Illiquid, Overvalued

As "dip buyers" get eviscerated, more dominos fall, and at a tipping point, the herd realizes the tide has reversed and it's time to sell--but alas, it's too late.

Illiquid, Overvalued describes a great many assets that are on the books as "rock-solid investments." Illiquidity means there are few if any buyers for the asset being offered for sale, and this can arise from various conditions.

1. Credit is tight and expensive, limiting the pool of potential buyers to those with cash.

2. Nobody wants the assets because they're grossly overvalued.

3. The pool of buyers with the expertise and financial backing needed to buy the asset is inherently limited.

4. "Animal spirits" have left the room and buyers are "on strike" due to caution / fear of future losses.

Bill Ackman outlined some useful principles of illiquidity in

a recent commentary on X in his discussion of the illiquid nature of many assets held by Ivy league university endowment funds:

"Harvard's endowment is principally invested in illiquid private assets including real estate, private equity, and venture capital funds.

Real estate and private equity funds are highly levered so relatively small changes in asset values can have a large impact on equity values. For example, if a real estate fund's asset values decline by 15% and the assets are levered 60%, the fund's equity value will decline by 37.5%.

The increase in cap rates and interest rates have impaired real estate and private equity asset values. These funds do not generally mark to market as public assets are marked leading to a wide disparity between public values and private values when overall values decline.

Venture funds generally mark their assets to the last round valuation so these marks can also be overstated as these values can become stale.

I believe that a substantial part of the reason why many private assets remain private despite the stock market near all time highs is that the public market will value private assets at lower values than they are being carried at privately."

In other words, assets held privately can be "marked to fantasy" because they're not exposed to the market's appraisal of their liquidity and value, which are two sides of one coin: if nobody has the cash and willingness to buy the asset, its value is essentially zero, regardless of its "book value."

When Alan Greenspan issued his mea culpa in late 2013 about missing the subprime mortgage implosion and the resulting Global Financial Meltdown (Why I Didn't See the Crisis Coming Foreign Affairs), he identified two sources of his failure to "see it coming":

1. He assumed markets would remain liquid, i.e. that a buyer would emerge for every seller

2. The total failure of everyone's sophisticated models to predict the collapse of confidence.

The core failure lay in the models' reliance on the notion that humans make decisions rationally as Homo economicus, when the reality is we are extremely prone to irrational exuberance (a.k.a. running with the euphorically greedy herd) and panic (running off the cliff with the herd). He invoked Keynes famous "animal spirits" as the missing variable in economic models.

Irrational "animal spirits" generate "tail risk," events that supposedly happen only rarely but when they do happen, they trigger outsized consequences, and the Fed's models failed to accurately account for "tail risk" because they happen more often than statistical models predict.

All this boils down to illiquidity caused by a panic-button urgency to sell and a profound reluctance to buy: When "animal spirits" are confident in ever-higher asset valuations, participants place a constant bid under the market because prices will keep going up so I'll make more money. This constant bid is called liquidity: cash is flowing into the asset class, be it stocks or housing or cryptocurrencies or commodities.

When "animal spirits" turn to panic, sellers rush to sell as buyers vanish as they fear that prices will keep going down so I'll lose more money. Buying into a downtrend is known as "catching the falling knife": the initial "buy the dip" players have their heads handed to them on a platter, and those on the sidelines decide not to try to catch the falling knife.

This is an illiquid market: the bid keeps dropping until buyers are willing to gamble that "this is the bottom." But should asset prices continue sliding after an initial euphoric pop higher--"the bottom is in, buy!"--then those who held back find their caution reinforced: that wasn't the bottom after all, and everyone who jumped in lost money.

As every surge of "buy the dip" players loses, the market goes bidless--everyone who wanted to play "catch the falling knife" has been burned, and those who have lost the "animal spirits" to gamble stay out. Bids (offers to buy) dry up and asset prices crash to levels no one in the greed-euphoria stage could imagine were even remotely possible.

