Phase Shifts, Stick/Slip and the Demise of Our "Socialist" Housing Policy

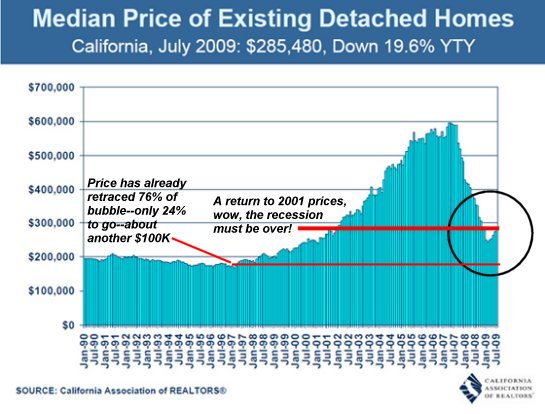

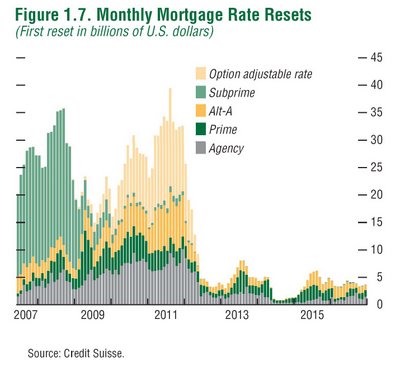

Any of several critical factors could trigger the next phase shift decline in housing prices. (To see the charts in full, please click on the title above) The government owns well over half the nation's $10 trillion in mortgages via its defacto ownership of Fannie Mae and Freddie Mac, and it has guaranteed virtually all the mortgages originated in the past year via FHA or VA. Anyone claiming to be a supporter of free-market capitalism must demand an immediate end to this 100% "socialist" support of the U.S. housing and mortgage markets. The reason why realtors, bankers, builders and politicos are nervously whispering "we're all socialists now" is simple: were the Fed and Federal government to withdraw their subsidies, guarantees and outright purchases of mortgages, the mortgage market would instantly freeze up or start pricing in the very real risk that housing is not "recovering" and that anyone holding a mortgage could suffer huge losses if real estate continues declining in value. If hypocrisy was fatal, virtually every realtor, banker, mortgage lender, Fed and Treasury official and craven politico would instantly expire. Housing is the ultimate "too big to fail"--yet it is failing nonetheless. To understand why, let's revisit one of my first explorations of how phase shifts offer a guide to the housing bubble's decline (from 3.5 years ago): Phase Transitions, Symmetry and Post-Bubble Declines (August 2, 2006) Clearly, we have experienced only the first leg of the decline; thanks to unprecedented "socialist" backstopping, guarantees, subsidies and outright ownership of mortgages, buyers in 2009 were persuaded "the bottom is in" and millions of souls rushed in to buy a home "at the bottom." Unfortunately for the bottom fishers, there are a daunting number of triggers for the next leg down. 1. Due to growing political pressure now that "the recession is over" and Fed/Federal debt is skyrocketing into the trillions of dollars annually, the Fed might be constrained from buying another $1.2 trillion in mortgages in 2010, 2011, and beyond. The result of any weakening in this "socialist" policy to prop up housing no matter how many trillions are needed will be nearly instantaneous: the mortgage market will either disappear or interest rates will leap and lending standards will tighten dramatically, effectively ending the subsidized sales which promoted the fantasy that "housing is in recovery." 2. A new wave of mortgage re-sets swamps the socialist support of the market. 3. The pressure building from underwater mortgages, foreclosures and job/income losses will "slip," unleashing a sudden decline in house valuations. One of the concepts I cover in Survival+ is the stick-slip hypothesis. An earthquake is an example of this phenomenon: the pressure on two adjacent plates of the Earth's crust rises without apparent consequence until the plates suddenly "slip," triggering a devastating earthquake. Look how suddenly housing prices fell once the pressure reached a threshold and the market "slipped" in a phase transition: Another phenomenon observed in Nature is the Pareto Principle: that 20% of a group can generate outsized influence on the other 80%. Often referred to as the 80/20 rule, this can be distilled down to the 4/64 rule. This led me to explore the idea that 4% of the homeowners with mortgages (50 million mortgages so 4% is 2 million homeowners) defaulting could trigger a collapse in the housing market: Can 4% of Homeowners Sink the Entire Market? (February 21, 2007) We now know the answer: yes, they can. The consequences continue unfolding, as I forecast in that entry from three years ago: Now that over 2 million homes have already been foreclosed and another 5 million are in default/distressed, we are rapidly approaching the critical 20% threshold: when 20% of all mortgages