Unpopped Housing Bubbles Abound

History suggests that we can anticipate the eventual popping of all remaining housing bubbles.

Though much has been written about the popping of the housing bubble in the U.S. and Ireland, remarkably little has been written about the many housing bubbles that remain unpopped. As a rule, speculative bubbles pop and revert to their pre-bubble levels, so we can anticipate the eventual popping of all remaining housing bubbles.

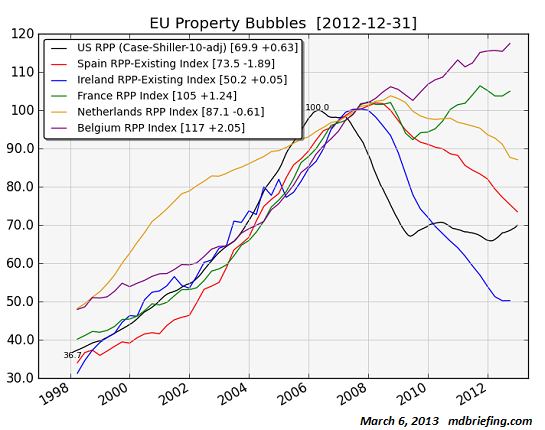

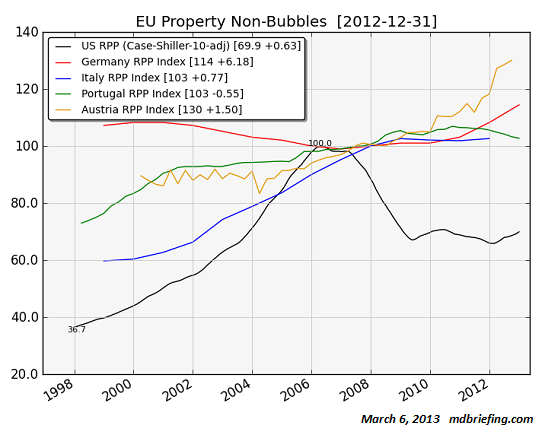

David P., proprietor of the excellent Market Daily Briefing blog, recently shared two charts depicting housing markets in the European Union. David explains his methodology of dividing the EU housing markets into two groups (EU Property Bubbles):

Many nations in Europe have had a property bubble, but only Ireland has officially had a bubble pop. Spain is currently in process of acknowledging their bubble pop, but many other nations in the eurozone appear to have had similar-looking housing price growth yet have not officially acknowledged their bubble price moves.

The different eurozone nations were split into two groups; states with property bubbles, and states without. Criteria for a bubble is property prices doubling within 10 years. The selection was relatively easy in most cases - the only borderline case was Italy, where they had property prices rise "only" 66% over 8 years. There are two notable cases: Belgium, where prices have gone up 243% since 1998 and are still at that lofty level, and France, where prices have risen 263%, and no correction has yet occurred.

The data comes from the ECB, but is collected by each member nation. They are index values, with the 100 value set generally to one of the years between 2007-2008. Some of these series update annually, some monthly, and some quarterly. It is a mix of data; some use only existing homes, others use existing and new homes. Data availablity varies between nations; every attempt was made to select the best series. To provide a "bubble baseline", the US Case Shiller 10-city index has been normalized with early 2006=100 and added to each graph.

Here are David's charts:

Notice that Ireland's decline tracks a classic bubble pop; the U.S. decline was stopped by gargantuan Federal subsidies (3% down payment loans passed out like candy, etc.) and Federal Reserve intervention (zero interest rates and $1+ trillion purchases of mortgages). Spain and The Netherlands have rolled over but still have a long way down to reach pre-bubble levels.

Belgium and France prove that "stone" (real estate) is still a popular investment, especially when credit money is sloshing around (see chart below).

Austria and Germany are playing catch-up in the housing bubble game--better late than never. Perhaps capital is fleeing risky EU locales and finding a home in German and Austrian real estate.

