Fake News, Mass Hysteria and Induced Insanity

The "fake news" is that we've never been healthier, healthcare costs are under control and our economy has fully "recovered."

We've heard a lot about "fake news" from those whose master narratives are threatened by alternative sources and analyses. We've heard less about the master narratives being threatened: the fomenting of mass hysteria, which turns the populace into an easily manipulated and managed herd, and induced insanity, a longer-term marketing-based narrative that causes the populace to ignore the self-destructive consequences of accepting the fad/ ideology/ mindset being pushed as "good" and "normal."

In terms of "fake news," it's hard to beat the mainstream media and its handlers' attempts to whip up mass hysteria via unsubstantiated claims that Russian hackers working for Putin deprived Hillary of the presidency. The campaign to spark mass hysteria was launched with great precision, unleashing the overwhelming forces of endless repetition (the marketer's favorite tool) and appeals to national security authorities: The C.I.A., F.B.I, and all the other security agencies purportedly concur that Russia "hacked" (whatever that means) the U.S. election.

The intent of the campaign was painfully obvious: by wheeling out the big guns of authority without any actual evidence, the campaign's designers hoped the public would automatically assume the bizarre, outlandish claim must be "true," even though no evidence was submitted to substantiate this fact-free claim, and respond as planned, i.e. willingly join a mass hysteria herd in favor of discrediting the U.S. election results.

Did the "hackers" change the election results issued by voting machines? Did they "hack" the election totals? Wouldn't there be tell-tale forensic evidence of such tampering? How else could "hackers" change the election other than by changing votes and vote totals?

Or was the media campaign to generate mass hysteria based on nothing but purposefully vague and unsubstantiated claims of Russia-inspired "fake news" that undermined the election by questioning the mainstream media's biased coverage of the presidential campaign?

"Fake news" is of course the staple of marketing products that end up killing the unwary consumers who buy the hype. The classic example is the cigarette/ tobacco industry, which ran adverts for decades proclaiming absurdities such as the health benefits of smoking (other than dying a horrible, needless death), the "fact" that doctors preferred one brand of cigarette over the other brands, and so on.

The industry famously went to truly monumental lengths to hide the facts about the destructive consequences of smoking from the public, and aggressively attacked any evidence that smoking was remarkably unhealthy as "unscientific," i.e. beating back the truth with The Big Lie.

That a form of consumption that killed the consumers was unquestionably accepted not just as "normal" but as cool/hip for decades illustrates the staying power of induced insanity. Mass hysteria eventually wears off, as it overloads the emotional circuitry of the target audience; humans soon become desensitized to the triggers used to generate mass hysteria, and it takes heavier and heavier doses of propaganda to maintain the feverishly herd-inducing hysteria.

Eventually, the populace habituates to the stimulus and becomes exhausted by the hysteria.

Induced Insanity, on the other hand, is not an emotional state--it is a state of mind and a state of perception that filters and interprets inputs to produce the desired output-- an acceptance of insanity as "normal" and "good."

For example, eating mountains of food that "tastes good" is positive and normal. Never mind that we're eating/consuming ourselves to death:

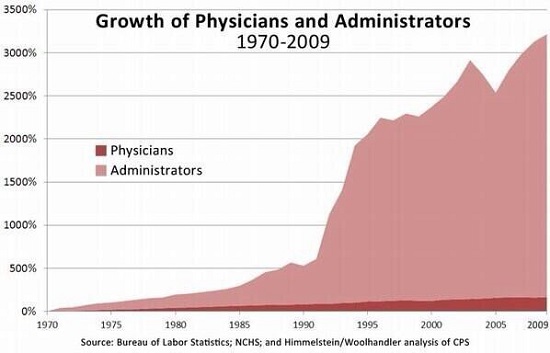

Or that our medical costs are so out of control that they're bankrupting households, enterprises and eventually,the entire economy:

Or that much of the money is spent on shuffling paperwork/ claims and counter-claims, complying with thousands of pages of regulations and dealing with the systemic fraud our system invites and rewards:

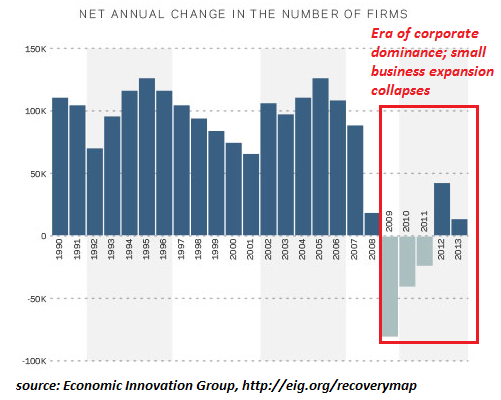

Induced insanity doesn't just describe our acceptance of ill health and a doomed healthcare system; it also describes our blind acceptance of an economy that's throttling small business:

The "fake news" is that we've never been healthier, healthcare costs are under control and our economy has fully "recovered." These sustained "fake news" campaigns are intended not to induce hysteria, but an enduring acceptance of what is visibly destructive and insane.

Food for thought as we enter 2017. Always start every inquiry with a simple question: cui bono--to whose benefit?

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com.

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com.

Check out both of my new books, Inequality and the Collapse of Privilege ($3.95 Kindle, $8.95 print) and Why Our Status Quo Failed and Is Beyond Reform ($3.95 Kindle, $8.95 print). For more, please visit the OTM essentials website.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Victor C. ($10/month), for your outrageously generous pledge to this site -- I am greatly honored by your support and readership.

|

Thank you, Eric J. ($5/month), for your superbly generous pledge to this site -- I am greatly honored by your support and readership.

|