The Systemic Risk No One Sees

The unraveling of social cohesion has consequences. Once social cohesion unravels, the

nation unravels.

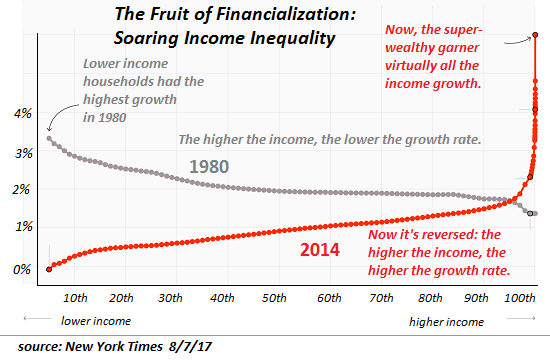

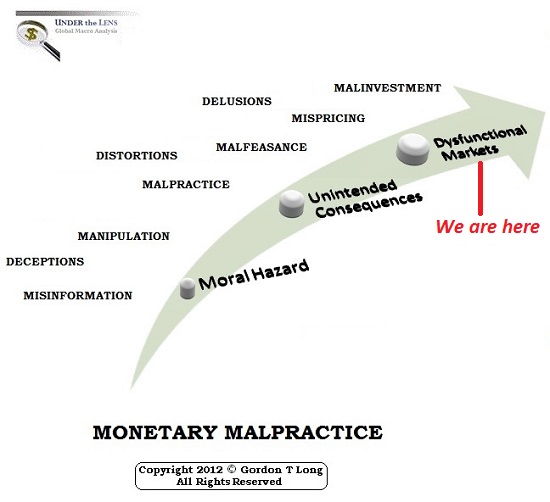

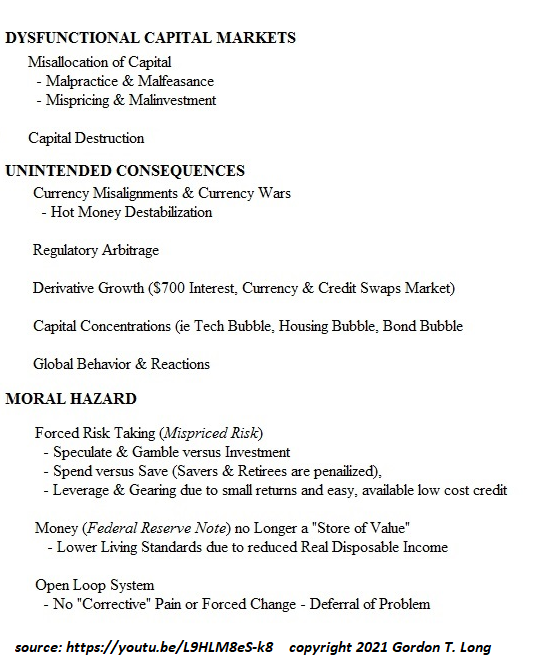

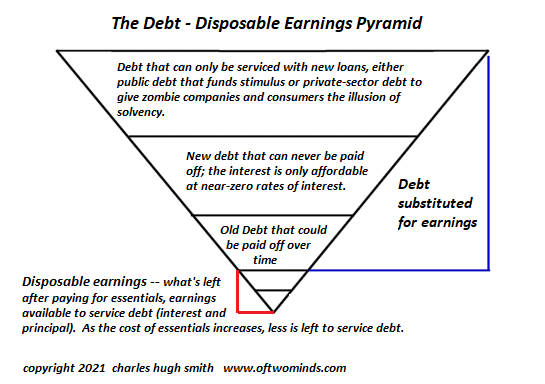

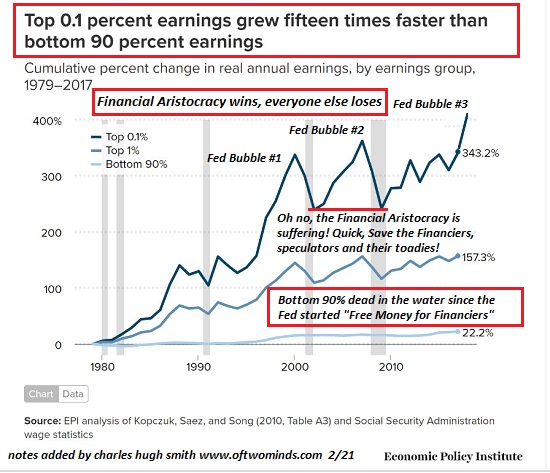

My recent posts have focused on the systemic financial risks created by Federal Reserve policies

that have elevated moral hazard (risks can be taken without consequence) and speculation to

levels so extreme that they threaten the stability of the entire financial system.

These risks are well known, though largely ignored in the current speculative frenzy.

But there is another systemic risk which few if any see: the collapse of social cohesion.

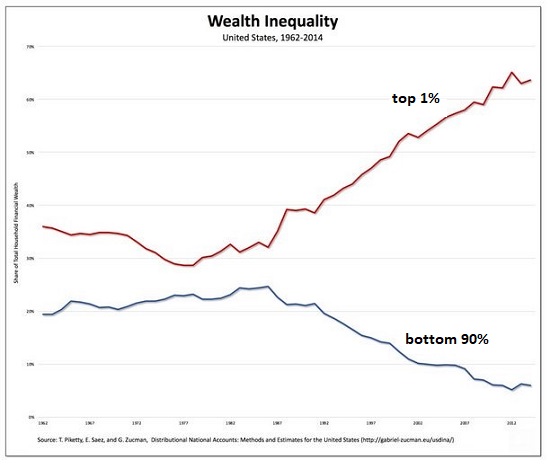

President Carter was prescient in his understanding that a nation's greatest strength is its

social cohesion, a cohesion that America's unprecedented wealth / income / power inequalities

has undermined. Consider this excerpt from his 1981 Farewell Address:

"Our common vision of a free and just society is our greatest source of cohesion at home and

strength abroad, greater even than the bounty of our material blessings."

