Extremes Become More Extreme, Then Revert to the Mean

A fatal bout of runaway instability becomes inevitable when "extraordinary emergency measures" become permanently essential to keep the bubbles from popping.

A funny thing happens as policies intended to fill financial potholes transition from "temporary emergency measures" to "we need to keep doing this to stabilize the status quo": extremes get more extreme as what were once viewed as extraordinary policy measures required to keep the rickety system from collapsing become the "New Normal."

Of course the Federal Reserve continues suppressing interest and mortgage rates even after the financial crisis has passed, because if they stopped, the system would revert to crisis and collapse.

I've assembled a few charts of extremes becoming more extreme as a consequence of "emergency policies" becoming not just normalized but the keystone of the entire economy. What were desperate expediencies at first are now the lifeblood of the economy: withdraw them and the economy collapses in a heap.

I discussed these extremes in a podcast with Richard Bonugli (26 minutes), with the following charts providing context.

What's extraordinary is the systemic nature of the current extremes. New heights of precarity are being reached across the entire spectrum of the economy, not just in stock market bubbles but in the concentration of "wealth" in risk-on speculative assets--the very assets most prone to destabilization and reversion to the mean, the statistical dynamic in which outlier metrics eventually return to their starting point.

The causes of this reversion don't matter; after the fact, pinpointing the cause becomes a popular parlor game, but the reality is systems revert without any specific cause: suppressing instability with extreme policies creates a temporary illusion of stability, but the extreme policies actually increase instability.

Credit-asset bubbles are a manifestation of extremes generating an illusory euphoria of stability while beneath the surface, these extremes are ramping up instability to the point that sudden breakdown / collapse is the only possible outcome.

When the economy becomes dependent on ever more extreme financial trickery to maintain the illusion of stability, a death loop becomes normalized: as instability leaks through the extreme policies, then even more extreme measures are instituted, generally behind the scenes. Obscure methods of expanding liquidity are normalized, bank credit and other mechanisms (repos, etc.) are jacked up, all of which serve the goal of duct-taping the system to appear stable to unknowing eyes.

The problem with this financial fentanyl is that it's impossible to detect the lethality of the dose until it's too late. That's the current situation in American and global markets.

Let's go through a few of the many extremes flashing red warning signs of systemic precarity.

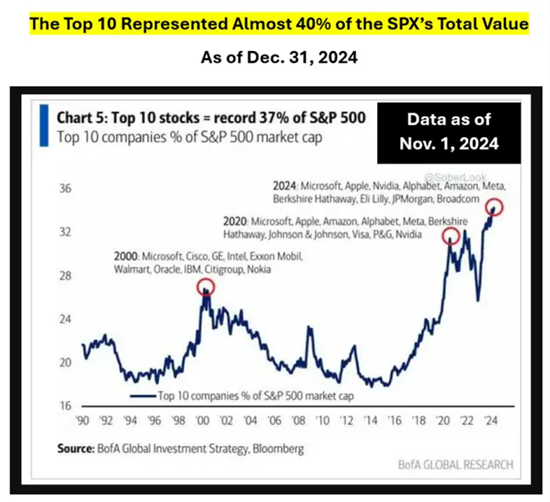

A handful of Big Tech stocks are holding up not just the S&P 500, but the entire global stock market. The Mag 7 (or top 10, it's basically the same) dominate the market capitalization of the entire S&P 500 to a dizzying degree. Everyone knows this extreme is not a sign of ruddy economic health, but they're forced to chase the mega-cap stocks lest they be fired for underperformance: another example of a death-loop feedback.

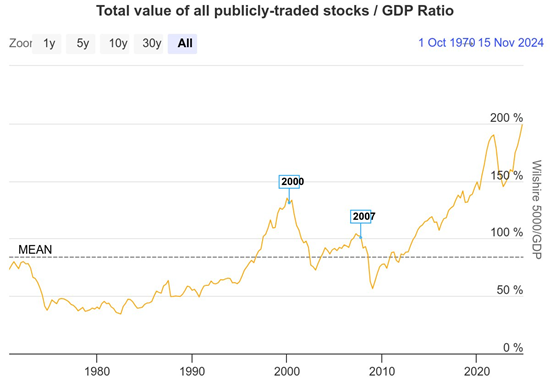

Stock valuations in relation to GDP have reached new extremes, with stocks being valued at more that 200% of the nation's GDP.

