Lessons from the Unraveling of the Roman Empire: Simplification, Localization

The fragmentation, simplification and localization of the post-Imperial era offers us lessons we ignore at our peril.

There is an entire industry devoted to "why the Roman Empire collapsed," but the post-collapse era may be offer us higher value lessons. The post-collapse era, long written off as The Dark Ages, is better understood as a period of adaptation to changing conditions, specifically, the relocalization and simplification of the economy and governance.

As historian Chris Wickham has explained in his books

Medieval Europe and

The Inheritance of Rome: Illuminating the Dark Ages 400-1000, the medieval era is best understood as a complex process of social, political and economic natural selection: while the Western Roman Empire unraveled, the Eastern Roman Empire (Byzantium) continued on for almost 1,000 years after the fall of the Western Roman Empire, and the social and political structures of the Western Roman Empire influenced Europe for hundreds of years.

In broad-brush, the Roman Empire was a highly centralized, tightly bound system that was remarkably adaptive despite its enormous size and the slow pace of transport and communication. Roman society was both highly hierarchical--the elites claimed superiority and worked hard to master the necessary tools of authority-- slaves were integral to the building and maintenance of Rome's vast infrastructure--and open to meritocracy, as the Roman Army and other classes were open to advancement by anyone in the sprawling empire: every free person became a Roman Citizen once their territory was absorbed into the Empire.

When the Empire fell apart, the model of centralized control/power continued on in the reigns of the so-called Barbarian kingdoms (Goths, Vandals, etc.) and Charlemagne (768-814), over 300 years after the fall of Rome. (When the Ottomans finally conquered Constantinople in 1453, they also adopted many of the bureaucratic structures of the Byzantine Empire.)

Over time, however, the feudal model of localized fiefdoms nominally loyal to a weak central monarchy replaced the centralized model of governance. This adaptation fit the highly fragmented nature of European societies in this era.

But centralized influence never went away. The Christian churches based in Rome and Constantinople continued to exert centralized influence in politically fragmented regions, and monarchies continued to exist, in various states of strength and weakness. The Holy Roman Empire--as Voltaire is reputed to have observed, "neither Holy, Roman or an Empire"--had an enormously complex history in Germany and the rest of Europe. The monarchies in England and France remained in place, and the city-states of northern Italy wielded influence via trade and shifting alliances.

In other words, the Medieval era was ultimately a complex competition between overlapping models of governance and sharing resources, a competition between centralized and localized (what Wickham calls "cellular") nodes of power and the various ways that rulers and those they ruled dealt with each other.

Throughout the era, the legitimacy of rulers ultimately flowed from public assemblies, a tradition inherited from Rome that manifested in aristocratic courts and the church's leadership (bishops, etc.) and eventually, in parliaments. This tension played out in the sharing of costs and resources and the general direction of the state.

As a general rule, when monarchs consolidated too much power, they engaged in catastrophically costly and doomed wars (The Hundred Years War) because they were able to override or ignore the cautious counsel of elite assemblies.

Understood as a selective process of adapting to changing circumstances, this history offers us valuable lessons and templates for our future.

Once the centralized power of Rome fragmented, economic, social and political power simplified and relocalized. Trade volume shrank and trade routes vanished. Once the bureaucratic and military structures dictated by Rome collapsed, regions and localities were on their own.

Elites naturally sought out the best means to consolidate and expand their power, and residents (as a general rule, the peasantry and town-dwellers) sought to improve their own lives by reducing costs and securing access to resources.

The immense geographic, cultural, social and economic diversity of Europe was in effect freed to play out. This diversity is still evident; the European Union may have unified the European financial system, but cultural and social divisions have not dissolved.

Wickham distinguishes between two primary sources of income and wealth accessible to elites and governments: land and taxes. Collecting taxes requires an immense bureaucracy to identify and assess property owners, tenant farmers, merchants, collect duties on trade flows, etc. Taxes are the only reliable way to fund professional armies and the stupendous bureaucracy required to manage a complex centralized empire. The Byzantine Empire survived multiple rivals, invasions, etc. largely due to its competent tax collection bureaucracy, and European monarchies could only fund long, costly wars once they established tax collection bureaucracies.

Wealth from land--surplus skimmed from the labor of peasants--was adequate to fund highly localized nobility (many of which had one or two castles and a small fiefdom), but it wasn't reliable enough or large enough to support professional armies or vast centralized states.

How does this history offer a template for the next 20 years?

