What If Housing Is Done for a Generation?

What if housing valuations are in a structural, multi-decade decline?

A strong case can be made that the fundamental supports of the housing market-- demographics, employment, creditworthiness and income--will not recover for a generation. It can even be argued that housing has lost its status as the foundation of middle class wealth, not for a generation, but for the long term.

Let's begin by noting that despite the many tax breaks lavished on housing--the mortgage interest deduction, etc.--there is nothing magical about housing as an asset. That is, its price responds in an open, transparent market to supply and demand and the cost of money and risk.

There are a number of quantifiable inputs that feed into supply and demand--new housing starts, mortgage rates and income, to name three--but there are other less quantifiable inputs as well, notably the belief (or faith) that housing will return to being a "good investment," i.e. rising in price roughly 1% above the rate of inflation.

If this faith erodes, then the other factors of demand face an insurmountable headwind, for the most fundamental support of housing is the belief that buying a house is the first step to securing middle class wealth.

Rising rates of homeownership require five conditions:

1. Favorable demographics: a cohort of potential buyers that is larger than the cohort of potential sellers.

2. Rising household formation rates: an expanding population does not necessarily translate into rising rates of household formation. If the number of people per household goes up, then the number of households can plummet even as population expands.

3. A large cohort of creditworthy potential buyers: that means buyers with savings, buyers with sufficient income to pay the mortgage and buyers with low debt loads.

4. An economy that generates rising incomes to support homeownership.

5. An unshakable belief that owning a house is a favorable and secure investment that will rise in value in the decades ahead.

If the first four conditions have eroded, then the belief in the permanence of a rising housing market will also erode.

The demographics are not favorable to housing on a number of fronts. Jim Quinn recently posted some devastating charts of U.S. demographics in his brilliant post CAUSE, EFFECT & THE FALLACY OF A RETURN TO NORMALCY (The Burning Platform).

Without going into too much detail, we can stipulate that the Baby Boom (65 million people) will be downsizing their housing, i.e. selling for the next two decades. We can also stipulate that most of the Baby Boom no longer has the wherewithal to buy second homes; rather, they will be dumping second homes to pay for living expenses as earnings, interest income and housing equity have all cratered since 2007.

Not only are there not enough younger workers to buy all these millions of homes that will be put on the market, few of those younger workers have either the creditworthiness or income to buy a house unless the Federal government gives them essentially free money and a no-down payment entry. With the Federal deficit skyrocketing, that sort of giveaway won't last long.

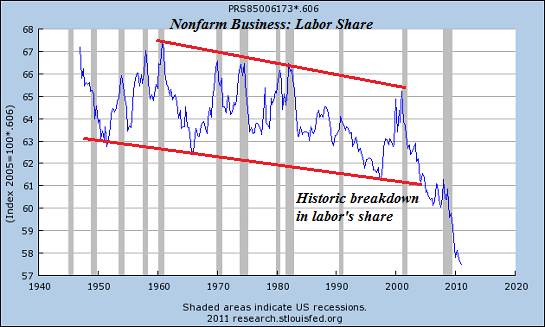

Labor's share of the national income has plummeted to historic lows. How can households be expected to buy a house when their real (inflation-adjusted) income declines year after year?

Labor share is the portion of output that employers spend on labor costs (wages, salaries, and benefits) valued in each year’s prices. Nonlabor share—the remaining portion of output-- includes returns to capital, such as profits, net interest, depreciation, and indirect taxes.

This chart suggests that a fundamental structural shift has taken place since the dot-com bubble popped in 2000: labor's share of the national income is in a secular long-term decline. That does not bode well for household income going forward.

Meanwhile, income has declined, especially for younger workers. Soaring Poverty Casts Spotlight on ‘Lost Decade’:

According to the Census figures, the median annual income for a male full-time, year-round worker in 2010 — $47,715 — was virtually unchanged, in 2010 dollars, from its level in 1973, when it was $49,065.

Overall, median household income adjusted for inflation declined by 2.3 percent in 2010 from the previous year, to $49,445. That was 7 percent less than the peak of $53,252 in 1999.

Notice that the only age brackets with flat or rising incomes are the over 55 cohort; everyone younger than 55 has seen their income slashed. And this is assuming "official" inflation is accurate; if it understates real inflation (loss of purchasing power), then the income declines are actually much more severe than charted here.

