Note to Fed: Giving the Banks Free Money Won't Make Us Hire More Workers

Lowering interest rate and making credit abundant doesn't make employers hire more workers.

The Federal Reserve's policy of targeting unemployment is based on a curious faith that low interest rates and lots of liquidity sloshing around the bank system with magically lead employers to hire more workers. I say this is a curious faith because it makes no sense. In effect, the Fed policy is based on the implicit assumption that the only thing holding entrepreneurs and employers back from hiring is the cost and availability of credit.

But as anyone in the actual position of hiring more staff knows, it is not a lack of cheap credit that makes adding workers unattractive, it is the lack of opportunities to increase profit margins by adding more workers.

If the economic boom of the mid-1980s proves anything, it is that the cost of credit can be very high but that in itself does not restrain real growth. What restrains growth is not interest rates, it is opportunities to profitably expand operations.

What the Fed cannot dare admit is that in a crony-capitalist, globalized, State/cartel-dominated economy, there are few profitable opportunities, regardless of the cost of credit. Yes, there is a natural-gas boom in the Dakotas, but outside of energy plays the harsh reality is that the only way for most businesses to increase profits is reduce labor, not hire more workers.

The second survival tactic is to lower labor costs by recycling full-time, full benefits jobs into part-time or lower-paid jobs. Rather than pay insanely high healthcare premiums on full-time jobs, businesses lay off full-benefit workers and replace them with a mix of part-time workers who receive no benefits or contract workers who handle their own healthcare costs.

There is another way to recycle jobs to reduce costs: fire a $90,000/year employee and hire someone for $60,000 to do the same job. Mish has shown that virtually all the gain in employment since the start of the "recovery" is in the 55+ age group: Startling Look at Job Demographics by Age (Mish)

Older workers often complain that they have been replaced with "cheaper" younger workers who will work for less, but the real trend to is to hire higher-productivity workers for less pay. In most cases, as revealed by the above chart, the older workers are higher productivity for a number of self-evident reasons: they won't take maternity leave, they know their work well and have proven a work ethic that younger workers may not have had the opportunity to prove.

It is difficult to transition to a new career or get a job as an inexperienced worker for the reason that employers want someone who can be productive on Day One. Sadly, it is too costly and risky to take chances with on-the-job training or mentoring; it is lower-risk to find someone who can do the work immediately.

Older workers' healthcare insurance costs are skyhigh, but the solution is to hire older workers as consultants and push the costs of healthcare onto them. In many cases, older workers are covered by a spouse's insurance, so they can afford to take a job that offers no benefits.

The other trend the Fed cannot dare recognize is that cheap credit enables employers to reduce labor by investing in automation and software. If opportunities are scarce (and they are), or if the business is hanging on by a thread, then hiring more employees is the last thing an employer would do to boost productivity: the solution is reduce headcount and invest in tools that make the remaining employees more productive.

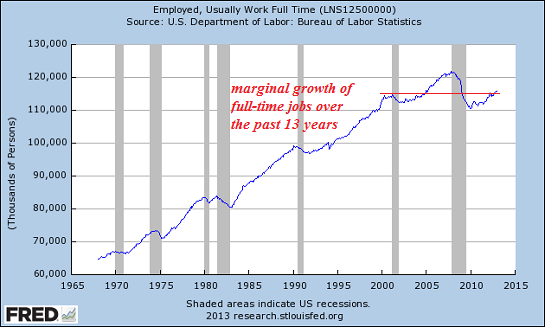

We can see this reality in the following charts: full-time employment has returned to levels reached 13 years ago, but median wages are lower, reflecting the "recycling" described above.

