How Housing Bubble #2 Bursts

Corporate / private equity / STVR investors are all fair-weather owners of housing.

Let's indulge in some basic logic:

1. All credit-asset bubbles burst.

2. U.S. housing is a credit-asset bubble.

3. The U.S. housing bubble will burst.

The only variables are how and when Housing Bubble #2 will burst. That's today's topic.

I've been writing about housing since 2005, as Housing Bubble #1 was inflating. I've participated in / observed housing rising sharply in the late 1970s and the late 1980s, followed by deflation / stagnation. Housing Bubble #1--circa 2003-2008--was characterized by all the classic signs of a mania:

1. Participants denied it was a bubble. When greed displaces prudence, this isn't a bubble doomed to pop, it's the New Normal.

2. Fraud, malfeasance, misrepresentation, speculation and leverage were all rampant. In the euphoric ascent to ever higher valuations, why let foolish little things like income, risk management and credit ratings stand in the way of reaping more profits?

Housing Bubble #2 has rolled over into the decline phase, but this is discounted by the consensus which holds that higher mortgage rates dented the market; once they drop a bit, housing will resume its ascent to ever-higher valuations.

I see a different set of dynamics in play:

1. The 40+ year cycle of interest rates / bond yields has turned. Rates will not go back to zero and stay flatlined for years. Risk and inflationary forces have changed and are not returning to The Great Moderation.

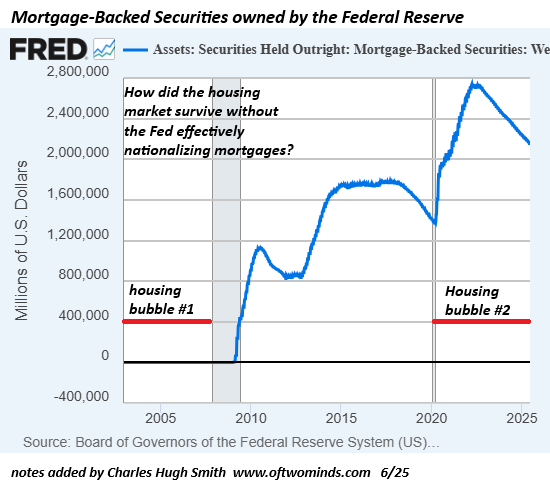

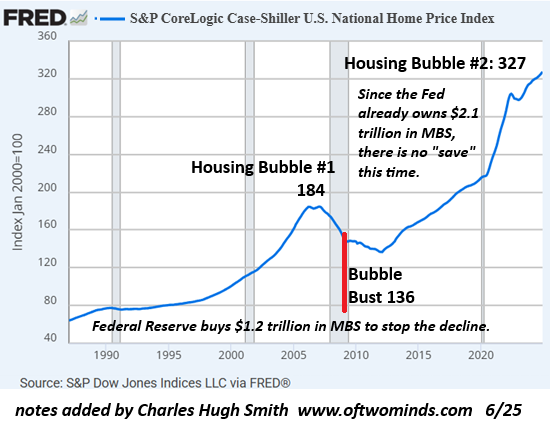

2. The Federal Reserve / federal government effectively nationalized the mortgage industry post-2009 Global Financial Meltdown as the means to stop the decline of housing valuations and re-inflate them via super-low mortgage rates. The Fed bought a staggering $1.2 trillion of mortgage-backed securities in 2009-2010, up from zero--a monumental manipulation of the mortgage market that soon exceeded $1.6 trillion.

How the housing/mortgage market managed to survive without Fed nationalization prior to 2009 remains a mystery.

For its part, the federal government effectively nationalized the quasi-governmental mortgage agencies (Fannie Mae, Freddy Mac), using these agencies to guarantee most mortgages in the U.S.

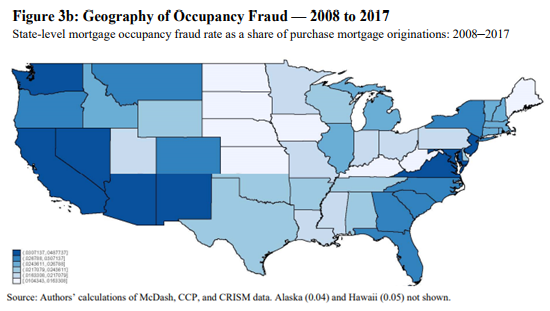

3. The incentive (lower mortgage rates) to commit fraud by claiming to be an owner-occupant rather than an investor has pushed mortgage fraud to levels that Federal Reserve researchers declare "rampant."

Owner-Occupancy Fraud and Mortgage Performance (A 46-page PDF report is available on this link.)

The study's authors found that "in most years, fraudulent investors make up roughly one-third of the total pool of investors." Fraud rates in excess of 13% were found in some states states.

The frenzy to buy and convert houses to short-term vacation rentals (STVRs) took off in the post-pandemic "revenge travel" boom. Corporate purchases of houses as rental properties had taken off in the post-2009 era of mass foreclosures, a trend that accelerated as private equity sought new markets to exploit.

