Now Hiring: The Ministry of Failure

Those expecting some centralized, political-administrative "solution" will be disappointed, as the political-administrative "solution" is actually the problem.

The Ministry of Failure is hiring, as their decades-long expansion is accelerating. You probably don't know about the Ministry, but you see its handiwork everywhere. The principle behind the Ministry's existence and its raison d'etre is simple: failure is more profitable than efficiency.

The greater the inefficiency and the higher the failure rate, the fatter the budgets and profits. Consider the permit process: the longer it takes, the more revisions and hoops the applicant must go through and the higher the late fees and penalties for non-compliance, the fatter the budget of the agency and the fatter the compensation of the administrative staff. Inefficiency is more profitable than efficiency.

Consider the immense profitability of planned and quasi-planned obsolescence. The Ministry of Failure doesn't take any chances; it requires manufacturers to use the cheapest, lowest-quality electronic components so the failure of the controller board is essentially guaranteed. And since the cost of the replacement board and the labor to install it is so outrageous, the consumer is forced to buy a new product. Failure is more profitable than durability.

The Ministry is also tasked with eliminating competition while masking this behind a phony facade of faux competition. Consider insulin, a pharmaceutical product that is essential to diabetics. Here is a snippet from the Yale School of Medicine website:

Insulin is seven to 10 times more expensive in the U.S. compared with other countries around the world. The same vial of insulin that cost $21 in the U.S. in 1996 now costs upward of $250. But it takes only an estimated $2 to $4 to produce a vial of insulin.

The Ministry of Failure has spent decades perfecting various cover stories for quasi-monopolies and cartels to justify their blatant profiteering. The Ministry tirelessly works to eliminate competition, grease the revolving doors of regulatory capture and add more compliance thorns to the regulatory thicket that keeps oh-so-unprofitable competition safely suppressed.

So insulin costs 10X in the U.S.? Fantastic! Thanks to the efforts of the Ministry of Failure, this abject failure is incredibly profitable.

The Ministry understands that any efficiency or reduction in administrative friction steps on somebody's toes by disrupting the profitability of failure and administrative churn. All those toes crushed by efficiency and reducing administrative dead weight belong to powerful interests, and so everything continues to be done the way it's been done because any increase in efficiency / durability and any reduction in administrative bloat hurts somebody with political clout.

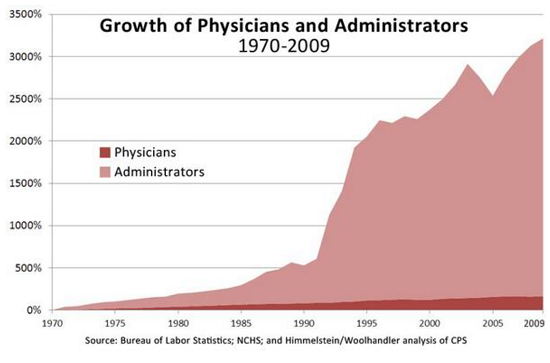

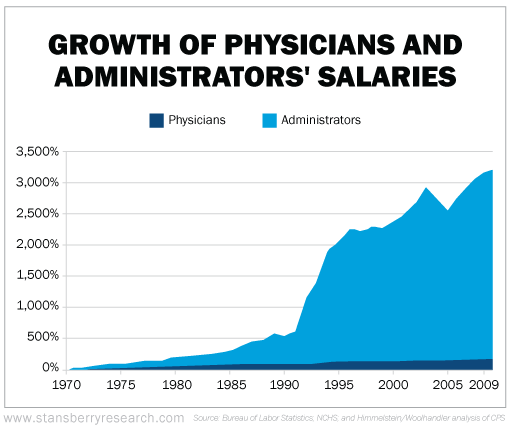

One of the greatest successes of the Ministry of Failure has been the rise to dominance of administrative bloat. Consider the example of the healthcare sector, which has experienced an explosive rise in the number of administrators and in the salaries of these administrators (see charts below).

This doesn't reflect the staggering increase in administrative burdens placed on doctors and nurses. The Ministry of Failure has worked tirelessly to exhaust frontline workers everywhere with needless, pointless admin duties.

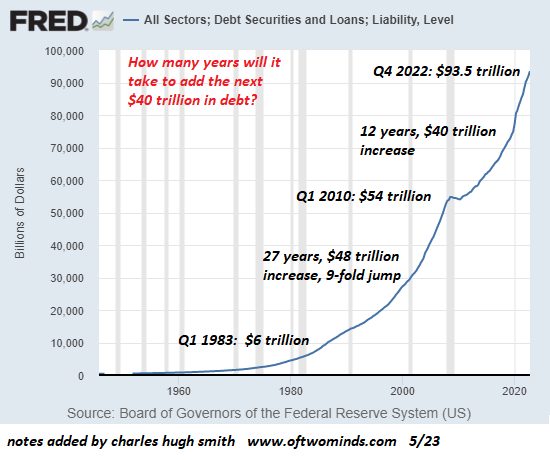

All of this bloat and inefficiency has been papered over with an equally explosive rise in borrowed money. All the gross inefficiencies, skims, scams and administrative bloat have pushed costs higher, and so the Ministry has worked with the political class and the Federal Reserve to flood the economy with "free money" borrowed into existence by the Fed and the federal government.