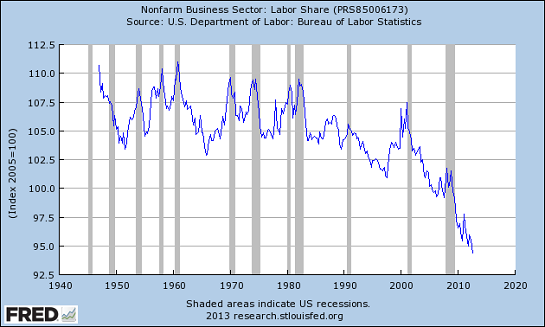

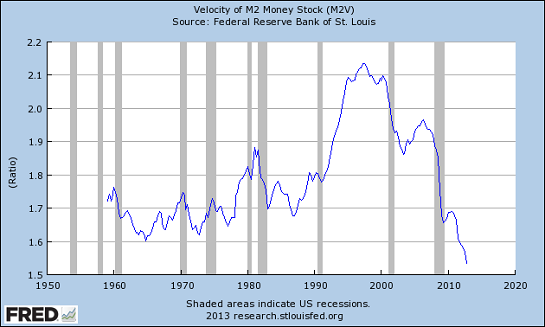

Meanwhile, labor's share of the non-farm private economy has fallen off a cliff, along with money velocity, which measures the relative activity of cash and credit:

So exactly what mechanism is the Fed trying to boost with super-low interest rates and massive liquidity (free money) in the banking sector? Answer: push businesses into high-risk ventures.

Federal Reserve Bank of Chicago President Charles Evans: “The investment climate seems to be one where people are increasingly understanding that very low interest rates on super safe assets are going to be around for a while. And if they’re worried by that they need to take on more risk - and taking on that more risk will help get the economy growing.”

In other words, the Fed's policy is to push for more mal-investment. There is no other way to describe the flow of money into risky, marginal ventures.

Note to Fed: there is too much of everything. Too many restaurants, too many apps, too many empty dwellings (19 million at last count), too many malls, too many nail salons. There is too much junk for sale everywhere, from retail outlets to online to jumble/garage sales. The developed world is awash in overcapacity in every sector other than a relative handful of special equipment/services (deep-ocean drilling rigs, etc.)

Pushing businesses to borrow money to gamble in risky ventures is precisely what happened in Japan in the late 1980s. With interest rates low and credit in abundance, bank reps went around to enterprises small and large begging them to borrow money for essentially any reason.

The net result: massive bubbles across asset classes and an overhang of debt that remains 20+ years later, as unpayable now as it was in 1992. That is the result of pushing enterprises into risk-on bets: bubbles and collapses.

What those with access to the Fed's free money--big banks and hedge funds--are doing with the zero-cost credit is invest in rentier skimming operations: buying 5,000 single family homes, buying $1 billion in apartments and homes to rent out, etc.

“It’s hard to find a private-equity firm on the planet that doesn’t have a strategy in this space,” Gary Beasley, chief executive officer at Waypoint Homes, said last week at the American Securitization Forum’s annual conference in Las Vegas. The Oakland, California-based company has bought homes in California, Arizona, Illinois and Georgia.

How many jobs are created by rentier skimming? Very few. Get the houses painted, hire a few handypeople to take care of maintenance and a few people to handle the property management.

The other way to make money with nearly-free credit is to chase risk-on assets, for example stocks. Why would any hedge fund or bank trading desk with easy access to the Fed's free money bother taking risks in the real economy which is burdened with massive over-capacity and sclerotic State-mandated cartels (healthcare, defense, etc.) when the easy money is in chasing assets higher?

How many jobs are created by chasing assets higher? Maybe the Fed thinks that high-end Manhattan restaurants will add staff to handle the influx of new money skimmed from the stock and bond markets, but if they think rentier/speculative skimming is going to add millions of jobs to the economy, they are delusional.

Perhaps if any of the Fed governors had ever operated a real business in the real economy, the board might have a somewhat better grasp on reality.

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify or understand. We will cover the five core reasons why things are falling apart:

1. Debt and financialization

1. Debt and financialization2. Crony capitalism and the elimination of accountability

3. Diminishing returns

4. Centralization

5. Technological, financial and demographic changes in our economyComplex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Not accepting responsibility and being powerless are two sides of the same coin: once we accept responsibility, we become powerful.

Kindle edition: $9.95 print edition: $24 on Amazon.com

To receive a 20% discount on the print edition: $19.20 (retail $24), follow the link, open a Createspace account and enter discount code SJRGPLAB. (This is the only way I can offer a discount.)

| Thank you, David C. ($5/month), for your wondrously generous subscription to this site -- I am greatly honored by your support and readership. | Thank you, Paul L. ($225), for your outrageously generous contribution to this site --I am greatly honored by your steadfast support and readership. |