How the U.S. Could End Up with High Interest Rates

January 16, 2008

I will be away on family matters from Jan. 16 - 24. I apologize for the lack of new posts in this period, and invite you to explore the voluminous archives on this site: forbidden stories, 2007 archives, Recommended Books/Films, and even the first chapters of a young-adult adventure novel, Claire's Great Adventure. I am sorry, but I will be unable to reply to email until I return.

Everywhere you turn, the pundits' predictions are unanimously for "much lower interest rates." Aren't you a little skeptical of any "received wisdom" on which the pundits all agree? I certainly am, as history has time and again thumbed its nose at collective certainty by swerving in the exact opposite direction of what was unanimously predicted as a "sure bet."

Low interest rates are supposed to calm the recessionary waters by invigorating the sagging housing market. Sure, lower rates make everything from corporate debt to new auto loans cheaper to service--but the real impact, we're told, will be on housing.

Why? Two reasons. First, the family house is the bedrock of 2/3 of the nation's families' wealth--and the key metric in their perception of overall family wealth (up, down, neutral).

Second, the last seven years of "prosperity" have been ones of equity expansion (rising stock market and home equity) and equity extraction (re-financing/equity lines of credit). If lower rates can re-ignite housing sales, the hope is that home prices will at least stabilize or perhaps even start rising again.

In an economy where 70% of GDP is consumer driven, does anyone actually believe that lowering the cost of corporate borrowing will pull the economy out of recession?

So lower mortgage and interest rates are seen as the essential foundation of continued consumer borrowing and the reinvigoration of the consumer's primary asset, their home. Nice, but what if rates don't stay low, but actually start rising?

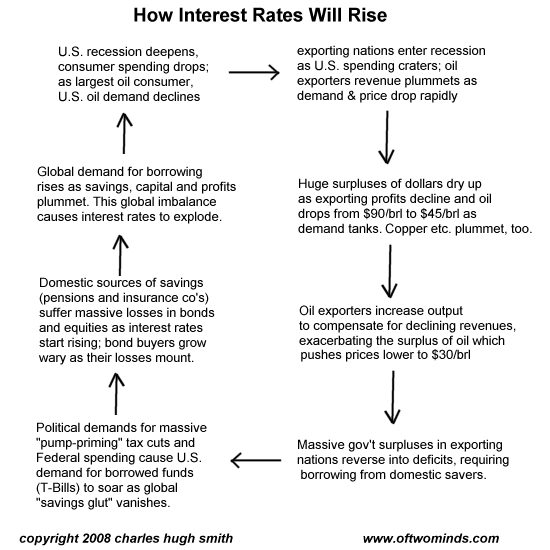

What situation could possibly cause U.S. interest rates to rise, regardless of the Federal Reserve's actions? Here's a graphic depiction of what could well cause real interest rates (that is, not the Fed Funds Rate, but what you and I will pay to borrow money) to rise in a long-term, self-reinforcing trend:

The key point is simple: the U.S. has been able to fund stupendous government deficits and a cheap/easy-money fueled housing bubble because non-U.S. banks and investors were piling up mountains of dollar-based exporting profits and petro-dollars which they needed to invest somewhere. Trillions of these profits flowed into U.S. bonds and debt-based securities (mortgage-backed securities, etc.), enabling cheap, easy-to-get loans and mortgages.

So what happens of a global recession knocks down both the profits made by exporting to the U.S., and the demand for oil? Then the pool of hundreds of billions in dollars looking for a home dries up in astonishingly short order.

As exporting nations slip into recession and deficit spending, they will tap the savings and capital of their own citizens. The way to do this is raise interest rates.

The pool of savings available to the profligate U.S. will dwindle, forcing the U.S. to bid for the shrinking pool of global savings. The only way to secure funding will be to raise the rates of return being paid to savers--i.e., interest rates will rise.

Two other forces will exacerbate this trend. As revenues drop along with the price of crude oil, oil exporters will pump even more product to compensate for lower revenues. This will depress prices further, pressuring exporters to pump more, and so on.

Secondly, as the global recession depresses corporate profits, global stock markets will tank, erasing trillions in capital. As interest rates rise, the value of existing bonds drops, too, setting up a one-two punch to pension funds, insurance company holdings, and individuals' retirement accounts. The global pool of capital will shrink, along with profits, reserves and savings.

All of this seems commonsensical, but we are told again and again that global savings are so robust that rates will stay low for years or even generations. What the pundits overlook is this: those savings are a result of an uprecedented global boom which is now ending. Once the boom dissipates, the profits and savings vanish along with it-- and so does all the cheap money which fueled the boom.

Readers Journal has been updated! Check out the new thoughtful, provocative ideas which have been added, including "401K debt cards," an excellent new essay by Lloyd L., What to Tell Your Children? and a new book recommendation by Riley T., Deer Hunting with Jesus: Dispatches from America's Class War

NOTE: contributions are humbly acknowledged in the order received. Your name and email remain confidential and will not be given to any other individual, company or agency.

A flurry of much-appreciated donations arrived in the past two weeks, and rather than delay recognition of those charitable souls who honored this site with their financial support, I am acknowledging one for every day I will be absent:

Thank you, Cheryl A. ($50), for your amazing donation in support of this humble site. I am greatly honored by your ongoing contributions and readership, and by your suggestions for topics.

charles hugh smith

Investing In Revolution

Ultra-Processed Life

The Mythology of Progress

Self-Reliance in the 21st Century

Burnout: Reckoning and Renewal

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States

A Hacker's Teleology

Will You Be Richer or Poorer?

Pathfinding our Destiny

The Consulting Philosopher

Money and Work Unchained

Inequality and the Collapse of Privilege

Why Our Status Quo Failed and Is Beyond Reform

A Radically Beneficial World

Get a Job, Build a Real Career and Defy a Bewildering Economy

The Nearly Free University

Resistance, Revolution, Liberation

Investing in troubled times

Survival +

Add Of Two Minds to your reader:

CHS

Weekly Musings Reports

Subscribers ($5/mo) receive weekly Musings Reports. At readers' request, there is also a $10/month subscription option.

What subscribers are saying about the Musings (read samples):

"What makes you a channel worth paying for? It's actually pretty simple - you possess a clarity of thought that most of us can only dream of, and a perspective that allows you to focus on the truth with laser-like precision." Jim S.

The "unsubscribe" link is for when you find the usual drivel here insufferable.

2005

2010

2015

2020

2025