When the "Fix" Increases Systemic Fragility, Things Fall Apart

All the "fixes" have fatally weakened the real economy, and created a dangerous illusion of "wealth," "growth" and solvency.

The "fix" of the last eight years worked, right? This was the status quo's "fix":

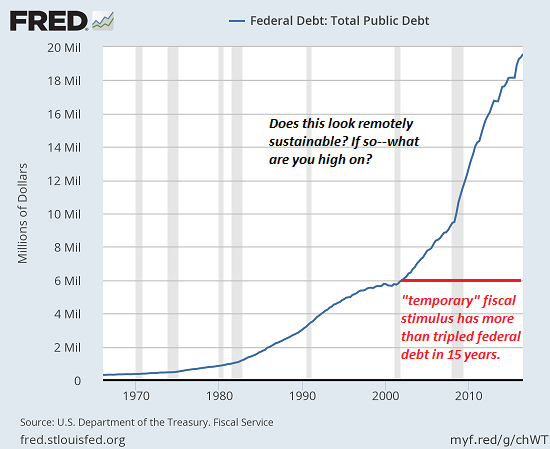

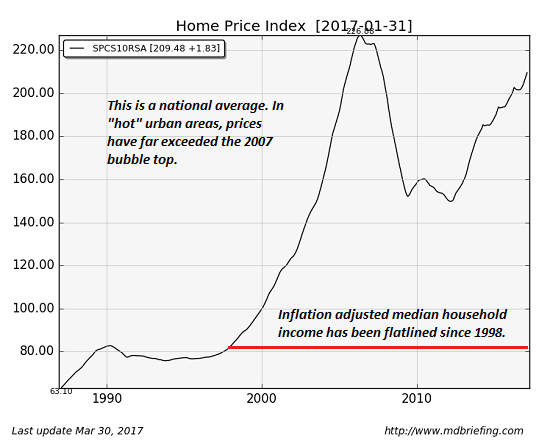

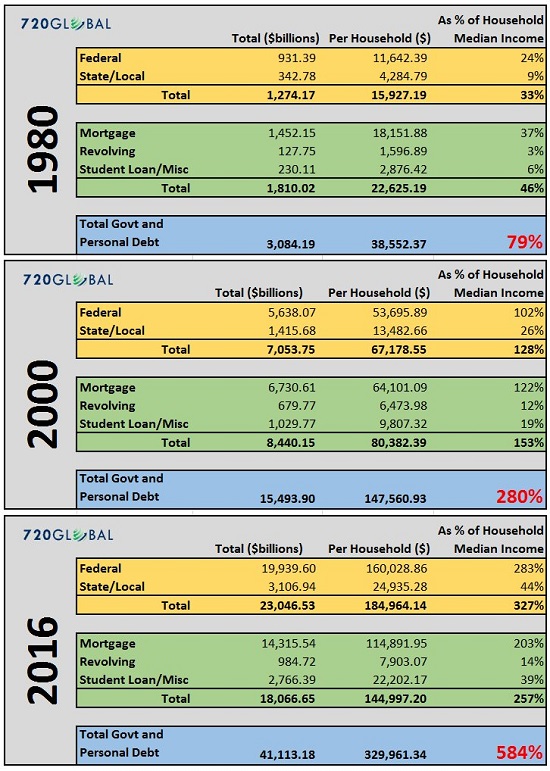

1. Massive expansion of debt: sovereign, household and corporate, all in service of a) bringing consumer demand forward b) fiscal stimulus funded by debt c) corporate stock buybacks to boost stock valuations d) asset bubbles in real estate, bonds, stocks, bat guano futures, etc.

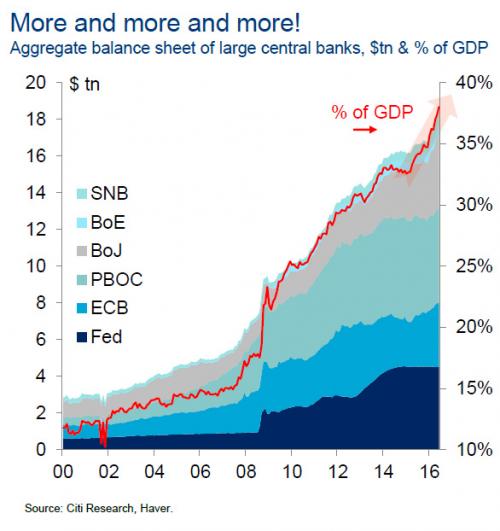

2. Monetary stimulus, i.e. creating and distributing money at the top of the wealth/power pyramid so corporations and the super-wealthy could buy more assets with free money for financiers issued by central banks.

3. Gaming statistics such as unemployment and metrics such as stock indices to generate the illusion of "growth," "stability" and "wealth."

4. Saying all the right things: the "recovery" is creating millions of jobs, inflation is low, virtue-signaling is more important than actual increases in inflation-adjusted wages, etc.

As Dave of the X22 Report and I discuss in Central Banks Weakened The Economy To The Point Of No Return, Day Of Reckoning Has Arrived (42 min. podcast), this "fix" has fatally weakened the real economy. The cost of maintaining the illusions of "growth," "stability," "wealth" and solvency is extremely high, and hidden from view: systemic fragility has increased to the point of brittleness.