In other words, a nation's strength flows not just from its material wealth but from its

social cohesion--a term for something that is intangible but very real, something that doesn't

lend itself to quantification or tidy definitions.

Here is my definition: Social cohesion is the glue binding the social order; it is the

willingness of the citizenry to sacrifice individual gains for the common good.

Social cohesion is the result of the citizenry sharing a common purpose and identity

and working toward the common good even at personal cost. Social cohesion arises from a

national identity based on shared values and sacrifices.

To maintain social cohesion, opportunities to better their circumstances must be open to all

(the social contract of social mobility) and sacrifices must be shared by the entire citizenry. If the privileged

elites evade their share of sacrifice, social cohesion is lost and the entire social order unravels.

The glue binding the privileged elites to shared sacrifice is civic virtue, a moral code

that demands elites devote a greater share of their own resources to the public good

in exchange for their political and financial power.

Though no one dares confess this publicly, America is now a moral cesspool. As a result,

the moral legitimacy of the nation’s leadership has been lost. Every nook and cranny

of institutionalized America is dominated by self-interest, and much of the economy is

controlled by profiteering monopolies and cartels which wield far more political power

than the citizenry.

Civic virtue has been lost. What remains is elite self-interest masquerading as civic virtue.

In his Farewell Address, President Carter explained that "The national interest is not always

the sum of all our single or special interests. We are all Americans together, and we must

not forget that the common good is our common interest and our individual responsibility."

Social cohesion, civic virtue and moral legitimacy are the foundation of every society,

but they are especially important in composite states.

America is a composite state, composed of individuals holding a wide range of regional,

ethnic, religious and class-based identities. The national identity is only one ingredient

in a bubbling stew of local, state and regional identities, ethnic, cultural and religious

identities, educational/alumni, professional and tradecraft identities, and elusive but

consequential class-based identities.

Composite states are intrinsically trickier to rule, as there is no ethnic or cultural identity

that unifies the populace. Lacking a national identity that supersedes all other identities,

composite states must tread carefully to avoid fracturing into competing regional, ethnic

or cultural identities.

Composite states must establish a purpose-based identity that is understood to demand shared

sacrifice, especially in crisis. In the U.S., the national purpose has been redefined by the

needs of the era, but never straying too far from these core unifying goals: defending the

civil liberties of the citizenry from state interference, defending the nation from external

aggressors, and serving the common good by limiting the power of special interests and

privileged elites.

We've failed to limit the power of privileged elites, failed to demand greater sacrifices

of the wealthy in exchange for power, and so the moral legitimacy of the regime has been lost.

And with the ascendance of self-interest and the elite's abandonment of sacrifice,

social cohesion has been lost.

This loss is reflected in the bitter partisanship, the increasingly Orwellian attempts to

control the mainstream and social media narratives, the debauchery of "expertise" as

dueling "experts" vie for control, the fraying of social discourse, the substitution of

virtue-signaling for actual civic virtue, the institutionalization of white-collar crime

(collusion, fraud, embezzlement, etc.), the increasing reliance on Bread and Circuses (stimulus,

Universal Basic Income) as real opportunity dissipates, and the troubling rise in shootings,

crime, random violence and plummeting marriage and birth rates.

The unraveling of social cohesion has consequences. Once social cohesion unravels, the

nation unravels.

What's the solution? At the national level, all that has been lost will have to be restored:

civic virtue, moral legitimacy, the social contract of opportunity, shared sacrifice that

falls most heavily on the wealthiest and most powerful, and a renewed national purpose centered

on serving the common good.

Is such a restoration of moral legitimacy and shared purpose even possible? No one knows.

If history is any guide, such a renewal is only possible after the empire of rampant self-interest

implodes.

So what do we do in the meantime? Nurture our own social cohesion by living purposefully

and sharing sacrifices and bounties with those we trust and admire--those in the lifeboat

we chose to join.

This essay was first published as a weekly Musings Report sent exclusively to subscribers and

patrons at the $5/month ($54/year) and higher level. Thank you, patrons and subscribers, for

supporting my work and this free website.

If you found value in this content, please join me in seeking solutions by

becoming

a $1/month patron of my work via patreon.com.

My new book is available!

A Hacker's Teleology: Sharing the Wealth of Our Shrinking Planet

20% and 15% discounts (Kindle $7, print $17,

audiobook now available $17.46)

Read excerpts of the book for free (PDF).

The Story Behind the Book and the Introduction.

Recent Videos/Podcasts:

It Always Ends The Same Way (34:33) (with Gordon Long)

My COVID-19 Pandemic Posts

My recent books:

A Hacker's Teleology: Sharing the Wealth of Our Shrinking Planet

(Kindle $8.95, print $20,

audiobook $17.46)

Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $5, print $10, audiobook)

Read the first section for free (PDF).

Pathfinding our Destiny: Preventing the Final Fall of Our Democratic Republic

($5 (Kindle), $10 (print), (

audiobook):

Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake

$1.29 (Kindle), $8.95 (print);

read the first chapters

for free (PDF)

Money and Work Unchained $6.95 (Kindle), $15 (print)

Read the first section for free (PDF).

Become

a $1/month patron of my work via patreon.com.

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

|

Thank you, Laura D. ($50), for your exceedingly generous contribution to this site -- I am greatly honored by your steadfast support and readership. |

Thank you, Jay & Teresa T. ($100), for your outrageously generous contribution to this site -- I am greatly honored by your steadfast support and readership. |