Bernanke's Neofeudal Rentier Economy

The Fed has directly created a neofeudal rentier economy and society.

Federal Reserve Chairman Bernanke is a Reverse Robin Hood, robbing from the lower 95% and giving to the financier class. The Real Reverse Robin Hood: Ben Bernanke and his Merry Band of Thieves (August 31, 2012).

It's worth understanding the mechanisms of this wealth transfer: in essence, the Fed extends low-cost credit (i.e. "free money") to the financier class which then uses this free money to buy rentier assets, that is, assets that generate economic rents for the owners, who add no value and create no wealth.

This is of course the neofeudal model: the financial aristocracy in the manor house own the rentier assets and the debt-serfs toil away to pay the rents and taxes. The financier class (i.e. those that benefit from the financialization of the economy) are as unproductive as feudal lords; they skim the profits generated by the debt-serfs while adding no productive value to the economy.

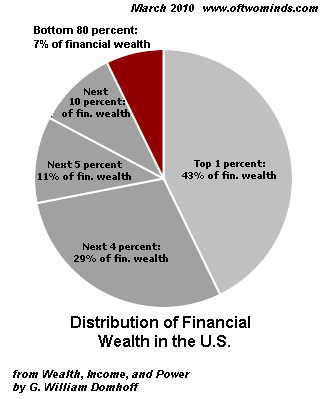

(I separate the bottom 95% from the top 4.5% and the .5% financier class for several reasons: 1) most of the stocks and bonds are owned by the top 5%; 2) the top 4.5% is shedding debt while the bottom 95% are adding debt; 3) the income of the top 4.5% is rising while household income of the bottom 95% is declining, and 4)the top 4.5% have access to lower-cost credit than the bottom 95%, but they do not have access to billions of dollars in nearly-free credit from the Fed or the shadow banking system like the financier class.)

Let's take rental housing as an example of this Fed-driven rentier economy. The financiers borrow $1 billion in nearly-free money and use these funds to buy thousands of houses for cash. Since they can offer cash, they beat out households with approved mortgage applications.

This is the story one hears anecdotally: potential home buyers have a mortgage application approved, all they need is to have their offer for a house accepted. But the house is sold to an investor with cash.

So while the Federal housing agencies are offering low-interest, low-down payment mortgages to marginally qualified (or flat-out unqualified) buyers, the Fed is enabling the financier class to outbid conventional homebuyers.

Here's the key dynamic: cash earns no return, thanks to the Fed's zero-interest rate policy (ZIRP). This means the interest rate paid by the financier class is also near-zero. So the trick is to take all those billions of nearly-free dollars and use them to buy assets returning 3+% annually.

These include rental housing, stocks that pay hefty dividends (for example utility companies), municipal bonds, long-term Treasuries, dividends based on patents and royalties, and everyone's favorite low-risk investment, state-sanctioned monopolies and cartels. (no wonder Big Pharma stocks have skyrocketed.)

Zero interest rates rob from the bottom 95% who do not have equal access to low-cost credit and transfer that wealth to the rentier-financier class. The bottom 95% provide the capital (pension funds, 401K accounts, checking and savings accounts, etc.) for zero return, but their access to near-zero cost credit is restricted.

The financier class then borrows money from the Fed (or the "shadow banking" non-bank credit system that is ultimately backstopped by the Fed) at near-zero rates, which it then uses to buy rentier assets that yield 3+%. The financier class then skims the rents from the debt-serfs, who have been effectively robbed of trillions of dollars in lost interest by the Federal Reserve.

The Fed has directly created a neofeudal rentier economy and society. Giving the financier class unlimited access to free credit with which to buy rentier assets serves two purposes: 1) it drives the valuations of rentier assets ever higher, creating the useful (in terms of propaganda and perception management) illusion of economic vitality, and 2) it greatly enriches the financier class at the expense of the bottom 95%.

Goebbels would approve of the Fed's masterful propaganda campaign: rob the bottom 95% to benefit the financier class, all the while piously proclaiming that its policies were aimed at increasing employment for the bottom 95%.

In terms of propagandistic chutzpah, it doesn't get any better than this. Congratulations, Bernanke, Yellen, et al.

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify or understand. We will cover the five core reasons why things are falling apart:

1. Debt and financialization

1. Debt and financialization2. Crony capitalism and the elimination of accountability

3. Diminishing returns

4. Centralization

5. Technological, financial and demographic changes in our economy

Complex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Not accepting responsibility and being powerless are two sides of the same coin: once we accept responsibility, we become powerful.

Kindle edition: $9.95 print edition: $24 on Amazon.com

To receive a 20% discount on the print edition: $19.20 (retail $24), follow the link, open a Createspace account and enter discount code SJRGPLAB. (This is the only way I can offer a discount.)

| Thank you, Christopher B. ($50), for your superbly generous contribution to this site -- I am greatly honored by your steadfast support and readership. | Thank you, David C. ($10), for your most generous contribution to this site -- I am greatly honored by your support and readership. |