The Oil Head-Fake: The Illusion that Lower Oil Prices Are Positive

The essence of the Oil Head-Fake Dynamic is the inevitable drop in oil price due to global recession will trigger disruption of the global oil supply chain.

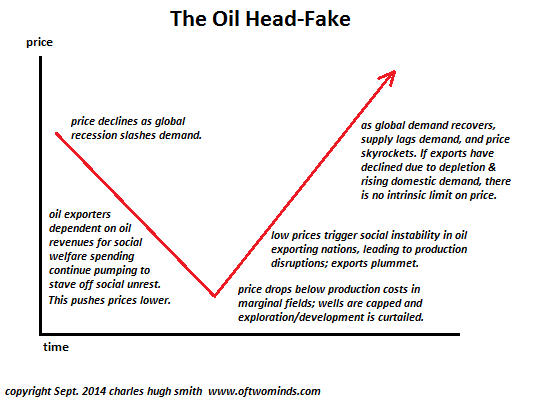

I've described the dynamic of structural imbalances of supply and demand leading to lower prices for crude oil as the Oil Head-Fake: high global production (supply) continues while demand declines due to global recession, and the resulting imbalance of supply and demand triggers a major decline in price. But this drop is not positive; it's a temporary response that triggers a variety of disruptive consequences.

There's nothing fancy about a basic supply-demand pricing model; if the world is awash in crude oil and demand slides, price will eventually follow.

The interesting parts of the Oil Head-Fake Dynamic arise from the supply side, not the demand side. Demand for oil is famously inelastic, meaning that easy substitutes are not readily available, and the primacy of oil in the global economy insures a steady demand.

Yes, natural gas can be substituted for vehicles that have been converted to burn natural gas, coal can be converted into liquid fuels, gasoline/diesel vehicles can be scrapped and replaced with electric vehicles--but all of these substitutes require reworking not just the vehicles but the entire infrastructure of extracting and delivering liquid fuels (or sufficient quantities of electricity) to substitute for oil.

Even with natural gas production soaring due to the fracking revolution (a rise in production many doubt is sustainable), there isn't enough natural gas being extracted to substitute for oil, except at the margins: the fuel being replaced with natural gas is coal.

While the Nazi war machine famously ran (at least partly) on liquified coal, fabricating enough plants to liquify coal in quantities large enough to substitute the new coal-based fuel for oil-derived fuels is non-trivial.

As for using electricity, all the electricity generated by alternative-energy sources such as solar and wind amount to a few percentage points of total energy consumption in the U.S. The percentage is higher in other nations (for example, Germany), but substituting alt-energy for oil-based fuels is not practical without massive, sustained capital investment in new energy production, delivery and distribution infrastructure.

Despite the relative inelasticity of oil demand, a significant percentage of oil consumption is discretionary: tourism is discretionary, and so are many single-passenger commutes. Keeping the lights on all night in empty buildings is discretionary. Some percentage of military training is discretionary. Driving every day to run one errand when all five errands per week could be accomplished in one trip is discretionary. Much of business travel is discretionary. Driving to a restaurant when a meal could be prepared at home is discretionary. Shopping for non-essentials is discretionary.

When jobs are lost and budgets are slashed, discretionary demand for oil craters.

The ebb and flow of discretionary demand is known as the business cycle of expansion and recession. Though the business cycle is considered the natural order of all economies, the current crop of Central Planners is convinced that their powers enable them to eliminate the business cycle, i.e. recessions are no longer a necessary feature of the credit cycle and everyone can enjoy permanent expansion of consumption, debt and risk.

History suggests the omnipotence of central banks is illusory, and their hubris will be rewarded with a recession that breaks the back of their interventions.

Even if you believe in the omnipotence of central banks, statistical reversion to the mean suggests recessions (declines in discretionary demand) have not been eliminated--they've just been pushed forward.

Several emerging features of the oil supply story complicate the supply-demand pricing model. In the classic model, as demand drops, price follows, and at some point it's no longer profitable for high-cost producers to continue pumping oil. As a result, they cap their wells, cease extracting oil, and eventually supply drops to match demand and price stabilizes.

When demand recovers, price follows, and marginal production is brought back on line to meet rising demand. Price stabilizes as supply rises to meet demand.

So far so good, but as noted above, oil is not a commodity that can be replaced with a substitute, except at the margins.

Oil has another peculiarity: it isn't distributed evenly around the world. Some nations-states have large reserves, others essentially none. Those with large reserves export some of their production to those with little or no oil.

Those nations with abundant oil often suffer from The Resource Curse:--due to the extraordinary wealth generated by their oil, the rest of their economy atrophies and their political/social structure is distorted by the oil wealth.

The atrophying of the non-oil economy and endemic corruption driven by oil wealth lead to societies and economies with few opportunities. The despots, monarchies and other Elites reaping the oil wealth keep a lid on this simmering social unrest with welfare. As their populations of non-Elites have exploded, the costs of placating the restive masses with social welfare have also exploded higher.

Domestic consumption of oil has also soared, along with population and as a result of subsidies that keep the cost of petrol absurdly low. What is nearly free is inevitably squandered, and with no price discipline, consumption has skyrocketed in oil exporting nations.