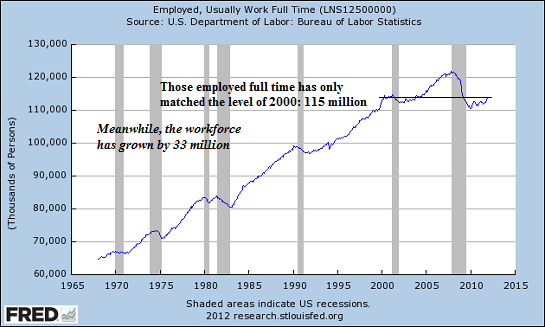

Part-time jobs and temp jobs do not generate enough stable income to support a mortgage. The only measure of employment that really matters in housing is fulltime employment, and that has declined to levels of 1999-2000 even as the workforce has added tens of millions of potential workers (all of whom have been deleted from the official workforce by Federal bean counters as "not in labor force" or "discouraged workers").

I don't have time to assemble the statistics for this entry, but the number of people with fulltime jobs that pay enough to support a mortgage is smaller than the number of fulltime workers. In other words, people working fulltime at or near minimum wage have a difficult time qualifying for a non-subsidized mortgage.

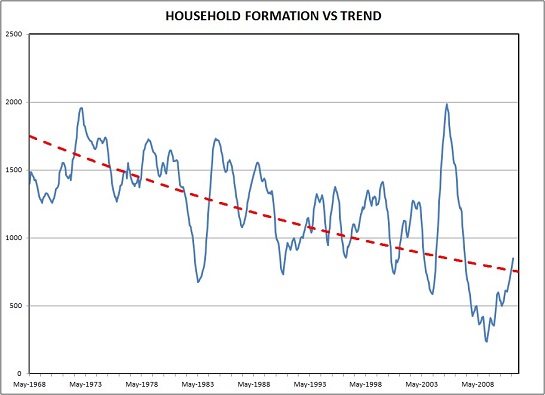

Household formation is also in a long-term decline. The chart depicts the housing bubble spike when marginally qualified people bought homes. Once the bubble popped, household formation plummeted and then returned to the declining trendline.

Recall that there are about 130 million housing units in the United States. About 112 million housing units are occupied: 75 million by owners and 37 million by renters. There are are about 19 million vacant dwellings: about 8.5 million second homes and vacation rentals, 2.5 million home for sale and another 8 million "vacant for other reasons" in Census-speak. (All number are approximate, drawn from 2010 Census Bureau data.)

If we subtract the 4 million second homes, that leaves about 15 million homes that could be occupied by owners or renters. With an average household size of about 2.5 people, that means we already have enough dwellings to house an additional 15 million households or 37 million people.

But this calculation overlooks the financial realities of declining income: the number of people per household is likely rising as fewer people can afford their own homes or apartments.

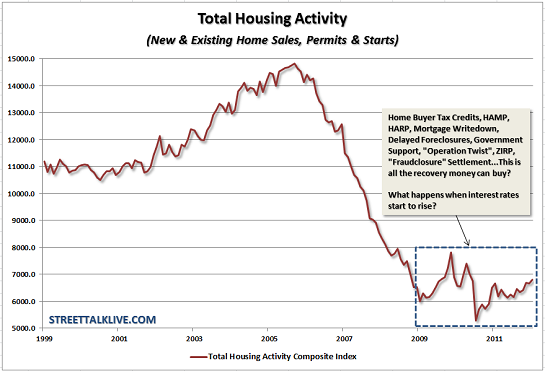

This oversupply of dwellings and soft demand is reflected in this chart of housing activity: despite unprecedented Federal subsidies and Federal Reserve pump-priming (buying impaired mortgages, lowering interest rates, etc.), housing has flatlined.