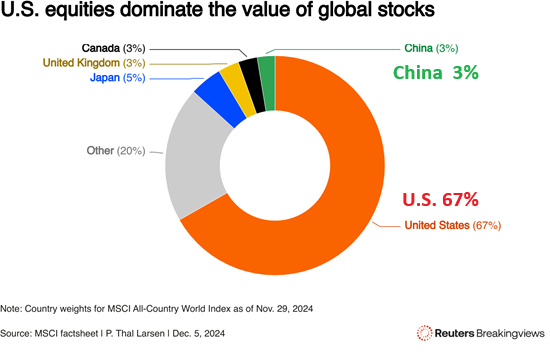

U.S. stocks--concentrated in a mere 7 stocks--are now 67% of the entire global stock market. For context, China's stock market has a 3% share of the global stock market, the American populace is about 4% of the global population, and America's GDP is 26% of the global GDP in nominal terms and around 15% when adjusted for PPP (purchase price parity).

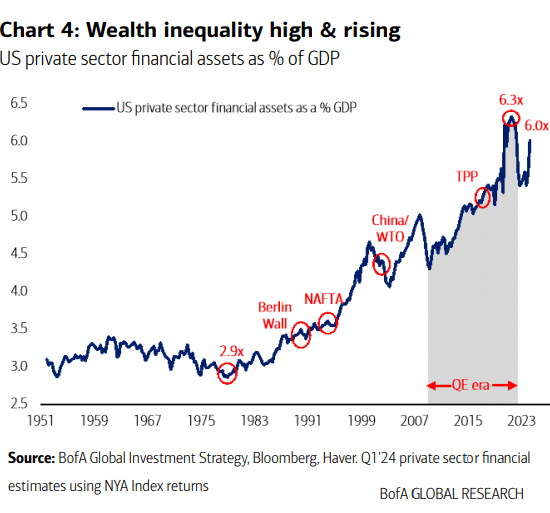

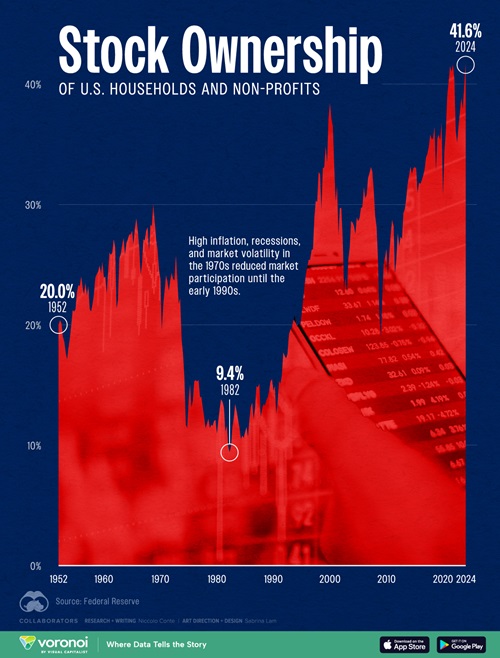

Since ownership of stocks and other financial assets is concentrated in the top 10%, the concentration of "wealth" in stocks has greatly increased wealth inequality. The ownership of stocks is not just concentrated in the top 10%, it's also a core asset of the Boomer generation. According to Jim Bianco of Bianco Research (@biancoresearch on X),

"The share of equities held by people who are at or near retirement age (55+) has climbed to about 80%, up from 60% two decades ago, according to an analysis of Federal Reserve data by Rosenberg Research. And Americans 70 and older now have an "astonishing" 30% share."

Other sources indicate that 52% of people aged 60-65 have 70% of their savings in stocks.

Stock ownership across the board has also reached historical extremes.

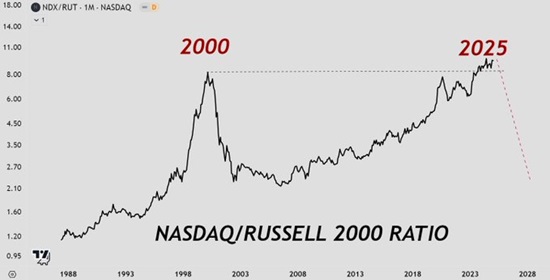

Given the extreme concentration of stock market gains in a handful of mega-cap tech companies, it's little wonder that the Nasdaq index has reached extremes of valuation compared to the the small-cap Russell 2000 index.

