Once the Bubbles Pop, We're Broke

I hate to break it to you, but the everything bubble isn't permanent.

OK, I get it--the Bull Market in stocks is permanent. Bulls will be chortling in 2030 that skeptics have been wrong for 22 years--an entire generation. Bonds will also be higher, thanks to negative interest rates, and housing will still be climbing higher, too. Household net worth will be measured in the gazillions.

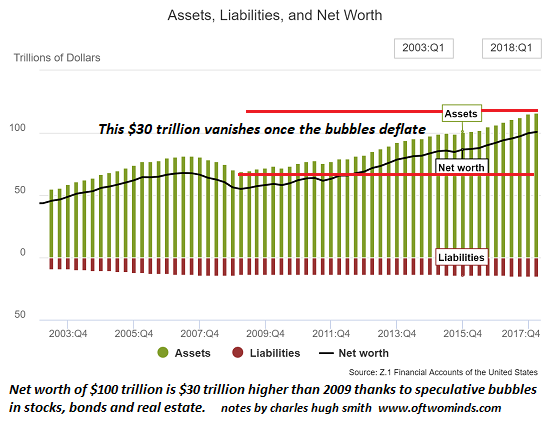

Here's the Fed's measure of current household net worth: a cool $100 trillion, about 750% of disposable personal income (DPI):

Household net worth has soared $30 trillion in the past decade of permanent monetary and fiscal stimulus. No wonder everyone is saying Universal Basic Income (UBI)-- $1,000 a month for every adult, no questions asked--is affordable, along with Medicare For All (never mind that Medicare is far more expensive than the healthcare provided by other advanced nations due to rampant profiteering, fraud and paperwork costs--we can afford it!)

And we get to keep the Endless Wars (tm), trillion-dollar white elephant F-35 program, and all the other goodies--we can afford it all because we're rich!

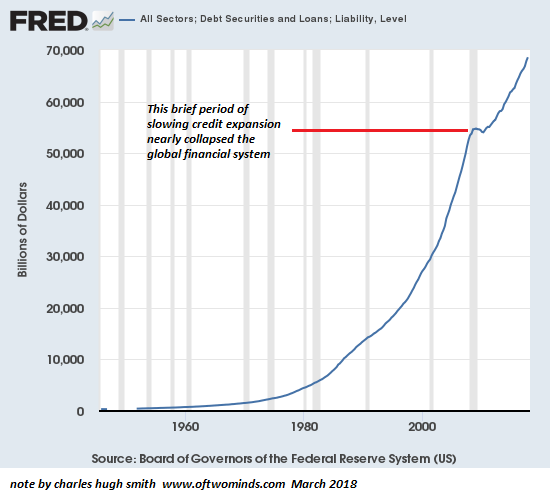

We're only rich until the bubbles pop, which they will. All speculative bubbles deflate, even those that are presumed permanent, And when the current everything bubble pops, net worth--and all the taxes generated by bubble-era capital gains--vanish.

Take a look at the Federal Reserve's Household Balance Sheet (June 2018):

$34.6 trillion in non-financial assets

$81.7 trillion in financial assets

$15.6 trillion in total liabilities ($10 trillion of which is home mortgages)

$100 trillion in net worth

$34.6 trillion in non-financial assets

$81.7 trillion in financial assets

$15.6 trillion in total liabilities ($10 trillion of which is home mortgages)

$100 trillion in net worth

So $25 trillion is in real estate. When the housing bubble pops, $10 trillion will go poof. Maybe $12 trillion, but why quibble about a lousy $2 trillion? We're rich!

Consumer durables are worth $5.7 trillion, minus consumer debt of $3.8 trillion. As we know from the 2008-09 recession, the value of used boats, BBQ grills and assorted other gew-gaws drops to near zero (boats abandoned to avoid slip fees, etc.), so shave off the phantom $2 trillion in consumer durables.

Stocks held directly and indirectly, $28 trillion. Stocks are overvalued by half, so once reality sets in $14 trillion will vanish into thin air.

Non-corporate businesses currently worth $11.9 trillion--in the depths of a recession, many will close and the market value of the struggling survivors won't be much. Let's say $5 trillion vanishes.

That's $30 trillion up in smoke, and we haven't even gotten to pensions and $15 trillion in "other financial assets." Whatever they are, we can bet that $10 trillion in pension entitlements and "other financial assets" disappear, too.

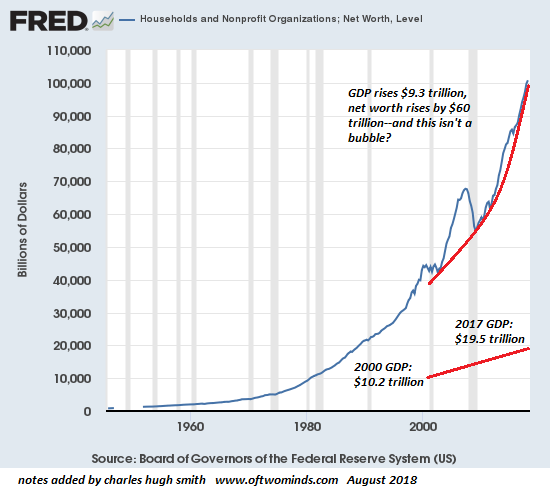

So a reasonable estimate is post-bubble, household net worth drops by 40%, or $40 trillion. This is actually being generous, as this leaves a $20 trillion gain since 2000, a period in which GDP rose from $10.2 trillion to $19.5 trillion:

I hate to break it to you, but the everything bubble isn't permanent. Extend this geometric line of net worth a decade and then extend the GDP line a decade; at that point, our wonderful assets will be worth $1,000 trillion while our real-world economy will have grown to $25 trillion. Does history suggest this is possible, or likely? Will the pundits still be declaring that this is all quite reasonable considering how well the economy is doing?

We're only rich until the bubble pops--then we're broke.

Back to School Book Sale: 57% off the Kindle edition and 25% off the print edition of The Nearly Free University and the Emerging Economy ($2.99 Kindle, $15 print)

My new book Money and Work Unchained is now $6.95 for the Kindle ebook and $15 for the print edition.

My new book Money and Work Unchained is now $6.95 for the Kindle ebook and $15 for the print edition.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

Thank you, Mike G. ($100), for your outrageously generous contribution to this site -- I am greatly honored by your steadfast support and readership.

|

Thank you, Mitch S. ($65), for your superbly generous contribution to this site -- I am greatly honored by your steadfast support and readership.

|