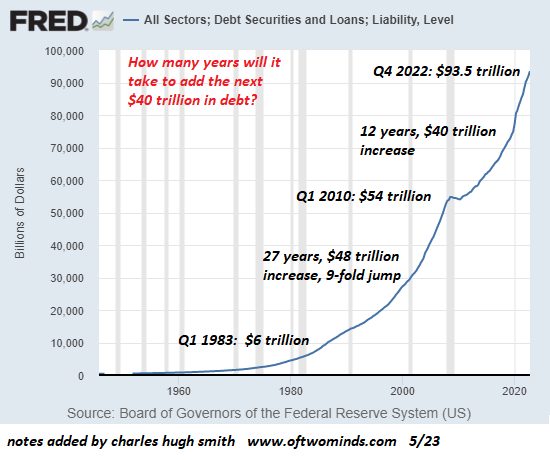

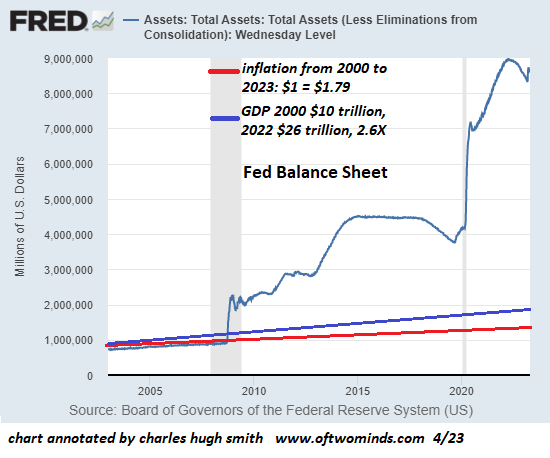

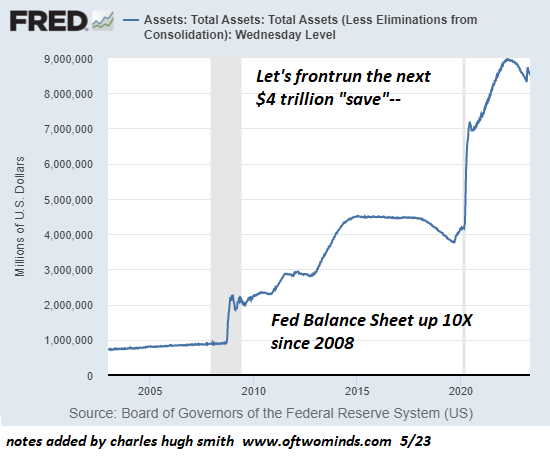

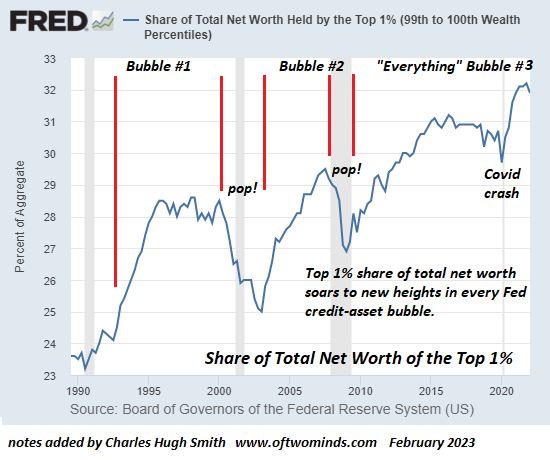

I have long held that the dominant global forces binding the global economy are globalization and financialization. Both have greatly increased the income and wealth that nation-states can tax to fund their vast structures: military, social welfare, and bureaucracies of management, regulation and control.

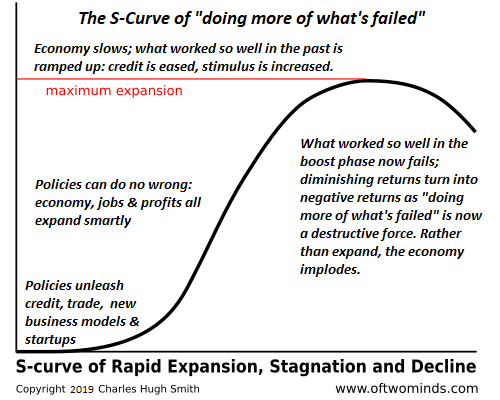

I have also held that globalization and financialization became hyper-structures prone to over-extension and the diminishing returns of the S-Curve. (see chart below) Both have reversed and are now in decline, a decline that I anticipate will accelerate unpredictably and rapidly as each dynamic is centralized and tightly bound, meaning each subsystem is highly interconnected with other subsystems. Should one break, the entire system unravels.

Globalization may appear to be decentralized, but the vast majority of global trade and capital flows through a few centralized nodes, and many aspects of trade depend on a very small number of routes and suppliers. This makes global trade exquisitely sensitive to disruption should any critical supplier or node fail.

Financialization is equally centralized and tightly bound, to the absurd degree that obscure financial structures (reverse repos, etc.) can trigger cascading crises in the real-world economy.

I anticipate a global simplification of trade and finance as fragile hyper-structures collapse as the failure of subsystems cascade through the entire system.

These systems have greatly accelerated extremes of wealth-income inequality by their very nature, and these vast distortions and imbalances are unsustainable. Also unsustainable is the immense expansion of the plundering of the planet's remaining resources via globalization and financialization. These dynamics will collapse under their own weight.

