We're Relying on Phantom Wealth to Fund Our Retirement

Phantom wealth cannot possibly fund unprecedented retirement and healthcare promises.

The narrative that Social Security, Medicare and pension funds invested in stocks and bonds can fund the retirement of 65 million people is a misleading fantasy. The sad reality is we can't fund the enormous expense of retirement/healthcare for 20% of the populace out of our national earned income, and the savings that have been set aside are either fictitious (the Social Security Trust Fund) or based on phantom wealth created by speculative asset bubbles in stocks, bonds and real estate.

I explain the fraud of the Social Security Trust Fund in detail in The Fraud at the Heart of Social Security (January 17, 2011).

In the bogus "Trust Fund," the cash has been siphoned off and spent on Federal government outlays. The Fund holds no cash. Instead, it has been given IOUs "backed by the full faith and credit of the United States," the non-marketable securities.

Now what happens when the Social Security system redeems $100 billion of those securities? the Treasury goes out and borrows the $100 billion on the global bond market, and taxpayers are on the hook for the debt and the interest on that freshly issued debt.

This isn't that difficult to understand, but let's go through it again:

In a real Trust Fund, taxpayers pay in their cash, and the surplus cash is invested in marketable bonds--not IOUs, but real assets that pile up in the Trust Fund just like savings in a savings account. That cash is then withdrawn later, as needed, via the sale of bonds purchased with the cash. Taxpayers (employees and employers) pay nothing above and beyond their payroll taxes to fund Social Security.

In the fraudulent "Trust Fund," taxpayers' Social Security taxes have been squandered on other Federal expenses, and they have to pay interest on Treasury debt which is borrowed to pay their SSA benefits. In other words, taxpayers pay twice: once via Social Security taxes, a substantial 12.4% of all wages, and then they pay again to borrow cash on the bond market to actually pay the Social Security benefits.

Medicare is equally unsustainable: please read these for the full story:

Rather than face up to the reality that we face an impossible dilemma--either workers will be slowly impoverished by taxes that must go up to fund unrealistic retirement/healthcare promises, or those promises will have to be drastically scaled back--we have chosen to believe the happy illusion that inflating asset bubbles will painlessly conjure up enough phantom wealth to pay all those promises.

How can an unprecedented number of people (65 million Baby Boomers) all retire with unprecedented pension payouts and unprecedented healthcare expenses, and do so without raising taxes? Easy--just inflate asset bubbles that create trillions of dollars in magical wealth.

But as I explained in The Happy Story of Boomers Retiring on Their Generational Wealth Is Wrong (June 25, 2014), the assumption that there will be buyers of stocks, bonds and real estate at bubble-level valuations is not based on demographic realities.

The phantom wealth of asset bubbles is based on anomalously low interest rates and equally anomalous central bank intervention in capital markets. The base assumption is that these anomalous conditions are not anomalous but the New Normal: central banks can intervene without any negative consequences forever, interest rates can be suppressed to near-zero without any negative consequences forever, and sovereign debt (government deficits) can rise indefinitely without any negative consequences forever.

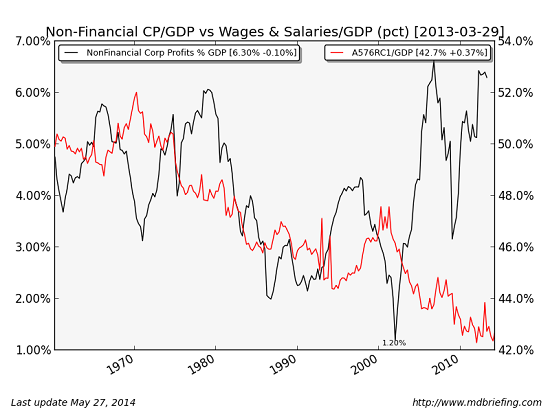

Oh, and corporate profits can also rise indefinitely, too, even as earned income (as a share of gross domestic product--GDP) declines:

To tap this phantom wealth, assets must be sold at bubblicious valuations; this raise the question, Who Will Boomers Sell Their Stocks To? (June 23, 2014)

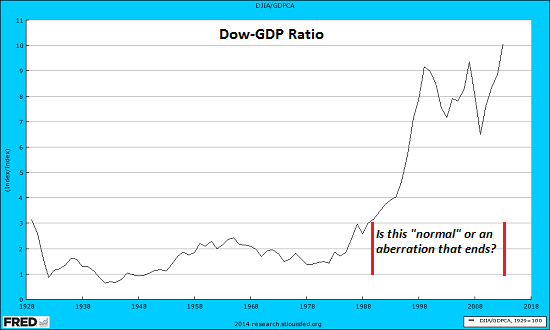

Consider the fundamental relationship of stocks to the nation's gross domestic product (GDP). Current sky-high stock valuations are not just aberrations in terms of previous stock prices--they're aberrations in terms of stocks' valuations compared to the nation's entire economy.

So if bonds decline by 50% as interest rates normalize (i.e. rise), and stocks fall 50% as corporate profits and central bank intervention normalize, and real estate declines 50% in most locales as declining wages meet rising interest rates, then what source of funding will replace the $30 trillion in phantom wealth that evaporated?

Declining wages? A new speculative asset bubble in bat guano?

Perhaps it's time that we face up to the fiscal reality that unprecedented promises can only be paid out of current income and hard assets that can be sold in vast quantities without depressing the price of those assets. As earned income declines as a share of the economy and asset bubbles based on liquidity and financialization pop, we will eventually have to deal with the difficult reality that government debt is not a hard asset that can be sold in vast quantities without depressing the value of that asset.

In sum, phantom wealth cannot possibly fund unprecedented retirement and healthcare promises. Only real wealth can do that, and central bank liquidity and the asset bubbles it inflates are not real wealth.

Are you like me? Ever since my first summer job decades ago, I've been chasing financial security. Not win-the-lottery, Bill Gates riches (although it would be nice!), but simply a feeling of financial control. I want my financial worries to if not disappear at least be manageable and comprehensible.

Are you like me? Ever since my first summer job decades ago, I've been chasing financial security. Not win-the-lottery, Bill Gates riches (although it would be nice!), but simply a feeling of financial control. I want my financial worries to if not disappear at least be manageable and comprehensible.And like most of you, the way I've moved toward my goal has always hinged not just on having a job but a career.

You don't have to be a financial blogger to know that "having a job" and "having a career" do not mean the same thing today as they did when I first started swinging a hammer for a paycheck.

Even the basic concept "getting a job" has changed so radically that jobs--getting and keeping them, and the perceived lack of them--is the number one financial topic among friends, family and for that matter, complete strangers.

So I sat down and wrote this book: Get a Job, Build a Real Career and Defy a Bewildering Economy.

It details everything I've verified about employment and the economy, and lays out an action plan to get you employed.

I am proud of this book. It is the culmination of both my practical work experiences and my financial analysis, and it is a useful, practical, and clarifying read.

Test drive the first section and see for yourself. Kindle, $9.95 print, $20

"I want to thank you for creating your book Get a Job, Build a Real Career and Defy a Bewildering Economy. It is rare to find a person with a mind like yours, who can take a holistic systems view of things without being captured by specific perspectives or agendas. Your contribution to humanity is much appreciated."

Laura Y.

Gordon Long and I discuss The New Nature of Work: Jobs, Occupations & Careers (25 minutes, YouTube)

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

| Thank you, Ron R. ($100), for your outrageously generous contribution to this site -- I am greatly honored by your steadfast support and readership. | Thank you, John R. ($5/month), for your supremely generous re-subscription to this site -- I am greatly honored by your steadfast support and readership. |