The Global Endgame in Fourteen Points

An over-indebted, overcapacity economy cannot generate real expansion. It can only generate speculative asset bubbles that will implode, destroying the latest round of phantom collateral.

I have endeavored to lay out the global endgame in four recent entries:

Is This the Terminal Phase of Global Capitalism 1.0? (February 8, 2013)

Note to Fed: Giving the Banks Free Money Won't Make Us Hire More Workers (February 11, 2013)

Cheap, Abundant Credit Creates a Low-Return, Bubble-Prone World (February 12, 2013)

Europe Is Not "Fixed": Two Charts (February 13, 2013)

For those seeking a summary, here is the global endgame in fourteen points:

1. In the initial "boost phase" of credit expansion, credit-based capital ( i.e. debt-money) pours into expanding production and increasing productivity: new production facilities are built, new machine and software tools are purchased, etc. These investments greatly boost production of goods and services and are thus initially highly profitable.

2. As credit continues to expand, competitors can easily borrow the capital needed to push into every profitable sector. Expanding production leads to overcapacity, falling profit margins and stagnant wages across the entire economy.

Resources (oil, copper, etc.) may command higher prices, raising the input costs of production and the price the consumer pays. These higher prices are negative in that they reduce disposable income while creating no added value.

3. As investing in material production yields diminishing returns, capital flows into financial speculation, i.e. financialization, which generates profits from rapidly expanding credit and leverage that is backed by either phantom collateral or claims against risky counterparties or future productivity.

In other words, financialization is untethered from the real economy of producing goods and services.

4. Initially, financialization generates enormous profits as credit and leverage are extended first to the creditworthy borrowers and then to marginal borrowers.

5. The rapid expansion of credit and leverage far outpace the expansion of productive assets. Fast-expanding debt-money (i.e. borrowed money) must chase a limited pool of productive assets/income streams, inflating asset bubbles.

6. These asset bubbles create phantom collateral which is then leveraged into even greater credit expansion. The housing bubble and home-equity extraction are prime examples of this dynamic.

7. The speculative credit-based bubble implodes, revealing the collateral as phantom and removing the foundation of future borrowing. Borrowers' assets vanish but their debt remains to be paid.

8. Since financialization extended credit to marginal borrowers (households, enterprises, governments), much of the outstanding debt is impaired: it cannot and will not be paid back. That leaves the lenders and their enabling Central Banks/States three choices:

A. The debt must be paid with vastly depreciated currency to preserve the appearance that it has been paid back.

B. The debt must be refinanced to preserve the illusion that it can and will be paid back at some later date.

C. The debt must be renounced, written down or written off and any remaining collateral liquidated.

9. Since wages have long been stagnant and the bubble-era debt must still be serviced, there is little non-speculative surplus income to drive more consumption.

10. In a desperate attempt to rekindle another cycle of credit/collateral expansion, Central Banks lower the yield on cash capital (savings) to near-zero and unleash wave after wave of essentially "free money" credit into the banking sector.

11. Since wages remain stagnant and creditworthy borrowers are scarce, banks have few places to make safe loans. The lower-risk strategy is to use the central bank funds to speculate in "risk-on" assets such as stocks, corporate bonds and real estate.

12. In a low-growth economy burdened with overcapacity in virtually every sector, all this debt-money is once again chasing a limited pool of productive assets/income streams.

13. This drives returns to near-zero while at the same time increasing the risk that the resulting asset bubbles will once again implode.

14. As a result, total credit owed remain high even as wages remain stagnant, along with the rest of the real economy. Credit growth falls, along with the velocity of money, as the central bank-issued credit (and the gains from the latest central-bank inflated asset bubbles) pools up in investment banks, hedge funds and corporations.

The net result: an over-indebted, overcapacity economy cannot generate real expansion. It can only generate speculative asset bubbles that will implode, destroying the latest round of phantom collateral.

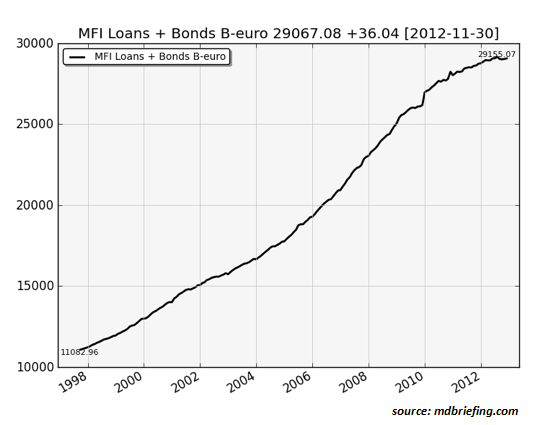

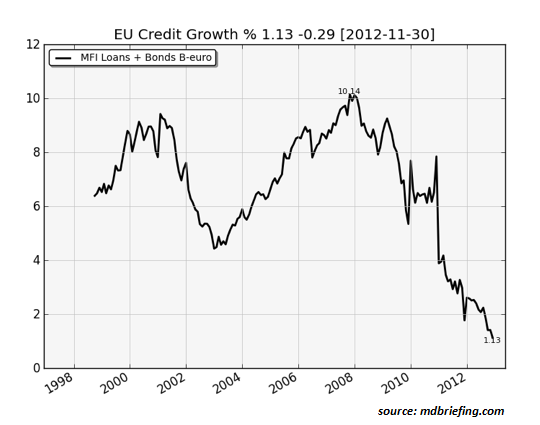

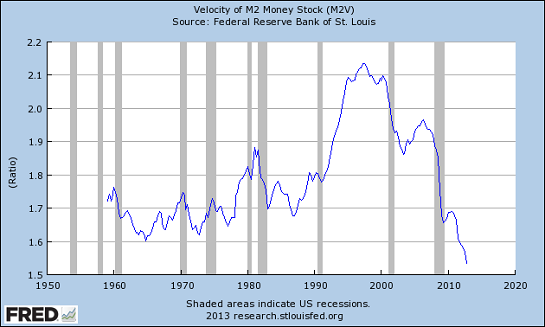

Here are three charts that illustrate #14:

Eurozone credit since the inception of the euro. This is roughly equivalent to TCMDO (Total Credit Market Debt Owed) in the U.S.

Eurozone credit growth:

Money velocity in the U.S.:

That is the endgame in three charts. Checkmate, game over.

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify or understand. We will cover the five core reasons why things are falling apart:

1. Debt and financialization

1. Debt and financialization2. Crony capitalism and the elimination of accountability

3. Diminishing returns

4. Centralization

5. Technological, financial and demographic changes in our economy

Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Not accepting responsibility and being powerless are two sides of the same coin: once we accept responsibility, we become powerful.

Kindle edition: $9.95 print edition: $24 on Amazon.com

To receive a 20% discount on the print edition: $19.20 (retail $24), follow the link, open a Createspace account and enter discount code SJRGPLAB. (This is the only way I can offer a discount.)

| Thank you, Kerry W. ($25), for your exceptionally generous contribution to this site -- I am greatly honored by your support and readership. | Thank you, Richard G. ($60), for your monstrously generous contribution to this site --I am greatly honored by your support and readership. |