The Housing Revolution: From Speculative Investment to Low-Cost Shelter

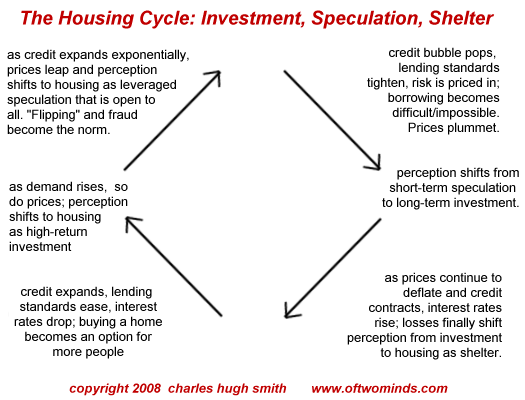

The revolution unfolding in U.S. housing will shift the perception of home ownership as a store of investment/speculative value to low-cost shelter. Some will say this is a horrible devolution, others a much-needed evolution; perhaps it is another cycle based on the larger credit-expansion/contraction cycle: (see below)

The key feature of housing as investment or speculation is that it depends totally on cheap, readily available lending to sustain prices. Once cheap, readily borrowed money dries up, so does the pool of potential buyers. When sellers far outnumber buyers, prices fall--and as credit shrinks, then the price eventually falls to its cash value, i.e. what someone is willing to pay in cash for the dwelling.

The salient feature of housing on the upswing half of the cycle is that the entire cost structure becomes bloated. When prices are rising by 10% or more in a short period of time, the cost of labor and materials is sloughed off--the owners' eyes are glued to the prospect of quick profit.

Even those who are "investing for the long-term" focus not on rising costs but on the "value added" by unnecessary "improvements" such as granite countertops, lavish bathrooms, "bonus rooms," etc. The perceived "value" is not so much the actual advantages of the improvement--let's face it, granite doesn't make you a better cook or even enable faster cleanup--but on the increase in selling price the improvement is supposed to yield.

In the upswing, "home" magazines proliferate as do articles about "which projects add more value." Housing is perceived as a store of appreciating value, and those who benefit from this perception relentlessly propagandize this perspective in the mainstream media.

As the "land rush" to buy/invest and "add value" increases, so do costs all along the line. Demand for skilled labor and materials trigger hefty increases in the cost of construction and renovation; as builders get busy, they raise their profit margins. As sales prices rise, property taxes increase; all of these rapidly rising expenses of ownership are ignored as prices are climbing even faster.

At the peak of the credit cycle, credit growth is exponential, feeding a speculative frenzy. The costs of ownership far exceed the cost of renting, but "ownership" is no longer the focus; housing is viewed first and foremost as a highly leveraged speculative vehicle that "everyone" can play.

As the speculative mania takes hold, builders ignore rising costs and the fundamentals of location and demand, and leverage all available resources into building "product" which can be sold even before the foundation is poured.

Then the credit cycle turns, as it always does, usually suddenly. Highly leveraged credit bets fail, risk rears its ugly head, regulators discover widespread fraud ("round up the usual suspects") and the euphoria is replaced by fear.

As credit dries up, all real estate is faced with plummeting demand. Buyers are scarce for two reasons: few can borrow the vast sums now required to buy property, and potential buyers are wary of falling prices. Buying on the way down ("catching the falling knife") is a good way to lose one's shirt.

The virtuous cycle of ever-rising values supporting ever-rising leverage reverses, and declining prices pull the props out from leveraged speculation. No-down or low-down payment owners quickly sink to negative equity, and even those who put down 20% are facing 50% losses in capital after a mere 10% decline in the value of their home.

As speculators are forced out of the real estate market by losses and insolvency, then players revert to the "real estate is the best long-term investment" mantra.

Unfortunately there is a huge fat diseased fly in the "investment" ointment: the bloated cost structure left from the speculative bubble remains firmly in place. Everyone in the food chain is loathe to lower prices; everyone from contractors to suppliers to cities collecting property taxes has built high-cost structures: extra employees, membership at the YMCA for all employees, new trucks, etc. etc.

