Understanding Failed Policies: Wealth Effect, Wage Effect, Poverty Effect

Central banks' attempts to boost borrowing, consumption and wages by inflating asset bubbles leads to the poverty effect, not the wealth effect.

Central bankers have been counting on "the wealth effect" to lift their economies out of the post-2009 global meltdown slump. The wealth effect concept is simple: flooding the economy with credit and zero-interest money boosts the value of assets such as housing, stocks and bonds. Those owning the assets feel wealthier, and thus more inclined to borrow and spend more money. This new spending creates more demand which then leads employers to hire more employees.

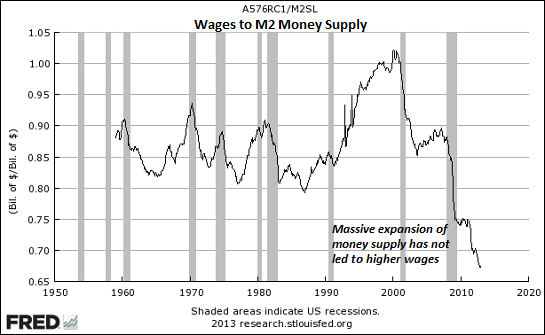

Unfortunately for the bottom 90% who don't own enough stocks to feel any wealth effect, the central bankers got it wrong: wages don't rise as a result of the wealth effect, they rise from an increased production of goods and services. Despite unprecedented money-printing, zero interest rates and vast credit expansion, real wages have declined.

Apologists will claim that it would even be worse without central banks attempting to inflate asset bubbles in search of the wealth effect, but the wage/M2 money supply correlation suggest chasing the wealth effect has been a policy failure.

The unintended consequence of inflating asset bubbles to drive an illusory wealth effect is that speculative bubbles inevitably pop, creating a pervasive poverty effect. The asset bubble creates phantom collateral that households borrow against. When the bubble pops, they're left with the debt and debt payments ("the poverty effect") while the ephemeral "wealth" has vanished.

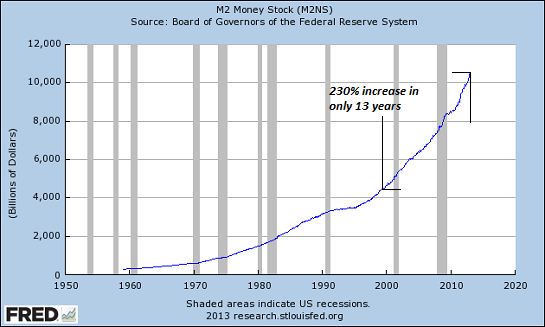

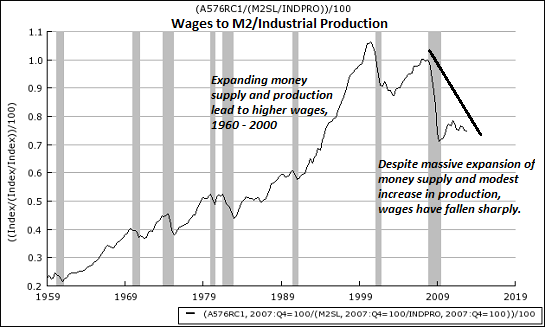

Frequent contributor B.C. has offered some charts correlating wages, M2 money supply and production. His commentary elucidates the difference between inflation that includes wages (wages rise along with prices) and inflation that erodes purchasing power (wages stagnate while prices and assets rise).

(The chart notes are mine.)

Here is B.C.'s commentary:

I tend to think of "inflation" as the effect on the purchasing power of wages from the differential rate of change of money supply (and by extension bank lending and GDP) to wages (relied upon virtually exclusively by 90% of households, including those receiving transfers from taxes on wages) with regard to production.In other words, if wages are rising along with production and prices, price inflation is largely a reflection of population, value-added output and consumption, and commensurate returns to labor from growth of money and production, i.e. an optimal growth condition.

However, if growth of money (M2) and bank lending (and GDP, which rises as a result of gov't deficit spending), exceeds growth of wages and production, money inflation tends to result in price inflation that erodes the purchasing power of wages and private production. This reflects economic conditions that are sub-optimal or recessionary.

To the extent that there is a so-called "wealth effect," the flow effect is likely in the opposite direction as is commonly assumed; that is, rising production and wages to money supply affect an increase in asset prices; therefore, it should be referred to as the "wage effect" on growth of economic activity and asset prices, rather than the converse.

Thus, the S&P 500 dropping back to the level of the mid-'90s (when the bubble commenced) would reflect the "wage effect" and actual sub-par economic conditions rather than the dubious "wealth effect" assumed from rising asset prices.

Of course, in the hyper-financialized US economy and global imperial trade regime, this is heresy.

Thank you, B.C. In other words, a sustainable wealth effect results from the wage effect, as rising production of goods and services organically boosts wages. The Federal Reserve and other central banks have it backwards: inflating asset bubbles does not increase wages or create a sustainable wealth effect; increasing production of goods and services bolsters wages which then leads to a sustainable wealth effect.

Inflating serial bubbles as a means of boosting more borrowing and consumption only leads to the poverty effect: an erosion of wages' purchasing power and the inevitable deflation of asset bubbles that leaves unpayable debt once the phantom collateral evaporates.

The Fed has been able to maintain price stability but not wage/purchasing power stability. That dooms its entire intervention project.

Simply put, central banks' attempts to boost borrowing, consumption and wages by inflating asset bubbles leads to the poverty effect, not the wealth effect.

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify or understand. We will cover the five core reasons why things are falling apart:

1. Debt and financialization

1. Debt and financialization2. Crony capitalism and the elimination of accountability

3. Diminishing returns

4. Centralization

5. Technological, financial and demographic changes in our economy

Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Not accepting responsibility and being powerless are two sides of the same coin: once we accept responsibility, we become powerful.

Kindle edition: $9.95 print edition: $24 on Amazon.com

To receive a 20% discount on the print edition: $19.20 (retail $24), follow the link, open a Createspace account and enter discount code SJRGPLAB. (This is the only way I can offer a discount.)

| Thank you, Helen S.C. ($10), for yet another magnificently generous contribution to this site -- I am greatly honored by your steadfast support and readership. | Thank you, Bud W. ($50), for your stupendously generous contribution to this site --I am greatly honored by your support and readership. |