What is fragility? Fragility is the result of an erosion of resilience, redundancy, adaptability, accountability, honesty, feedback and willingness to sacrifice today's consumption for tomorrow's productivity and systemic stability.

The status quo "fix" has gutted resilience, redundancy, adaptability, accountability, honesty, feedback and willingness to sacrifice today's consumption for tomorrow's productivity. Can anyone who isn't a lackey on the payroll of the Powers That Be provide any credible evidence that the U.S. economy is more resilient after eight years of debt-dependent "recovery"?

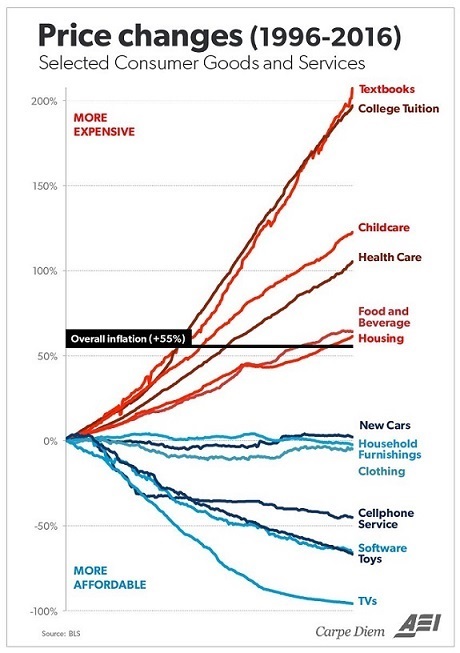

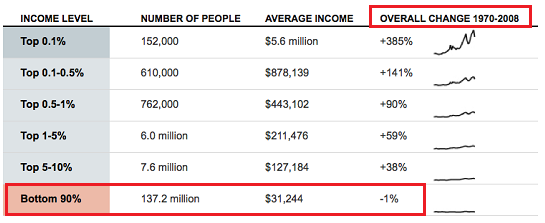

Sadly, we suffer from an oversupply of well-paid lackeys, factotums, apparatchiks, flunkies, media mouth-pieces and PR hacks and a severe scarcity of unbaised, unspun data points. What little data we do have tells us that the inflation-adjusted wages for the bottom 95% have declined during the "recovery" that made the wealthy much, much wealthier.

As for redundancy--redundancy reduces profits, as it increases costs, so redundancies have been as ruthlessly eliminated as human labor. The slightest disruption in global supply chains means production and transport of essentials collapses in a heap.

And how have the dominant state-protected cartels improved adaptability? They've stifled it at every turn. Higher education has jacked up prices for its overpriced marginal-utility "product," ditto the healthcare/Big Pharma cartels, the military-industrial cartel (hello overpriced, under-performing F-35 and LCS), the banking cartel (love those $35 fees and .01% interest paid on deposits), and all the other cartels that dominate our pay-to-play "democracy."

State-protected cartels and monopolies are the death of competition, transparency and adaptability--all essential dynamics in real solutions.

Accountability in the public/private-sector "swamp" is near-zero. A mumbled apology for malfeasance, a hand-slap fine for fraud, a bribe passed off as a "speech fee", revolving doors between government contractors and government agencies--accountability is non-existent at the top of the wealth-power pyramid, while a nickel-bag dealer gets a tenner (10-year gulag sentence) and the federal prosecutor gets a gold star. Meanwhile, the real criminals skim millions in ill-gotten embezzlements, frauds and cronyist skims are laughing all the way to their remote havens of wealth.

"Honesty" has lost all meaning in public dialog. Supposedly accurate statistics are rigged, and every public utterance is calculated to signal virtue (the acme of Orwellian doublespeak) or appeal to a constituency attuned to key words: utter the key words, and you're home free. Never mind the economy has been hollowed out: you've signaled your virtue and the moral superiority of the constituency.

Feedback has been reduced to a dollar sign. If you pony up millions in campaign contributions and lobbying, your feedback counts. All other feedback is discounted or ignored. Whistleblowers are prosecuted, any reform that threatens the status quo is watered down to meaninglessness, and anyone going public with truthiness is sent to bureaucratic Siberia.

As I explain in my book Why Our Status Quo Failed and Is Beyond Reform, all these fake-reforms only increase the systemic fragility by weakening all the dynamics that generate adaptability, accountability, feedback, transparency, etc.

The status quo is now like a wafer-thin sheet of ice over a deep lake of killing-cold water. To the naive and inexperienced, the ice looks solid; they believe the tall tales of "recovery," growth," "wealth" and solvency.

It's all phony public relations. As a strange as it may sound, PR doesn't make thin ice thick enough to stand on.

All the "fixes" have fatally weakened the real economy, and created a dangerous illusion of "wealth," "growth" and solvency.

Soaring debt and declining earnings = brittle thin ice.

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com.

Check out both of my new books, Inequality and the Collapse of Privilege ($3.95 Kindle, $8.95 print) and Why Our Status Quo Failed and Is Beyond Reform ($3.95 Kindle, $8.95 print, $5.95 audiobook) For more, please visit the OTM essentials website.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Lewis D. ($50), for your magnificently generous contribution to this site -- I am greatly honored by your steadfast support and readership.

|

Thank you, Patrick O'T. ($5/month), for your splendidly generous pledge to this site -- I am greatly honored by your support and readership.

|