Combine corporate / private-equity buyers with small investors flooding into STVRs and the post-pandemic panic-buying frenzy, and it's little wonder that investors--declared and fraudulent, large and small--now own huge swaths of housing in the U.S.:

Investors Bought 26% of the Country's Most Affordable Homes in the Fourth Quarter--the Highest Share on Record

An estimated 26% of Fort Worth's single family homes are owned by companies, city says

(Yes, family trusts and households can own housing as LLCs, but the study linked above paid no attention to the type of ownership; it paid attention to A) if the owners have multiple first liens, and B) whether they moved following the origination of their new purchase mortgage or not.)

4. The risks created by this preponderance of investor ownership are high. The Federal Reserve researchers found that fraudulent investors pose a much higher risk of default than declared investors and real owner-occupants.

As "revenge travel" shrivels up, property taxes and insurance rise and inflation ravages household budgets, STVRs are quickly shifting from income-producing assets to loss-generating liabilities. Investors either sell before they're under-water or the risk of default rises accordingly.

Professionally managed corporate and private-equity owners will start unloading properties as rents sag and vacancies rise. STVR owners who realize the tide has reversed will also rush to sell before the price slide gathers momentum.

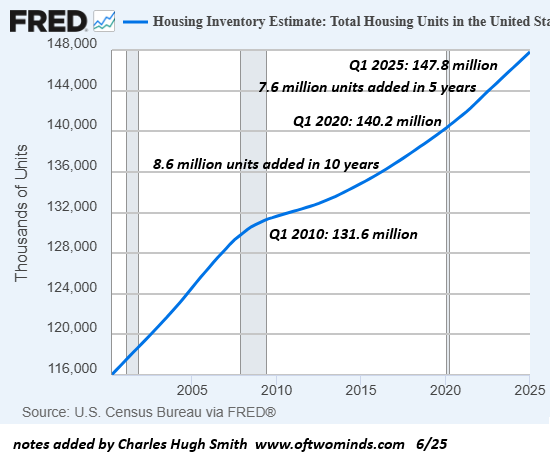

Let's look at some charts for context. Here is a chart of total housing units. Confounding the conventional narrative of a "housing shortage," the U.S. added 7.6 million housing units in the five years 2020-2025, a rate far higher than the 8.6 million units added over 10 years 2010-2020.

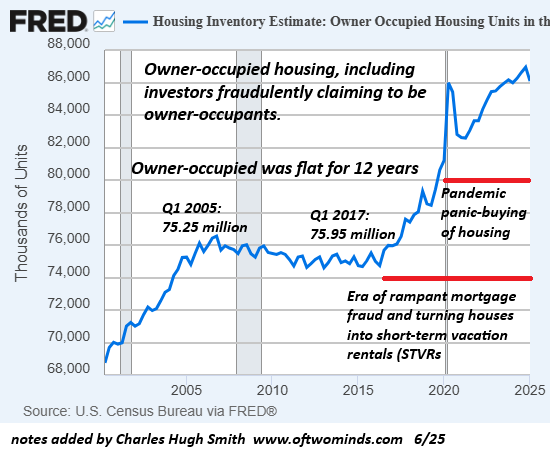

Here is a chart of owner-occupied housing. Note that the number of owner-occupied homes was flatlined for 12 years--from 2005 to 2016. Then it suddenly leaps up by 10 million in a few years--from 76 million to 86 million. Did 10 million households all win the lottery, or is the bulk of this astounding increase the result of fraudulent investors posing as owner-occupant buyers?

This map shows the extent of investor mortgage -fraud.

This chart of Federal Reserve ownership of mortgage-backed securities (MBS) overlays neatly with each leap higher in valuations. Pump "free money" into the financial system and keep rates at historic lows, and voila, you can inflate a bubble for the ages.

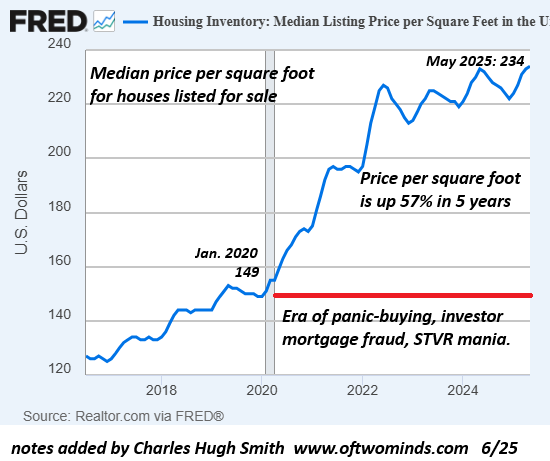

The post-pandemic buying frenzy pushed the cost per square foot of houses listed for sale up 57%.

