Is This the Last Bubble?

The consensus holds there will be another bubble after the Everything Bubble pops, but this might be misplaced confidence in the godlike powers of central banks.

The consensus holds that central banks--the Federal Reserve in the US--will gradually inflate away the world's rising debt burden while propping up assets and the economy with the usual bag of monetary magic: suppress interest rates so debt service costs ease, increase the money supply and credit to prop up asset bubbles in stocks and housing, and thereby generate growth in consumption via the elixir of "the wealth effect:" as assets loft higher, everyone feels richer and so they borrow and spend more.

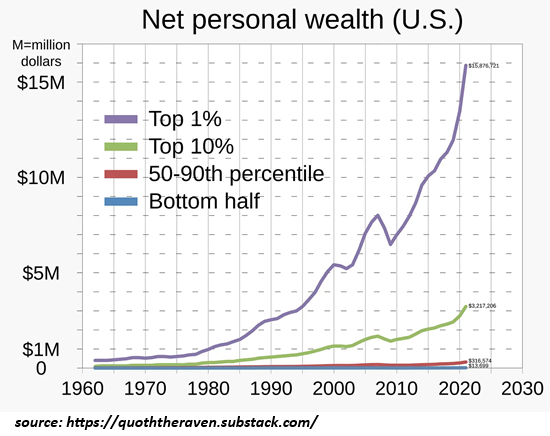

Well, not everyone, because only the top 10% own enough assets to feel "the wealth effect," but since they account for 50% of all consumer spending, that's enough to maintain the status quo, in which the bottom 90% lose ground (especially the bottom 60%) and the top 10% are doing splendidly.

Should the bubble du jour pop, no worries, central banks will rush to the rescue as they have for 25 years, goosing money supply and credit, opening the floodgates of liquidity, pushing interest rates down so everyone and every entity can borrow and spend / speculate more, more, more.

This is a nice story, and proponents have the past 25 years of history to back it up. But beneath the surface appeal of this story--a Hollywood ending every time, as the Fed will inflate another bubble, one after the other in an endless loop--there are stirrings in the deep that suggest the Everything Bubble is the last bubble of its kind, and attempts to inflate another bubble when this one pops will collapse the entire rickety contraption.

In other words, everything is forever until it is no more. Let's consider some points that speak to the nature of speculative bubbles.

1. Speculative bubbles don't require central banks increasing money supply and manipulating interest rates. Recency bias leads us to imagine that central bank policies inflate and pop speculative bubbles via monetary levers, but the colossal South Seas Bubble in 1720 that popped with such devastating consequences arose and fell in the pre-central bank era. The madness of crowds--or more specifically,

the greed-driven madness of greedy crowds is the core driver of speculative frenzies / bubbles.

2. Confidence is the foundation of speculative frenzies. Yes, confidence, as in a con. Back in 1720, the South Seas Company was supported by the establishment, and so confidence was high that it was a can't lose proposition. The riches skimmed by early investors encouraged this confidence.

Today, confidence that the Fed will rush to the rescue should the Everything Bubble pop is high, as is the confidence that the AI Bubble isn't a bubble because AI is going to change everything and that transformation will be immensely profitable--if not for the gold miners, then for those selling the miners picks and shovels.

3. Quasi-religious fervor, confidence, staggering gains and speculative frenzies all meld into one overflowing river, sweeping all before it. The primary force here is the belief that this isn't irrational, or speculative--it's all based on solid facts. That this was the exact same belief that powered bubbles in 1720, 1925-1929, 1998-2000 and 2004-2008 is brushed aside, for as we all know, this time it's different. Of course it is, but perhaps not in the way that the consensus anticipates.

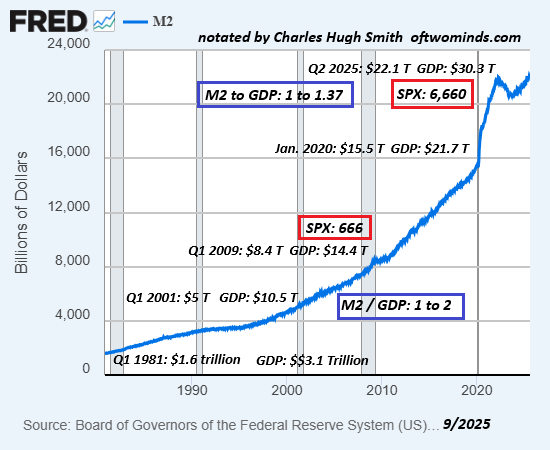

Just as a break from all the fun and games, let's consider a chart of M2 money supply, generally conceded as the driver of stocks rising, and compare it to GDP--a measure of economic expansion--and the S&P 500 stock index (SPX).

It's interesting to note the ratio of M2 and GDP. That money supply and economic expansion would rise together qualifies as common sense, but what makes this interesting is the slippage in the ratio.

For two decades, GDP was roughly double M2. In 1981, M2 was $1.6 trillion and GDP was $3.1 trillion. In 2001, M2 was $5 trillion and GDP was $10.5 trillion. So far so good.

In Q1 2009, at the bottom of the stock market crash / Global Financial Crisis, there was bit of slippage: M2 was $8.4 trillion and GDP was $14.4 trillion--no longer 1 to 2.