What will be left? Once the income and wealth that supported enormously costly nation-state governments contracts, central governments will no longer be able to fund their gargantuan systems. (States that attempt to fund their activities by printing money will only speed the collapse of their finances and thus their coherence.)

As in the post-Roman era, central authority may well continue, but its actual power and influence will be greatly reduced. Without expanding income and wealth to tax, the central state may attempt to extract most of the nation's surplus, but this stripmining of elites and commoners alike will trigger pushback and revolt.

A more sustainable response would be to offload most of the central government's financial burdens onto states, provinces, counties, etc., in effect pushing the impossible task of maintaining entitlements and promised spending on local entities.

Given the diversity of cultures, social values and economic dynamics in large nations and regions, we can anticipate a flowering of adaptations to these greatly reduced means. Some localities will favor increasing authoritarian controls, others will favor reducing authoritarian controls and ceding authority to the smallest units of public assembly.

Locales (shall we call them fiefdoms?) will divide naturally along geographic boundaries, just as fiefdoms in medieval Europe fell into natural boundaries shaped by rivers, valleys, mountain ranges, etc., and along economic and cultural borders.

This relocalization may manifest in the well-known forecasts of the US breaking into multiple regional states, or it might manifest as I suggest in a much-weakened but still influential central government ceding power to local political structures which may themselves fragment or form alliances with nearby entities with whom they share cultural and economic ties.

In other words, a churn of evolutionary adaptations can be expected. Just as there was no one post-Roman adaptation that worked equally well everywhere, we can expect there to be some adaptations of roughly equal success and many that are unsuccessful.

As individuals and households, we want to be located in successful adaptations that share our values and offer us agency, i.e. a say in public assemblies and the freedom to move and work as we see fit.

As I have outlined many times in the blog and in my books, locales that are highly dependent on long global supply chains and distant capital for their essentials will fare very poorly once those supply chains break and the capital dries up. Regions and locales that generate their own essentials (food, energy, metals, concrete, electronics, etc.), talent and capital are much more likely to generate enough resources to satisfy both local elites and the public.

As I explain in my book

Self-Reliance, we who have lived in the past 75 years of expanding production and consumption of Everything have lost touch with both the natural world that sustains us and the social and practical skills needed to endure and prosper in an era in which the engines of centralized power and wealth (globalization and financialization) decay and collapse.

Some locales will choose to foster relocalization and individual agency. Others will cling on to failing models of authoritarian control and globalization / financialization.

Ironically, perhaps, the most successful regions will be prone to indulging in hubris and denial, just as the Roman elites, basking in their centuries of dominance, dismissed the "Barbarians" and clung to their delusions of grandeur even as their world fragmented around them.

Those locales left behind by globalization and financialization may well offer much better opportunities for successful adaptation, relocalization and individual / household agency.

It is human nature to find reasons to dismiss the storm clouds on the horizon. We look around and find solace in the apparent strength of our institutions and economy, while ignoring their sobering dependence on unsustainable hyper-globalization and hyper-financialization.

The fragmentation, simplification and localization of the post-Imperial era offers us lessons we ignore at our peril.

It's important to view these lessons not just as an academic abstraction but as a guide to your own decisions about what places are most conducive to your security and well-being. Not every locale will do equally well, and the culture of many places may not be a great match for your own values and goals. If you decide to move, sooner is better than later.

This essay was drawn from my Weekly Musings Reports sent exclusively to subscribers, patrons and Substack subscribers. Thank you very much for supporting my work.

My new book is now available at a 10% discount ($8.95 ebook, $18 print):

Self-Reliance in the 21st Century.

My new book is now available at a 10% discount ($8.95 ebook, $18 print):

Self-Reliance in the 21st Century.

Read the first chapter for free (PDF)

Read excerpts of all three chapters

Podcast with Richard Bonugli: Self Reliance in the 21st Century (43 min)

My recent books:

The Asian Heroine Who Seduced Me

(Novel) print $10.95,

Kindle $6.95

Read an excerpt for free (PDF)

When You Can't Go On: Burnout, Reckoning and Renewal

$18 print, $8.95 Kindle ebook;

audiobook

Read the first section for free (PDF)

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States

(Kindle $9.95, print $24, audiobook)

Read Chapter One for free (PDF).

A Hacker's Teleology: Sharing the Wealth of Our Shrinking Planet

(Kindle $8.95, print $20,

audiobook $17.46)

Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $5, print $10, audiobook)

Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake (Novel)

$4.95 Kindle, $10.95 print);

read the first chapters

for free (PDF)

Money and Work Unchained $6.95 Kindle, $15 print)

Read the first section for free

Become

a $1/month patron of my work via patreon.com.

Subscribe to my Substack for free

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Max J. ($5/month), for your marvelously generous pledge to this site -- I am greatly honored by your steadfast support and readership. |

Thank you, Robert S. ($10.80), for your most generous contribution to this site -- I am greatly honored by your support and readership. |