The Endgame of State/Local Government Pensions

There is no way the pensions and benefits promised in an era of financialized abundance can be paid once the wheels of financialization fall off.

Yesterday I described the destructive effect of abundance on decision-making: An Abundance of Bad Decisions. One aspect of this dynamic is the tendency to extrapolate prosperity into the future as a permanent state of affairs.

One example of this is state/local government pensions: during the past 30 years of financialized abundance, the benefits and pensions promised to public employees were increased substantially. Public unions are a powerful political force in many states, and in eras of rising tax revenues, it's an easy political decision to increase public employee benefits and pension payouts.

The rising stock and bond markets generated huge profits for the public-employee pension funds, enabling them to grow without taxpayer contributions. The effortlessness and persistence of this growth encouraged the mindset that pensions would be paid for via the magic of ever-rising markets; if tax revenues weren't even needed to fund the pension plans, then no hard political choices would ever have to be made.

Alas, the 8+% annual growth rate of the boom era is now structurally unrealistic.The New Normal is bond yields of 2% or 3% at best, and equities markets that are increasingly at risk of significant sell-offs.

The illusion that the pension funds can pay the promised benefits is maintained by plugging wildly unrealistic 7% or 8% returns into projections of future pension fund earnings. Now those unrealistic projections are being questioned: California, Illinois on Brink of Pension Crisis (Mish).

This means tax revenues will have to be diverted from other government expenses to fund the pension plans.

A key dynamic in the pension crisis is called the the ratchet effect: it was effortless to increase the benefits and pensions of public employees, but it is effectively politically impossible to trim those promises.

The Ratchet Effect is one reason why the nation's political machinery has become sclerotic and ineffective: Dislocations Ahead: The Ratchet Effect, Stick-Slip and QE3(February 14, 2011).

As correspondent Mark G. explains, the public pension crisis has been 20 years in the making, and cannot be resolved without massive, sustained political and fiscal pain:

1. Long term interest rates began a secular decline in 1981. This continued until at least early this year.

2. In the early 1990s state and local politicians and their nominees began awarding management contracts to RIAs (Registered Investment Advisor) who promised higher rates of return. These promises were eagerly accepted at face value since it allowed them to reduce their annual contribution for defined benefit pension plans and spend the money elsewhere.

#1 plus the Reagan bull market made it possible to present this as fiscally responsible, or at least as progressive. Over the same period of time private corporations tended to shift to defined contribution plans for new hires. iow they ceased underwriting market risk for their pension funds. State and local governments will eventually be forced to follow this example.

Where Mish writes: "Pension plans typically assume 7.5% returns. That's not going to happen on a sustained basis with 10-year treasuries yielding close to 2%. Yet, any significant rise in bond yields will crush existing bondholders as well as wreak havoc in equities," he's underestimating the return assumption for a great many pension plans. CALPERS & CALSTRS (California public employee pension plans) are functionally at 8% or higher.

3. As a consequence of 1 & 2 defined benefit pension plans (along with charitable endowments) began a long-term movement out of bonds. The portfolio percentage allocations to stocks, followed by other forms of equity, began shooting up. Why would they not? The last time 30-year Treasuries saw 8% was in late 1994. It was already crystal clear by 1996 that investing in bonds was just a way to slowly sink into insolvency.

We're not on any "brink." It took two decades to get into this systemically insolvent condition. And I don't think this situation will produce further market instability. It's already been the main catalyst of market volatility since the mid 1990s in my second hand educated opinion. The dot.com and subprime housing bubbles could never have gotten so big without the participation of public and non-profit funds heaving hundreds of billions around in a chase for investment grade high yield.

In other words, the real casino action started at the precise moment that planning IRRs exceeded the 30-year US Treasury Bond rate.

What happens next? Probably a lot of things will happen. This particular crisis will revolve around defined benefit state and local government employee pension funds. It was created in the political arena and that's where it will be resolved.

I think the Democratic Party will be the most affected. The public employee unions are a core constituency and produce most of the ground troops for the Democrats. Broadly speaking there are two approaches. These are; 1) obtain more money and 2) reduce benefit payouts.

