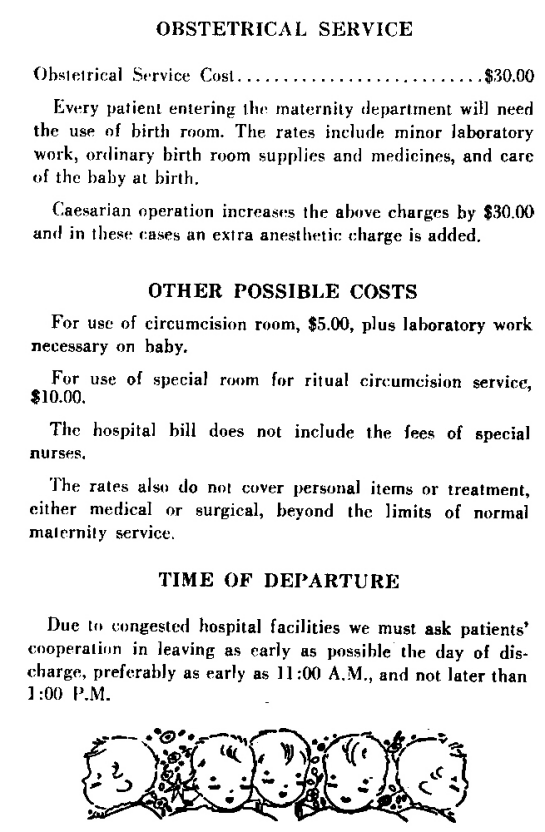

And here are the obstetrical rates:

Having a baby cost $30, which is today's dollars is $264. A private deluxe room cost $23 or $203 in today's dollars. According to the Bureau of Labor Statistic'sinflation calculator, $1 in 1952 is $8.81 in 2013 dollars.

I first published these documents in The "Impossible" Healthcare Solution: Go Back to Cash (July 29, 2009).

To the best of my knowledge, my father's employer-managed hospital group insurance did not cover childbirth. These expenses were paid in cash, as were all doctor's visits and medications. The hospital group insurance helped pay for accidents and illnesses serious enough to land someone in the hospital.

By the early 1960s, my Dad was earning $825 per month and the hospital group insurance deduction was $5.20. For context, his Group Life Insurance deduction was twice as much, $11. His net pay after taxes, the group insurance deductions and profit-sharing was $672.

Even if Sears was contributing more than 50% of the hospital group insurance, the total sum paid by employer and employee was 2% of gross wages. (By this time there were four kids, so the insurance covered a family of six.)

As an employer myself in the mid-1980s, we paid the total cost of our employees' healthcare insurance, though Hawaii state law only required that we pay 50%. The cost for single workers was around $45/month and for families of four around $150/month. Gross pay for employees ranged between $1100 and $1700 per month.

In 2013 dollars, that is equivalent to $97/month and $325/month.

As a self-employed non-poverty level household, we pay 100% of healthcare insurance costs ourselves. For a stripped-down plan with no dental, eyewear or medication coverage (all those must be paid in cash), the monthly cost is $1,136 for two people. Yes, there is an age differential, but our younger friends with one child pay roughly the same per month. Ironically, perhaps, this works out to nearly 20% of our income--the same percentage healthcare consumes of the American GDP (healthcare is 18% of the $16 trillion economy.)

Five years ago, our monthly healthcare insurance was $635. This near-doubling of healthcare insurance costs is not unique to us; we are not outliers, we are merely one data point among millions seeing these kinds of increases.

Last time I paid nearly $400 for a small tube of medication (a cream that's been off-patent for years) at the pharmacy, the pharmacist muttered under her breath that "you have to be rich or poor so the government pays for everything."

The notion that employers should pay for employees' group healthcare insurance was not reached by careful consideration of future consequences or alternatives.The idea arose when group healthcare insurance was a trivial cost. Now that it has incrementally risen by roughly ten-fold, it is no longer trivial. It is hollowing out what's left of the middle and is on track to bankrupt the nation.

This is how incremental increases can lead to systemic collapse.

Note to readers: my workload the next three weeks is off the scale so my ability to respond to email will be near-zero. Blog postings may be sporadic as well. Your patience and understanding are greatly appreciated.

Note to readers: my workload the next three weeks is off the scale so my ability to respond to email will be near-zero. Blog postings may be sporadic as well. Your patience and understanding are greatly appreciated.

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify or understand. We will cover the five core reasons why things are falling apart:

1. Debt and financialization

1. Debt and financialization2. Crony capitalism and the elimination of accountability

3. Diminishing returns

4. Centralization

5. Technological, financial and demographic changes in our economyComplex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Not accepting responsibility and being powerless are two sides of the same coin: once we accept responsibility, we become powerful.

Kindle edition: $9.95 print edition: $24 on Amazon.com

To receive a 20% discount on the print edition: $19.20 (retail $24), follow the link, open a Createspace account and enter discount code SJRGPLAB. (This is the only way I can offer a discount.)

| Thank you, Stephen L. ($5/month), for your supremely generous subscription to this site -- I am greatly honored by your steadfast support and readership. | Thank you, William W. ($50), for your monumentally generous contribution to this site -- I am greatly honored by your support and readership. |