Since efficiency and reducing administrative bloat are impossible because somebody's toes will be stepped on, the only "solution" is to slosh more money into the failed system. If insulin costs 10X what it costs in other developed nations, no problem, let's just borrow another trillion dollars (oh heck, make it $10 trillion) so the costs of failure disappear into the background.

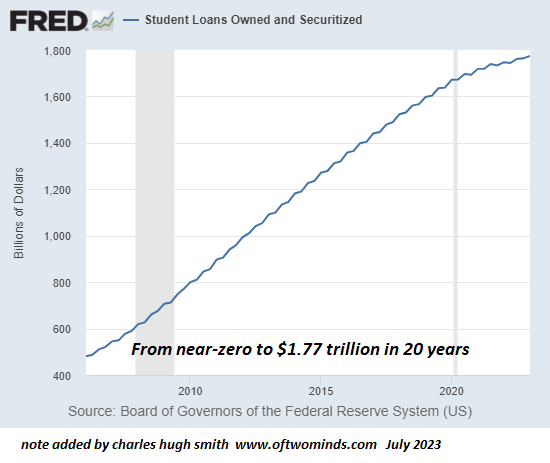

One of the outstanding successes of the Ministry of Failure in the past two decades has been the expansion of student loan debt from near-zero to $1.77 trillion. These trillions paid for the expansion of administrative bloat in higher education, and nice salaries and benefits for the administrators. Everybody wins, right?

That all this failure is a net loss to our society and economy is masked by the borrowed trillions. Need more money to pay for failure? Just borrow more. So total debt, public, private and corporate, skyrockets from $20 trillion to $95 trillion, so what? The Fed can always create as much as we need to afford the profitability of failure.

But this "solution" is illusion: the costs of failure have simply been transferred to the citizenry, society and the economy, all of which are now staggering under a crushing weight of debt, money borrowed to keep failure profitable.

Those expecting some centralized, political-administrative "solution" will be disappointed as the political-administrative "solution" is actually the problem.

The default path is to take a job in the Ministry of Failure and borrow boatloads of money to paper over the costs of systemic failure in our own lives.

The only real solution available is to develop solutions for yourself and your household: pursue

Self-Reliance and learn how to accredit yourself, a process I describe in my book

Get a Job and Build a Real Career. Solutions and workarounds abound, but they're not centralized or administrative in nature.

My new book is now available at a 10% discount ($8.95 ebook, $18 print):

Self-Reliance in the 21st Century.

My new book is now available at a 10% discount ($8.95 ebook, $18 print):

Self-Reliance in the 21st Century.

Read the first chapter for free (PDF)

Read excerpts of all three chapters

Podcast with Richard Bonugli: Self Reliance in the 21st Century (43 min)

My recent books:

The Asian Heroine Who Seduced Me

(Novel) print $10.95,

Kindle $6.95

Read an excerpt for free (PDF)

When You Can't Go On: Burnout, Reckoning and Renewal

$18 print, $8.95 Kindle ebook;

audiobook

Read the first section for free (PDF)

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States

(Kindle $9.95, print $24, audiobook)

Read Chapter One for free (PDF).

A Hacker's Teleology: Sharing the Wealth of Our Shrinking Planet

(Kindle $8.95, print $20,

audiobook $17.46)

Read the first section for free (PDF).

Will You Be Richer or Poorer?: Profit, Power, and AI in a Traumatized World

(Kindle $5, print $10, audiobook)

Read the first section for free (PDF).

The Adventures of the Consulting Philosopher: The Disappearance of Drake (Novel)

$4.95 Kindle, $10.95 print);

read the first chapters

for free (PDF)

Money and Work Unchained $6.95 Kindle, $15 print)

Read the first section for free

Become

a $1/month patron of my work via patreon.com.

Subscribe to my Substack for free

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

|

Thank you, N.H.M. ($50), for your magnificently generous Substack subscription to this site -- I am greatly honored by your support and readership. |

Thank you, Mark D. ($50), for your superbly generous Substack subscription to this site -- I am greatly honored by your support and readership. |

|

|

Thank you, Mary W. ($50), for your splendidly generous Substack subscription to this site -- I am greatly honored by your support and readership. |

Thank you, Engineer2.0 ($50), for your marvelously generous Substack subscription to this site -- I am greatly honored by your support and readership. |