Another peculiarity is the easy-to-get oil was extracted first. This makes sense in terms of cost-benefit, and the inevitable result is the oil that's left is more difficult to extract and process. This means the cost of producing a barrel of oil has risen from $1/barrel in the good old days to $40 or more in many exporting nations.

Add in graft, waste, distribution costs, taxes to fund social welfare programs, etc., and the break-even price for oil exporters is much higher than the production costs alone.

This sets up a contradictory set of requirements for oil exporters: oil exporters can only maintain their social spending and keep the regime afloat if oil prices stay elevated. When global recession guts demand and the price of oil tumbles, the exporter regimes are at risk of collapse if they can't maintain social welfare spending.

The only way to offset lower prices is to pump more oil, which paradoxically pushes prices lower. This is a double-bind: if they cut production in the hopes that prices will stabilize, this enables their competitors to keep production high: prices won't decline. But if they pump more to compensate, prices also decline.

Higher production costs mean any serious price decline makes production unprofitable at a higher threshold. Where it might have taken a decline to $40/barrel to squeeze marginal producers out, now the threshold might be closer to $60/barrel.

This means even modest declines in price soon trigger production cuts as marginal wells are capped and exploration/development of costly reserves are put on hold.

But since the supergiant oil fields responsible for most of the global production are in exporting nations, the dynamic of maintaining social control and regime stability outweighs declines in marginal production.

This set up a price decline spiral as marginal production is taken offline but supply doesn't drop along with demand. The Resource Curse establishes a positive feedback loop: in the classic model, the feedback is negative: demand drops, price and supply follow, and price stabilizes as supply reaches equilibrium with demand.

But the Resource Curse is positive feedback: the lower price declines, the greater the need to compensate for lower revenues with higher production.

Meanwhile, the more price drops, the more marginal (costly) production is taken offline. This sets up the ideal conditions for a positive feedback on price: when demand recovers, supply will never be able to catch up.

It doesn't take much imagination to discern a tipping point in oil revenues: once price declines enough that social welfare programs cannot be funded, some exporting nation regimes will be toppled by domestic instability. Others may become vulnerable to external forces. The point here is that production generally suffers mightily when regimes collapse and the Status Quo is disrupted.

Another peculiarity is that as the easy-to-get oil is depleted, the need for financial and human capital investment soars. It requires billions of dollars and vast expertise to maintain production, and exporting nations have typically made the choice to devote their scarce capital to social welfare and feathering the beds of Elites rather than investing billions of dollars to maintain their production capacity.

Add these dynamics up and we get a supply chain that is vulnerable to price declines and depletion of the cheap, easy-to-get oil. If supply is disrupted on multiple fronts--social, economic, physical--it will be incapable or rising to meet recovering demand after the forest-fire of global recession clears out the deadwood.

This sets up a new pricing dynamic: demand rises but supply does not, and prices continue higher without respite or any intrinsic limit. As I have noted before, a motorcycle deliveryman in India or China will pay $10/gallon for fuel because he only needs a few liters to conduct his business. The energy/price threshold of the American household with two gas-guzzling vehicles is considerably less resilient and adaptive: below a high level of consumption, the household ceases to function, and above a relatively low price, the household also ceases to function.

The essence of the Oil Head-Fake Dynamic is the inevitable drop in oil price resulting from a sharp decline in demand (i.e. global recession) will trigger disruption of the global oil supply chain that will eventually push prices higher than most currently think possible.

Of related interest:

Are you like me? Ever since my first summer job decades ago, I've been chasing financial security. Not win-the-lottery, Bill Gates riches (although it would be nice!), but simply a feeling of financial control. I want my financial worries to if not disappear at least be manageable and comprehensible.

Are you like me? Ever since my first summer job decades ago, I've been chasing financial security. Not win-the-lottery, Bill Gates riches (although it would be nice!), but simply a feeling of financial control. I want my financial worries to if not disappear at least be manageable and comprehensible.And like most of you, the way I've moved toward my goal has always hinged not just on having a job but a career.

You don't have to be a financial blogger to know that "having a job" and "having a career" do not mean the same thing today as they did when I first started swinging a hammer for a paycheck.

Even the basic concept "getting a job" has changed so radically that jobs--getting and keeping them, and the perceived lack of them--is the number one financial topic among friends, family and for that matter, complete strangers.

So I sat down and wrote this book: Get a Job, Build a Real Career and Defy a Bewildering Economy.

It details everything I've verified about employment and the economy, and lays out an action plan to get you employed.

I am proud of this book. It is the culmination of both my practical work experiences and my financial analysis, and it is a useful, practical, and clarifying read.

Test drive the first section and see for yourself. Kindle, $9.95 print, $20

"I want to thank you for creating your book Get a Job, Build a Real Career and Defy a Bewildering Economy. It is rare to find a person with a mind like yours, who can take a holistic systems view of things without being captured by specific perspectives or agendas. Your contribution to humanity is much appreciated."

Laura Y.

Gordon Long and I discuss The New Nature of Work: Jobs, Occupations & Careers(25 minutes, YouTube)

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

| Thank you, Doug M. ($25), for your superbly generous contribution to this site-- I am greatly honored by your support and readership. |