Those who follow liquidity assume that the more cash sloshing around the system, the more money will flow into assets. But this assumes participants are rational and prices are "fair value". When panic takes hold of the herd, no matter how much cash is sloshing around, none of it will be gambled on a losing bet.

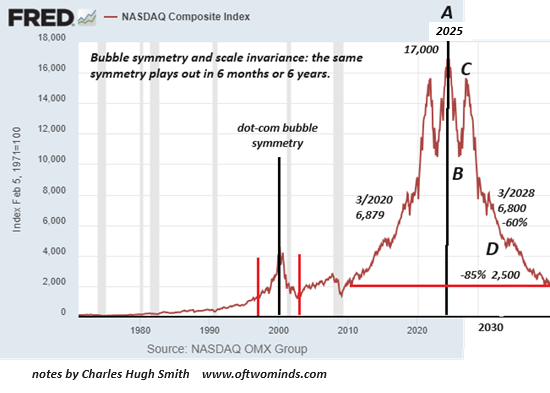

Take a look at this chart of the Nasdaq dot-com bubble, and note the bubble symmetry: what shot up soon plummeted back to pre-bubble levels. Stocks that had reached $60 per share were recommended as "buys" at $45--a rational play perhaps, but wildly off the mark, as the stock eventually bottomed at $4.

When sellers desperate to sell swamp buyers, prices decline. If bids dry up, prices crash.

There is a domino-like effect to euphoria /liquidity turning to caution and then to panic / illiquidity. When overvalued illiquid private assets are sold at huge discounts, this topples the first domino of caution in professional money managers, who then move to sell the overvalued assets on their books to credulous "retail" investors and overseas buyers.

As "dip buyers" get eviscerated, more dominos fall, and at a tipping point, the herd realizes the tide has reversed and it's time to sell--but alas, it's too late.

The Federal Reserve can pump billions of dollars of credit "liquidity" into the financial system, but if nobody wants to "catch the falling knife," the credit will just sit there untouched, as everyone who was dumb enough to borrow money and gamble it away--leaving the debt still to pay--has already been wiped out.

Illiquid and overvalued: two sides of the same coin.

Check out my new book Ultra-Processed Life and my new fiction/novels page.

Become

a $3/month patron of my work via patreon.com.

Subscribe to my Substack for free

My recent books:

Disclosure: As an Amazon Associate I earn from qualifying purchases originated via links to Amazon products on this site.

Ultra-Processed Life print $16, (Kindle $7.95, Hardcover $20 (129 pages, 2025) Read the Introduction and first chapter for free (PDF)

The Mythology of Progress, Anti-Progress and a Mythology for the 21st Century print $16, (Kindle $6.95, Hardcover $24 (215 pages, 2024) Read the Introduction and first chapter for free (PDF)

Self-Reliance in the 21st Century print $15, (Kindle $6.95, audiobook $13.08 (96 pages, 2022) Read the first chapter for free (PDF)

When You Can't Go On: Burnout, Reckoning and Renewal $15 print, $6.95 Kindle ebook; audiobook Read the first section for free (PDF)

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States (Kindle $6.95, print $16, audiobook) Read Chapter One for free (PDF).

A Hacker's Teleology: Sharing the Wealth of Our Shrinking Planet (Kindle $6.95, print $15, audiobook $17.46) Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $3.95, print $12, audiobook) Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake (Novel) $3.95 Kindle, $12 print); read the first chapters for free (PDF)

Money and Work Unchained $6.95 Kindle, $15 print) Read the first section for free

Become a $3/month patron of my work via patreon.com.

Subscribe to my Substack for free

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

|

Thank you, James M. ($70), for your exceedingly generous subscription to this site -- I am greatly honored by your support and readership. |

Thank you, Dan T. ($5/month), for your marvelously generous subscription to this site -- I am greatly honored by your support and readership. |

|

|

Thank you, Christopher H. ($50), for your superbly generous subscription to this site -- I am greatly honored by your support and readership. |

Thank you, John C. ($32), for your splendidly generous subscription to this site -- I am greatly honored by your support and readership. |