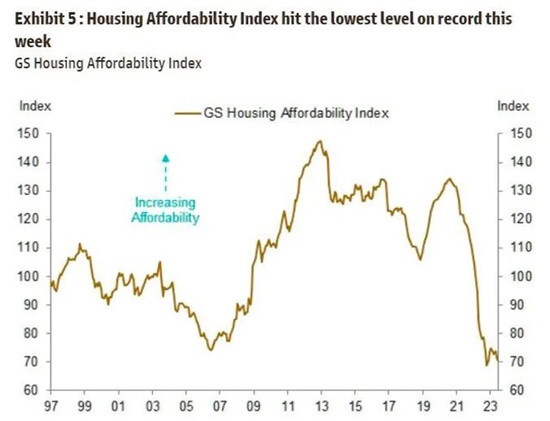

Unsurprisingly, this bubble pushed housing affordability to record lows.

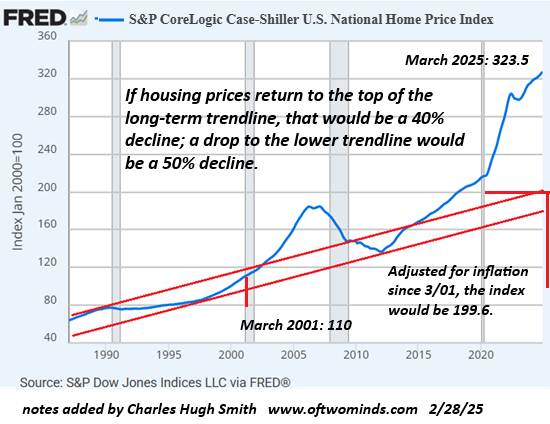

The Case-Shiller Index offers a long-term view of how far valuations could drop once the bubble bursts. A 40% decline would be the norm, and a 50% drop would be well within the typical range of bubbles bursting.

The Fed's mass manipulation of mortgage rates in 2010 "saved" Bubble #1 from playing out in a free-market manner, but the Fed won't be able to engineer an equivalent "save" this time around, as the mortgage market has already been nationalized and the Fed already owns a stupendous $2.1 trillion of MBS.

Corporate / private equity / STVR investors are all fair-weather owners of housing. Once the profits shrink or reverse into losses, investors push the "sell" button. And since housing is priced on the margins, it only takes a handful of get-me-out sales to push valuations down 10%, then 20%, then 30% and eventually to a bottom between 40% anf 50%.

This vulnerability to the collapse of valuations is the bitter fruit of the Fed's manipulation of rates and mortgages over the past 16 years. We love a "free market" when rapidly expanding credit inflates a bubble, but oh dearie-dearie me, we have to stop the "free market" from operating if it bursts the bubble.

Here's how Housing Bubble #2 bursts: buyers of overvalued, money-losing properties vanish, those who waited too long sink underwater (sales prices are lower than what they paid), marginal investors default, owner-occupants who lose their jobs sell or default, private equity realizes their losses will only increase the longer they hold off selling, and the momentum of sellers far outnumbering buyers cascades.

Greed is replaced by fear, and then by the realization it's too late to exit without losses. This is how bubbles burst.

Of related interest:

Paradise Lost (Melody Wright)

My recent books:

Disclosure: As an Amazon Associate I earn from qualifying purchases originated via links to Amazon products on this site.

The Mythology of Progress, Anti-Progress and a Mythology for the 21st Century print $18, (Kindle $8.95, Hardcover $24 (215 pages, 2024) Read the Introduction and first chapter for free (PDF)

Self-Reliance in the 21st Century print $18, (Kindle $8.95, audiobook $13.08 (96 pages, 2022) Read the first chapter for free (PDF)

The Asian Heroine Who Seduced Me (Novel) print $10.95, Kindle $6.95 Read an excerpt for free (PDF)

When You Can't Go On: Burnout, Reckoning and Renewal $18 print, $8.95 Kindle ebook; audiobook Read the first section for free (PDF)

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States (Kindle $9.95, print $24, audiobook) Read Chapter One for free (PDF).

A Hacker's Teleology: Sharing the Wealth of Our Shrinking Planet (Kindle $8.95, print $20, audiobook $17.46) Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $5, print $10, audiobook) Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake (Novel) $4.95 Kindle, $10.95 print); read the first chapters for free (PDF)

Money and Work Unchained $6.95 Kindle, $15 print) Read the first section for free

Become a $3/month patron of my work via patreon.com.

Subscribe to my Substack for free

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Buck V. ($100), for your outrageously generous subscription to this site -- I am greatly honored by your steadfast support and readership. |

Thank you, Richard C. ($7/month), for your marvelously generous subscription to this site -- I am greatly honored by your support and readership. |

|

|

Thank you, Royce M. ($150), for your beyond-outrageously generous subscription to this site -- I am greatly honored by your steadfast support and readership. |

Thank you, Elijah M.A. ($7/month), for your splendidly generous subscription to this site -- I am greatly honored by your support and readership. |