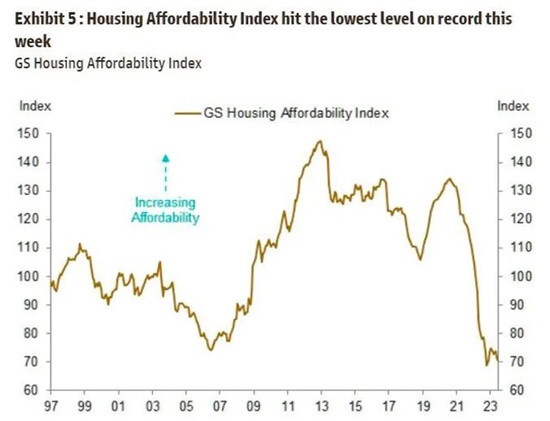

Lest we imagine that the extreme policy distortions that have been normalized to "stabilize the system" only manifest in the stock market, consider the extreme low of housing affordability. Lots of finger-pointing here, but few seem to notice that the Federal Reserve and the quasi-governmental mortgage agencies have effectively socialized the entire U.S. mortgage market. The only analog of such state control might be, well, um, Communist governments.

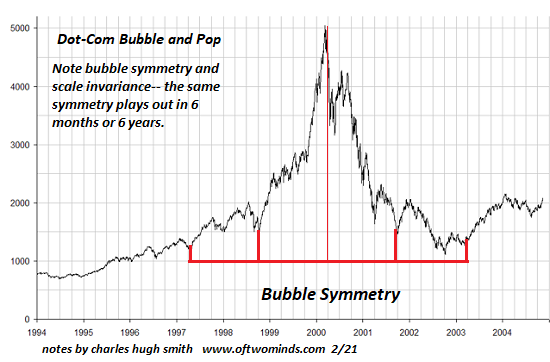

Here is how reversion to the mean worked in 2000 to 2003: The Nasdaq stock index fell 80% in 2.5 years. I can assure you that very few observers in March 2000 thought such a mean reversion was possible, much less inevitable, and the few Cassandras who warned of this were dismissed as losers who'd missed out on the greatest expansion of "wealth" in history.

Yes, well, "wealth" is also a funny thing, if you measure it solely by bubbles inflated with financial fentanyl: a fatal bout of runaway instability becomes inevitable when "extraordinary emergency measures" become permanently essential to keep the bubbles from popping.

New podcast:

Charles Hugh Smith on the Extremes in the U.S. Economy and Markets. (26 min)

My recent books:

Disclosure: As an Amazon Associate I earn from qualifying purchases originated via links to Amazon products on this site.

The Mythology of Progress, Anti-Progress and a Mythology for the 21st Century print $18, (Kindle $8.95, Hardcover $24 (215 pages, 2024) Read the Introduction and first chapter for free (PDF)

Self-Reliance in the 21st Century print $18, (Kindle $8.95, audiobook $13.08 (96 pages, 2022) Read the first chapter for free (PDF)

The Asian Heroine Who Seduced Me (Novel) print $10.95, Kindle $6.95 Read an excerpt for free (PDF)

When You Can't Go On: Burnout, Reckoning and Renewal $18 print, $8.95 Kindle ebook; audiobook Read the first section for free (PDF)

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States (Kindle $9.95, print $24, audiobook) Read Chapter One for free (PDF).

A Hacker's Teleology: Sharing the Wealth of Our Shrinking Planet (Kindle $8.95, print $20, audiobook $17.46) Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $5, print $10, audiobook) Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake (Novel) $4.95 Kindle, $10.95 print); read the first chapters for free (PDF)

Money and Work Unchained $6.95 Kindle, $15 print) Read the first section for free

Become a $3/month patron of my work via patreon.com.

Subscribe to my Substack for free

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

|

Thank you, David S. ($200), for your beyond-outrageously generous subscription to this site -- I am greatly honored by your steadfast support and readership. |

Thank you, Chris H. ($200), for your beyond-outrageously generous subscription to this site -- I am greatly honored by your steadfast support and readership. |

|

|

Thank you, Harvey D. ($100), for your outrageously generous subscription to this site -- I am greatly honored by your steadfast support and readership. |

Thank you, David ($70), for your splendidly generous subscription to this site -- I am greatly honored by your support and readership. |