What Higher Mortgage Rates Mean in the Real World

Rising mortgage rates reduce household purchasing power just like higher taxes and inflation.

Mortgage rates have jumped significantly in the past few weeks, from 3.50% at the beginning of May to the current rate of 4.875% for conventional Fannie Mae mortgages.

These are the two rates quoted by a mortgage broker in Mish's recent post on rising mortgage rates.

Here is the repayment summary for both rates courtesy of mortgagecalculator.org:

Here is the repayment summary for both rates courtesy of mortgagecalculator.org:

I plugged in these parameters, basing them on the average cost of a new home and a mid-range property tax rate:

$360,000 home value, $300,000 mortgage, annual property tax rate of 1%, interest rate of 3.50%:

Monthly Payment: $1,647.13

Total of 360 Payments: $592,968.26

Total Interest Paid: $181,968.26

Total Tax Paid: $108,000.00

Interest rate of 4.875%: This is an increase of 1.375%, which represents a 39% increase over the initial rate of 3.50%.

Monthly Payment: $1,887.62

Total of 360 Payments: $679,544.88

Total Interest Paid: $271,544.88

Total Tax Paid: $108,000.00

The monthly payment rose by $240.49, or 14.6%. While unwelcome, that in itself doesn't seem like much.

But look at the lifetime cost increase: $86,576, all extra interest of course.

This relatively modest increase in mortgage rates to a still low by historical metrics 4.875% will reduce the purchasing power of the household by $240. Over time, $86,000 in additional interest payments will be transferred from the household to the lender/ owner of the mortgage.

We are constantly told inflation is near-zero, but a decline in purchasing power is equivalent to inflation. If one's labor buys fewer goods and services, then saying inflation doesn't exist is merely a semantic victory.

In other words, the $240 reduction in the household purchasing power due to rising rates has the exact same effect as inflation that reduced the household's monthly income by $240/month.

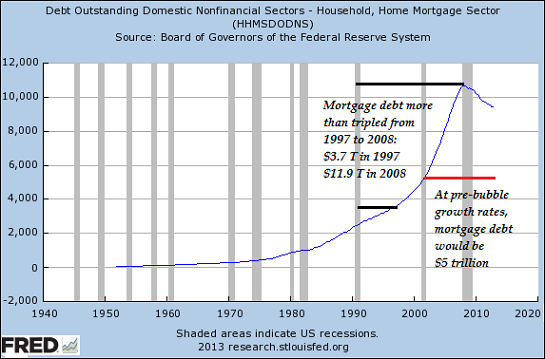

For context, here is a chart of mortgage debt. The total debt has declined for a number of reasons, including writedowns due to defaults and foreclosures and the decline in housing prices, which reduced the size of new mortgages:

Over time, rates on the roughly 48 million outstanding mortgages in the U.S. will rise. There are still millions of adjustable rate mortgages out there, often second mortgages or home-equity lines of credit (HELOCs). Those will start ticking higher in the months ahead.

$240 a month ($2,880 a year) may not seem like much, but multiply that by a million, and then by many millions, and the number starts becoming consequential: that money is no longer available for consumption or investment. Rising mortgage rates reduce household purchasing power just like higher taxes and inflation. That means there is less household income to spend on other things, and that's not good for "growth."

Things are falling apart--that is obvious. But why are they falling apart? The reasons are complex and global. Our economy and society have structural problems that cannot be solved by adding debt to debt. We are becoming poorer, not just from financial over-reach, but from fundamental forces that are not easy to identify or understand. We will cover the five core reasons why things are falling apart:

1. Debt and financialization

1. Debt and financialization2. Crony capitalism and the elimination of accountability

3. Diminishing returns

4. Centralization

5. Technological, financial and demographic changes in our economyComplex systems weakened by diminishing returns collapse under their own weight and are replaced by systems that are simpler, faster and affordable. If we cling to the old ways, our system will disintegrate. If we want sustainable prosperity rather than collapse, we must embrace a new model that is Decentralized, Adaptive, Transparent and Accountable (DATA).

We are not powerless. Not accepting responsibility and being powerless are two sides of the same coin: once we accept responsibility, we become powerful.

Kindle edition: $9.95 print edition: $24 on Amazon.com

To receive a 20% discount on the print edition: $19.20 (retail $24), follow the link, open a Createspace account and enter discount code SJRGPLAB. (This is the only way I can offer a discount.)

| Thank you, Steve D. ($10), for your most generous contribution to this site -- I am greatly honored by your support and readership. | Thank you, Schuyler G. ($25), for your extremely generous contribution to this site -- I am greatly honored by your support and readership. |