And in the go-go environment of easy speculative money, regulatory costs climb as well; with few constraints on costs, then workers compensation insurance, liability insurance, etc. all rise as well, and then stubbornly stay high even as real estate slumps.

As losses mount, everyone in the food chain demands subsidies and give-aways to prop up sagging prices. Since costs have risen far beyond historical measures of value and speculative demand has vanished, the supply/demand ratio cannot support inflated prices without government subsidies.

But alas, as the true (high) costs of such subsidies becomes visible, public support disappears and the subsidies are cut. Once this last leg of support is pulled, the price of real estate falls to its "natural" level, i.e. in line with the value as set by credit availability and by the market-rate rental income the property generates.

Since overbuilding is a natural result of credit bubbles, there are now more residences than households. As credit tightens, the entire economy contracts; as jobs are lost, households increase in size and the demand for more residences drops.

As losses mount and assets deflate, households jettison surplus housing: second homes, "investment" condos, etc., further adding to the inventory of empty homes.

If the credit expansion was truly historic (i.e., 1920s and the present), then the resulting contraction will be historic, too, lasting longer than anyone anticipates.

As housing declines along with credit availability, bottom after bottom is called by the real estate industry--but all are false. As equity shrinks and each "bottom" is followed by further declines, households' perception of the "long-term investment value" of housing weakens.

The problem is the cost-structure of the housing food chain remains completely out of touch with historic ratios. Once the cost structures rise, they stubbornly resist any decline; skilled labor only grudgingly accepts lower pay, counties grudgingly lower property taxes, realtors grudgingly discount fees, and so on.

For instance: back in the early 1980s, my company built numerous small (under 1,000 sq. ft.), modest "starter homes" for about $40,000, or about $45/sq. ft. Adjusted for inflation, such homes would cost about $90,000 in today's dollars, or $90/sq. ft. Yet prices for even modest homes have soared to $200 to $300/sq. ft., and the average size of houses has bloated to absurdly impractical 3-4,000 sq. ft. McMansions.

Note that the cost-structures of maintaining such huge homes have risen, too; heating and cooling such vast interior spaces is not efficient or cheap, and commuting to distant exurban housing is no longer cheap, either.

The ultimate end-point of the credit contraction cycle is the reduction of the entire cost structure of housing back to historic norms: roughly 2 to 3 times median income to own, and roughly 1/3 annual income to rent.

Once the perception of housing as a sure-fire long-term investment has been eroded by year after year of declining or stagnant prices, then households will revert to deciding to buy only if buying is actually cheaper than renting. With leverage largely unavailable ("prove you don't need the money and we'll lend it to you"), the "return on investment" of the cash required to buy a home will be: the fixed costs are lower than renting an equivalent dwelling.

About 25% of all homes in the U.S. are owned free and clear (no mortgage). As elder owners pass on, these houses may well be seen by the lucky offspring/inheritors not as an asset to sell to fund superflous consumption but as a desirable low-cost place to live: that is, shelter.

Sometimes a revolution occurs mostly in the minds of the participants.

charles hugh smith

Investing In Revolution

Ultra-Processed Life

The Mythology of Progress

Self-Reliance in the 21st Century

Burnout: Reckoning and Renewal

Global Crisis, National Renewal: A (Revolutionary) Grand Strategy for the United States

A Hacker's Teleology

Will You Be Richer or Poorer?

Pathfinding our Destiny

The Consulting Philosopher

Money and Work Unchained

Inequality and the Collapse of Privilege

Why Our Status Quo Failed and Is Beyond Reform

A Radically Beneficial World

Get a Job, Build a Real Career and Defy a Bewildering Economy

The Nearly Free University

Resistance, Revolution, Liberation

Investing in troubled times

Survival +

Add Of Two Minds to your reader:

CHS

Weekly Musings Reports

Subscribers ($5/mo) receive weekly Musings Reports. At readers' request, there is also a $10/month subscription option.

What subscribers are saying about the Musings (read samples):

"What makes you a channel worth paying for? It's actually pretty simple - you possess a clarity of thought that most of us can only dream of, and a perspective that allows you to focus on the truth with laser-like precision." Jim S.

The "unsubscribe" link is for when you find the usual drivel here insufferable.

2005

2010

2015

2020

2025