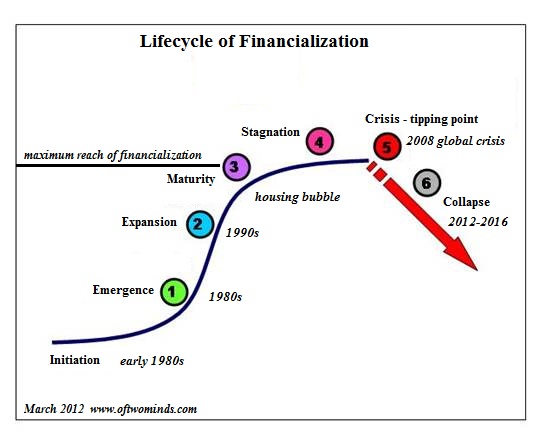

What few are willing to entertain is the possibility that housing is no longer the foundation of middle class wealth, and that its decline is structural, not cyclical. If we think of housing as an asset class that reflects not just demographics and income but financialization (i.e. hollowing out), then perhaps it is simply following the S-curve of financialization:

Lastly, we must consider the impact of declining employment, stagnating income and skyrocketing rates of student-loan debt on the creditworthiness of young potential buyers. If someone exits college with $100,000 in student-loan debt, how much will they have to earn to qualify for a $100,000 mortgage? How many graduates will earn that sum on a secure basis? Perhaps not as many as is generally assumed.

If the risk of default is once again priced into mortgages--that is, if the mortgage market ever ceases to be socialized and 99% guaranteed by Federal agencies--then we can also anticipate higher standards for qualification and a shrinking pool of qualified buyers.

It's easy to qualify people for a mortgage. The hard part is making sure they will have enough income and faith to service the mortgage for the next 30 years. If demand is softer than supply, prices will decline. If the belief that housing is the "best, most secure investment" fades, then so too will demand.

Declining employment, income and household formation are complex, long-term trends. If they continue trending down, so too will housing.

Planning your spring garden? Longtime oftwominds.com supporter Everlasting Seeds has a deal for you. At my request, Everlasting Seeds prepared a variety pack of non-hybrid seeds just for small gardeners like myself. If you've never planted a garden but always wanted to give it a try, this is the perfect opportunity to get started. Longtime gardeners will enjoy trying a different mix of veggies.

Planning your spring garden? Longtime oftwominds.com supporter Everlasting Seeds has a deal for you. At my request, Everlasting Seeds prepared a variety pack of non-hybrid seeds just for small gardeners like myself. If you've never planted a garden but always wanted to give it a try, this is the perfect opportunity to get started. Longtime gardeners will enjoy trying a different mix of veggies.

The Simple Garden - Special price: $29.95 + $8.00 shipping (USPS Priority Mail, insured and tracked)

Contains 30 seeds of each: Corn Broccoli Pea Onion Radish Carrot Cabbage Tomato Cauliflower Spinach Lettuce Pole Bean

Three New Podcasts now available: Macro Analytics podcasts with Gordon T. Long (about 20-25 minutes each). Each podcast is accompanied by a number of interesting charts; check out all the recent shows with Ty Andros, John Rubino, and three with Gordon and myself discussing these topics:

-- Fake Wealth Creation

-- The "Let's Pretend" Economy

-- Financialization

Contains 30 seeds of each: Corn Broccoli Pea Onion Radish Carrot Cabbage Tomato Cauliflower Spinach Lettuce Pole Bean

Three New Podcasts now available: Macro Analytics podcasts with Gordon T. Long (about 20-25 minutes each). Each podcast is accompanied by a number of interesting charts; check out all the recent shows with Ty Andros, John Rubino, and three with Gordon and myself discussing these topics:

-- Fake Wealth Creation

-- The "Let's Pretend" Economy

-- Financialization

Resistance, Revolution, Liberation will be available in a print edition later in April; buy it now as a Kindle eBook for $9.95.

We cannot know when the Central State and financial system will destabilize, we only know they will destabilize. We cannot know which of the State’s fast-rising debts and obligations will be renounced or written down; we only know the debts and obligations will be renounced in one fashion or another.The process of the unsustainable collapsing under its own weight and being replaced with a new, more sustainable model is called revolution, and it combines cultural, technological, financial and political elements in a dynamic flux. Though these systemic transitions can be profitably understood as cycles, history only illuminates past transitions; what the new arrangement will be is our choice.

| Thank you, John E. ($20), for your most-welcome generous contribution to this site--I am greatly honored by your support and readership. | Thank you, Robin B. ($50), for your gloriously generous contribution to this site--I am greatly honored by your support and readership. |