Why QE Won't Create Inflation Quite as Expected

The Fed can create money but if it doesn't end up as household income it is "dead money."

In the consensus view, the Federal Reserve's unlimited quantitative easing (QE3) programs will do two things: 1) boost stocks and other "risk on" assets and 2) generate inflation. The two follow-on effects are related, of course; gold and other hard assets are rising in anticipation of higher inflation.

But all is not quite as it seems when it comes to the inflationary effect of creating money. I'm going to cover a lot of ground here so buckle up and grab your favorite stimulating beverage.

Let's use some examples to illustrate key features of the relationship between money creation and inflation. Let's say a central bank prints $1 trillion in cash currency, digs a big hole and buries it. Does that $1 trillion in new money cause inflation? No, because it never got into the hands of people who might trade it for goods and services in the real world.

Recall that the premise of monetary inflation is straightforward supply and demand: when money is abundant and goods are scarce, the price of goods rises as abundant demand (everybody has lots of cash or credit) meets limited supply (limited oil, gold, grain, etc.) in an open marketplace.

Let's say the Fed electronically creates $1 trillion and metaphorically buries it in some account where it sits as "dead money." It cannot trigger inflation because it isn't reaching the hands of people who might use it to buy scarce goods and services.

Let's also recall that money is destroyed, not just created, when assets fall in value and bad debt is written down. Consider a house purchased for $350,000 at the top of the real estate bubble with a $50,000 cash down payment and a $300,000 mortgage. The owner defaults and the house is sold for $150,000. The $50,000 down payment was cash; it was not “on paper.” It has not been transferred to someone else; it has vanished.

The same can be said of the $150,000 the bank lost on the mortgage. The bank’s cash reserves (capital) take a $150,000 hit. That was real money, too, and it wasn’t transferred to someone else; it disappeared. Thus $200,000 of real money has been destroyed.

To the degree that immense overhangs of bad debt are slowly being written off, money is being destroyed. If the Fed “prints” $500 billion a year, and write-downs erase $500 billion, the money supply hasn’t expanded at all.

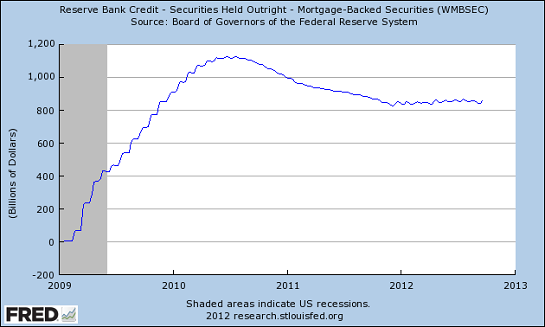

The Fed bought $1.1 trillion in mortgage-backed securities as part of its earlier QE interventions in 2009-10. Notice that the $1.1 trillion has already fallen to $850 billion--a decline of $250 billion in just a few years. The loans were paid down, paid off or written off.

According to the Balance Sheet of Households (federalreserve.gov), home mortgages have declined from $10.3 trillion in 2009 to $9.7 trillion in 2012. Credit is being destroyed in the primary asset of the American household, their home: one-third have zero equity (underwater), millions more have insufficient equity to borrow against/extract, and millions more are not creditworthy enough to borrow more, even though they have equity in their house.

The decline in asset values has destroyed money and credit.

The general assumption is that the Fed buys dodgy MBS from banks which then take the money and dump it into the stock market, pushing stocks higher. This assumption fails to consider the weak balance sheets of banks, which will soon be required to post some collateral behind their trillions of dollars of outstanding derivatives.

The favored collateral is U.S. Treasury bonds, and so banks may be constrained by their need to build reserves against future writedowns. They may end up buying Treasuries as collateral rather than gambling in the equities market. The newly created money may end up as "dead money" in reserves, not cash propping up equities.

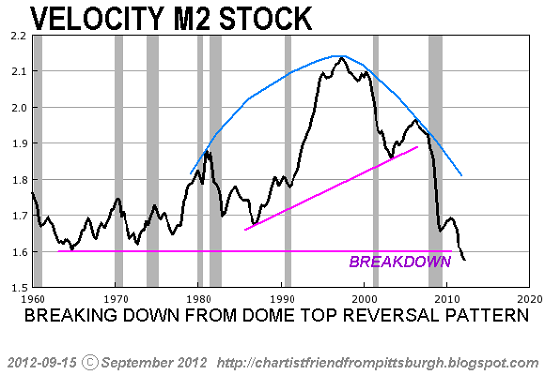

A number of indicators suggest money is not flowing into hands which might actually trade it for goods and services. Consider money velocity, courtesy of Chartist Friend from Pittsburgh:

The velocity of money buried in a hole is zero. The velocity of hoarded money is also zero. The velocity of credit that is never used (i.e. no money is actually borrowed and spent) is also zero. Money that is created but which has zero velocity cannot spark inflation.

If money were flowing into real-world households, we'd expect to see household incomes rise. Instead we see falling incomes. Here is the real (adjusted) income for the 45-54 year old age bracket, when lifetime earning tend to peak (courtesy of dshort.com):

Ouch. Income, Poverty and Health Insurance Coverage in the United States: 2011 According to the Census Bureau, "In 2011, real median household income was 8.1 percent lower than in 2007."

If there is net expansion of the base money supply, it isn't finding its way into household incomes where it could be spent on real goods and services.

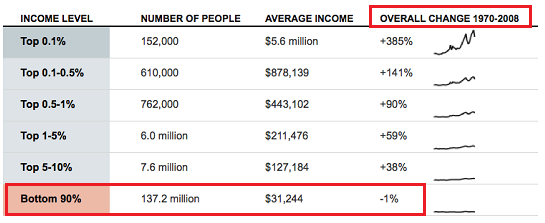

As for the "wealth effect," it only affects the 5% who own enough equities to make a difference. That narrows the whole "wealth effect" to 7 million people out of 142 million workers.

Interestingly, the top 5% is the only demographic that is actively deleveraging, i.e. reducing debt rather than borrowing more:

Add all this up and here's what we get: money is not just being created by the Fed, it's being destroyed by declines in asset valuations and writedowns of impaired debt. Credit may be expanding but the top rung of households is paying down debt, not borrowing more, and the bottom 95% are unable to add much to their already staggering debt load.

Incomes are declining, providing a smaller base for both spending and borrowing. The top 5% may be experiencing a "wealth effect" as stocks soar but 7 million people cannot levitate the entire $15 trillion U.S. economy much while the incomes of the 137 million other workers are stagnant or down.

Money velocity is plummeting and banks are hoarding Treasuries as much-needed collateral.

It's difficult to see how these forces could generate inflation. There may be new money and credit being created, but very little of it is flowing to households whose spending in the real economy drives inflation.

We are like passengers on the Titanic ten minutes after its fatal encounter with the iceberg: though our financial system seems unsinkable, its reliance on debt and financialization has already doomed it.We cannot know when the Central State and financial system will destabilize, we only know they will destabilize. We cannot know which of the State’s fast-rising debts and obligations will be renounced; we only know they will be renounced in one fashion or another.

The process of the unsustainable collapsing and a new, more sustainable model emerging is called revolution.Rather than being powerless, we hold the fundamental building blocks of power. We need neither permission nor political change to liberate ourselves. A powerless individual becomes powerful when he renounces the lies and complicity that enable the doomed Status Quo’s dominance.

| Thank you, Barney S. ($10), for your much-appreciated generous contribution to this site--I am greatly honored by your continuing support and readership. |