outstanding in 2007 are distressed/in default (10 million), then the odds of another "earthquake"/slip in housing prices increase dramatically. If we consider just the number of mortgages which are underwater--the mortgage exceeds the value of the property--that number is already estimated at 24%: well above the Pareto threshold for triggering outsized effects on the entire group of mortgage holders. Another wave of mortgage re-sets lies just ahead. It doesn't take much forecasting acumen to anticipate another wave of defaults and thus foreclosures. If we add the "shadow inventory" of homes being held off the market by sellers and lenders, then the market might already be close to the "10 million mortgages in default" tipping point/phase shift. It is important to note that so-called "conventional" 30-year fixed mortgages are also at risk. Here is my analysis from 2007: The Mortgage Mess: The Soft Underbelly Beyond Subprime (April 10, 2007) . Note that "safe" "prime" mortgages are a distinct minority of the market, and recent reports have documented that the default rate for prime loans is leaping up to match the default rates for riskier "toxic" loans. Prices are determined by supply and demand. The current illusion of "recovery" has been fueled by two massive manipulations of the market: the supply has been artificially limited by the withholding of distressed homes in the "shadow inventory," and the demand has been artificially juiced by stupendous "socialist" government pumping via subsidies, guarantees, backstops and purchases/ownership of "private" markets. The next phase shift down will be triggered by market forces responding to the asymmetry between supply (high and rising) and demand (low and falling). It doesn't take any more houses coming on the market to trigger the next leg down; it will only take a decline in demand as the pool of bottom fishers is exhausted and potential buyers realize the "recovery" was purely government-orchestrated illusion. Special autographed book offer: Fellow author (Reinventing Collapse: The Soviet Example and American Prospects) and blogger (Club Orlov) Dmitry Orlov has just published a limited-edition collection of his most acclaimed essays titled Hold Your Applause! A donation of $21 or more will get you a signed copy of this very limited-run book, and help support Club Orlov. Please check it out and support an independent, informed voice. DailyJava.net is now open for aggregating our collective intelligence. Of Two Minds is now available via Kindle: Of Two Minds blog-Kindle

One of the central ironies of the current "housing recovery" is that it is 100% "socialist," that is, funded entirely by the Federal Reserve and the Federal Government. The Fed has purchased quite literally 99% of all the mortgage-backed securities issued in the past year--$1.2 trillion. Without the Fed purchases, there would be no mortgage securities market. It's as simple as that.

This is a staggering conclusion, for it suggests just how a "mere" 4% delinquency/foreclosure rate could trigger a "modest" 15% decline in housing values, which would put the nation's mortgage holders (if taken in aggregate) under water: the nation's household debt would exceed the value of the mortgaged residential real estate.

If you haven't visited the forum, here's a place to start. Click on the link below and then select "new posts." You'll get to see what other oftwominds.com readers and contributors are discussing/sharing.

Order Survival+: Structuring Prosperity for Yourself and the Nation and/or Survival+ The Primer from your local bookseller or from amazon.com or in ebook and Kindle formats.A 20% discount is available from the publisher.

Thank you, Helen St.C. ($5/month), for your exceedingly generous subscription to this site. I am greatly honored by your support and readership. Thank you, Thomas S. ($20), for this much-appreciated generous contribution to this site. I am greatly honored by your support and readership.