1. Obtain More Money.

a. Raising taxes (primarily targeting Republicans) will be the attempted default of Democrat single party states. But the crisis is most acute in precisely those single party Democratic states with the highest taxes already. It is therefore not clear this approach will really raise more money. It could equally create a large refugee movement of targeted taxpayers fleeing these jurisdictions, thus producing lower net revenues overall. The available demographic data says this process is well underway in California.

b. Shift appropriations between budget lines. This means reducing money for schools, police, highway maintenance, welfare et al and transferring it to pension funds. This will create conflict inside the Democratic party between key constituency groups.

c. Get the Federal government (or Federal Reserve) to undertake direct bailouts. This is going to create conflict between Democratic and Republican states over issues of federalism and "transfer payments".

2. Reduce Benefit Payouts.

Recent events in Wisconsin show the potential for this action to create extreme political unrest.

I have long been watching this situation as a potential vector for political collapse.

Thank you, Mark, for this primer on the unsustainability of public pension promises.Raising taxes is the default solution to state/local government shortfalls, but there's a structural problem with raising taxes:

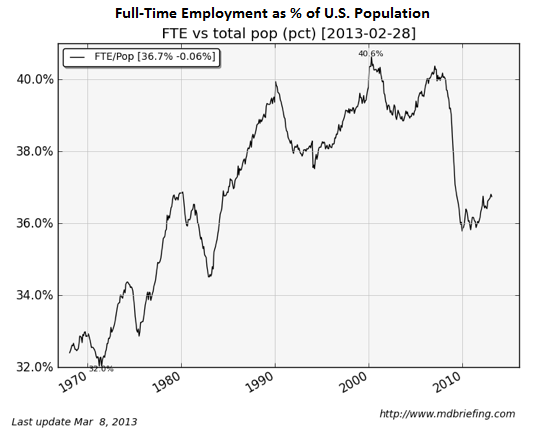

1. Fulltime jobs--the kind that pay the bulk of state/local taxes--are stagnant.

2. Real income is down for the vast majority of workers.

If state and local governments think low-income part-time workers can pay more taxes and survive, they are engaged in magical thinking:

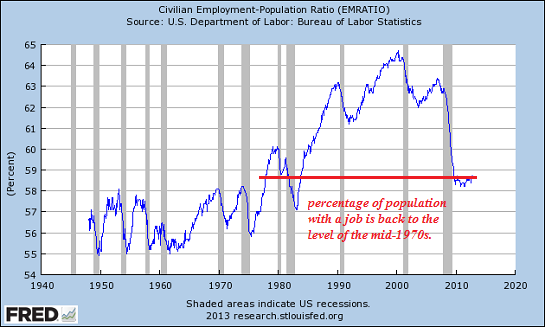

The percentage of the population with a job is back to the levels of the 1970s:

Real (adjusted for inflation) household income has declined by almost 8%; exactly how are households supposed to pay higher state and local taxes as their income steadily declines?

State and local governments planning on a Federal bailout should ponder this chart, which clearly shows a structural gap of monumental proportions between Federal tax revenues and Federal spending.

The endgame of promises made in an era of illusory, financialized abundance will be hurried along by a collapse in the equities and bond markets. I addressed the likelihood that all three primary investment markets would decline together in What If Stocks, Bonds and Housing All Go Down Together? (May 24, 2013): in a nutshell, if yields rise, mortgage rates rise and that sinks the housing market. Rising yields also sink stocks, as higher yields pull money out of risky equities. And rising yields also collapse the value of existing bonds, wiping out much of the wealth that is currently considered safe.

In sum: there is no way the pensions and benefits promised in an era of financialized abundance can be paid once the wheels of financialization fall off.

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify or understand. We will cover the five core reasons why things are falling apart:

1. Debt and financialization

1. Debt and financialization2. Crony capitalism and the elimination of accountability

3. Diminishing returns

4. Centralization

5. Technological, financial and demographic changes in our economyComplex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Not accepting responsibility and being powerless are two sides of the same coin: once we accept responsibility, we become powerful.

Kindle edition: $9.95 print edition: $24 on Amazon.com

To receive a 20% discount on the print edition: $19.20 (retail $24), follow the link, open a Createspace account and enter discount code SJRGPLAB. (This is the only way I can offer a discount.)

| Thank you, Sardar N. ($25), for your splendidly generous contribution to this site -- I am greatly honored by your support and readership. | Thank you, Jeffrey W. ($100), for your outrageously generous contribution to this site -- I am greatly honored by your steadfast support and readership. |