By the pre-Covid high watermark of Q1 2020, M2 was $15.5 trillion and GDP was $21.7 trillion. After the Covid crash and stimulus, here in Q2 2025 M2 is $22.1 trillion and GDP is $30.3 trillion-- 1 to 1.37.

There's a phrase that describes this: diminishing returns. Goosing money supply is no longer goosing GDP to the same degree it once did.

Meanwhile, back in Speculative Frenzy-Land, the SPX is up 10X, from the biblical low in Q1 2009 of 666 to today's high of 6660 (well, 6656, but close enough).

This suggests that the means of boosting GDP is now inflating bubbles, not actual economic activity. This is supported by the chart of money velocity, which is a measure of economic transactions across time. It's generally conceded that money velocity increases in good times and decays in not-to-good times. Here we see that money velocity has fallen off a cliff and never recovered the glory days of widespread, organically expanding economic activity.

It is not coincidental that the peak of money velocity in the mid-1990s Internet boom aligns with the peak of wage growth and the bottom 50%'s share of financial net worth. Simply put, the 1990s were the last era of widespread prosperity of the sort that actually "trickled down" to the bottom 90%. This was also the last era in which housing was broadly affordable to households with average incomes.

Saying that money velocity is an indicator of economic catastrophe doesn't go over well in polite company, but there it is. Somebody barfed in the punchbowl, sorry about that.

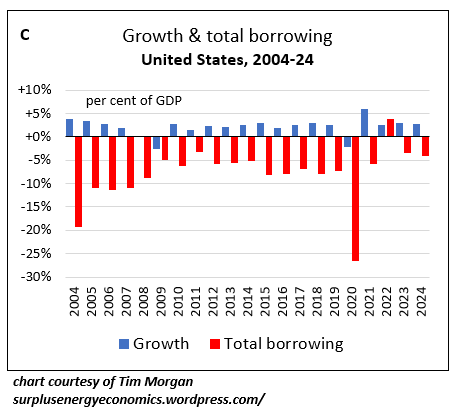

Lastly, consider this chart of debt and growth in the US, courtesy of Tim Morgan of the invaluable analytic site Surplus Energy Economics. Note that the blue indicators of growth are considerably smaller than the red indicators of debt.

Put all this together and it's clear that stock market and housing bubbles are the only sources of "growth," which is another way of saying that "growth" is a chimera masking the second-order effect of goosing money supply, credit, debt and speculative asset bubbles: extremes of wealth and income inequality as the top 10%'s wealth, income and spending have soared while the bottom 90% have fallen behind.

Consider the possibility that the AI Bubble is a close match for the 1720 South Seas Bubble, a bubble that sucked in the smart money (Sir Isaac Newton) and dumb money alike, and then collapsed in spectacular fashion wiping out true believers, gamblers, Wise Men and the credulous--everyone who participated other than those who sold early and stayed out as the bubble inflated to giddy heights. Due to the limitations of Wetware 1.0, the number of people who can manage to do that is so small that it's signal noise.

The consensus holds there will be another bubble after the AI Bubble / Everything Bubble pops, but this might be misplaced confidence in the godlike powers of central banks. If the Fed just gooses money supply, credit and crushes interest rates, the next bubble might be in the 2028 equivalent of Pet Rocks or Beanie Babies, it won't matter. There will always be another bubble because the Fed wills it to be so.

Or perhaps the limits of this serial bubble-blowing have already been reached, and this is the last, final bubble before the reckoning where the banquet of consequences has been set and Nemesis is catering what's served.

Check out my new book Ultra-Processed Life and my updated Books and Films.

Become

a $3/month patron of my work via patreon.com

Subscribe to my Substack for free

My recent books:

Disclosure: As an Amazon Associate I earn from qualifying purchases originated via links to Amazon products on this site.

Ultra-Processed Life print $16, (Kindle $7.95, Hardcover $20 (129 pages, 2025) audiobook Read the Introduction and first chapter for free (PDF)

The Mythology of Progress, Anti-Progress and a Mythology for the 21st Century print $16, (Kindle $6.95, audiobook, Hardcover $24 (215 pages, 2024) Read the Introduction and first chapter for free (PDF)

Self-Reliance in the 21st Century print $15, (Kindle $6.95, audiobook $13.08 (96 pages, 2022) Read the first chapter for free (PDF)

When You Can't Go On: Burnout, Reckoning and Renewal $15 print, $6.95 Kindle ebook; audiobook Read the first section for free (PDF)

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States (Kindle $6.95, print $16, audiobook) Read Chapter One for free (PDF).

A Hacker's Teleology: Sharing the Wealth of Our Shrinking Planet (Kindle $6.95, print $15, audiobook $17.46) Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $3.95, print $12, audiobook) Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake (Novel) $3.95 Kindle, $12 print); read the first chapters for free (PDF)

Money and Work Unchained $6.95 Kindle, $15 print) Read the first section for free

Become a $3/month patron of my work via patreon.com.

Subscribe to my Substack for free

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

|

Thank you, J.N. ($100), for your outrageously generous subscription to this site -- I am greatly honored by your steadfast support and readership. |

Thank you, Richard S. ($70), for your marvelously generous subscription to this site -- I am greatly honored by your steadfast support and readership. |

|

|

Thank you, Tiina ($7/month), for your superbly generous subscription to this site -- I am greatly honored by your support and readership. |

Thank you, David J. ($70), for your splendidly generous subscription to this site -- I am greatly honored by your support and readership. |