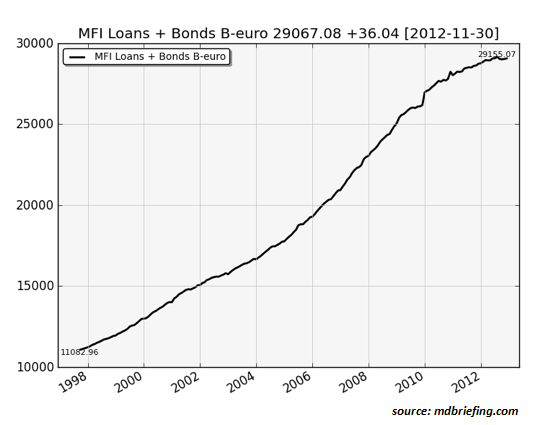

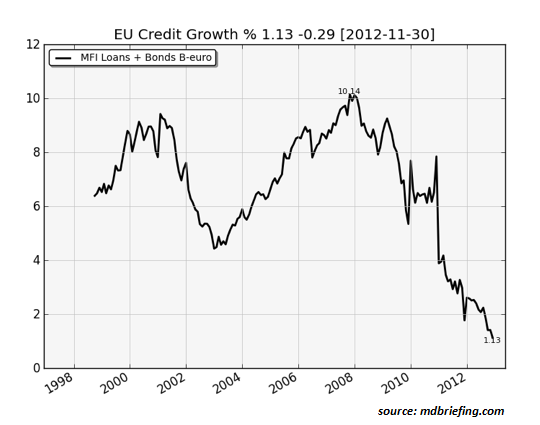

These two charts reveal the driver of the EU housing bubble and its piecemeal devolution: massive credit expansion, and a sharp decline in credit growth:

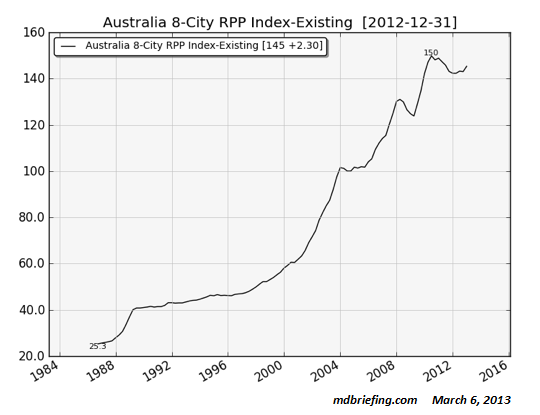

Housing bubbles are not limited to Europe, of course; here is David's chart of the Australian housing bubble:

Given the dearth of investment options open to households in China seeking to invest their prodigious savings, it is unsurprising that China's housing bubble continues expanding. Every proponent of housing during bubbles confidently proclaims that "this time it's different," and a decade later the dazed survivors shift through the financial rubble, wondering what went wrong with "guaranteed" fundamentals, trends, valuations, collateral and wealth.

Roundtable discussion with CHS, Gordon T. Long and Bill Laggner: China, Japan & Central Banking (25 Minutes, 34 Slides)

Roundtable discussion with CHS, Gordon T. Long and Bill Laggner: China, Japan & Central Banking (25 Minutes, 34 Slides)

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify or understand. We will cover the five core reasons why things are falling apart:

1. Debt and financialization

1. Debt and financialization2. Crony capitalism and the elimination of accountability

3. Diminishing returns

4. Centralization

5. Technological, financial and demographic changes in our economy

Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Not accepting responsibility and being powerless are two sides of the same coin: once we accept responsibility, we become powerful.

Kindle edition: $9.95 print edition: $24 on Amazon.com

To receive a 20% discount on the print edition: $19.20 (retail $24), follow the link, open a Createspace account and enter discount code SJRGPLAB. (This is the only way I can offer a discount.)

| Thank you, Craig H. ($100), for yet another outrageously generous contribution to this site -- I am greatly honored by your steadfast support and readership. | Thank you, John V. ($50), for yet another prodigiously generous contribution to this site --I am greatly honored by your steadfast support and readership. |